Prices

October 9, 2018

Mill Capacity Utilization Stuck Around 79 Percent

Written by Brett Linton

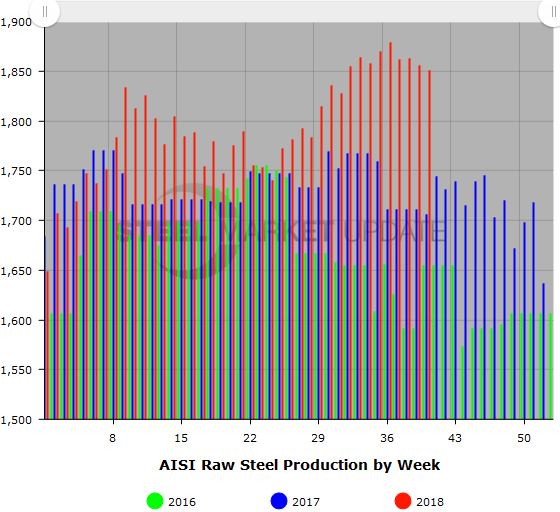

U.S. mills have cranked out steel at a capability utilization rate of 79.0 percent or better for nine weeks in a row, but only briefly have breached the 80 percent mark. U.S. raw steel production for the week ending Oct. 6 totaled 1,851,000 net tons with the mills operating at 79.0 percent capacity, reported the American Iron and Steel Institute.

Utilization peaked a month ago at 80.2 percent, which was the highest level in five years except for mid-August 2014 when it hit 80.3 percent. The domestic industry aspires to keep overall steel production above the 80 percent level to assure sustained profitability, but so far has fallen short of that goal.

Adjusted year-to-date producton through Oct. 6 totaled 72,320,000 net tons at a capability utilization rate of 77.5 percent, up 4.6 percent from the same period last year when the capability utilization was 74.4 percent.

Following is production by district for the Oct. 6 week: North East: 216,000 net tons; Great Lakes, 646,000 net tons; Midwest, 196,000 net tons; South, 720,000 net tons; and West, 73,000 net tons, for a total of 1,851,000.

Note, mill capability for fourth-quarter 2018 is approximately 30.8 million tons, compared to 30.6 million tons for the same period last year and 30.8 million tons for third-quarter 2018.

The raw steel production tonnage provided in this report is estimated. The figures are compiled from weekly production tonnage from 50 percent of the domestic producers combined with monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The AISI monthly production report provides a more detailed summary of steel production based on data supplied by companies representing 75 percent of U.S. production capacity.