Prices

July 17, 2018

SMU Price Ranges & Indices: Quiet Week

Written by Brett Linton

The market has been relatively quiet this past week with only minor adjustments to the flat rolled indices. Steel Market Update is hearing steel buyers’ concerns about possible price declines. At the same time, there are others who are positive that prices will remain within $50 per ton of today’s levels through the end of the year.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $900-$930 per ton ($45.00/cwt-$46.50/cwt) with an average of $915 per ton ($45.75/cwt) FOB mill, east of the Rockies. The lower end of our range rose $10 per ton compared to one week ago, while the upper end remiained the same. Our overall average is up $5 per ton compared to last week. Our price momentum on hot rolled steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sideways over the short term.

Hot Rolled Lead Times: 4-8 weeks

Cold Rolled Coil: SMU price range is $980-$1,020 per ton ($49.00/cwt-$51.00/cwt) with an average of $1,000 per ton ($50.00/cwt) FOB mill, east of the Rockies. The lower end of our range remained the same compared to last week, while the upper end decreased $20 per ton. Our overall average is down $10 per ton compared to one week ago. Our price momentum on cold rolled steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sideways over the short term.

Cold Rolled Lead Times: 5-10 weeks

Galvanized Coil: SMU base price range is $48.50/cwt-$51.50/cwt ($970-$1,030 per ton) with an average of $50.00/cwt ($1,000 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end declined $20 per ton. Our overall average is unchanged compared to last week. Our price momentum on galvanized steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sideways over the short term.

Galvanized .060” G90 Benchmark: SMU price range is $1,056-$1,116 per net ton with an average of $1,086 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5-12 weeks

Galvalume Coil: SMU base price range is $51.00/cwt-$52.50/cwt ($1,020-$1,050 per ton) with an average of $51.75/cwt ($1,035 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged compared to one week ago. Our price momentum on Galvalume steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sideways over the short term.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,311-$1,341 per net ton with an average of $1,326 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6-11 weeks

Plate: SMU price range is $960-$1,000 per ton ($48.00/cwt-$50.00/cwt) with an average of $980 per ton ($49.00/cwt) FOB the customer’s facility for orders to be delivered during the month of September. The lower end of our range rose $20 per ton compared to one week ago, while the upper end remained the same. Our overall average is up $10 per ton compared to last week. Our price momentum on plate steel is for higher prices once the mills open their October order books. The plate mills are on controlled order entry and are expected to remain that way over the next 30 days or longer.

Plate Lead Times: 4-9 weeks, allocation/controlled order entry

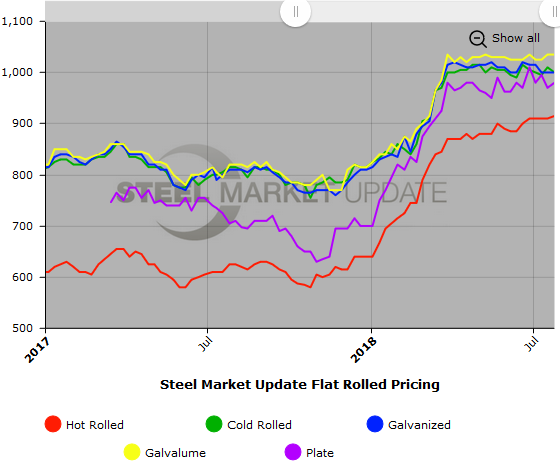

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. Note that plate prices are not yet available on our website, but we are in the process of adding that dataset. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or 800-432-3475.