Plate

March 20, 2019

SMU Imports Report: Cut to Length Plate

Written by Peter Wright

Each month, Steel Market Update produces an import analysis by region for two of the six flat rolled product groups (HRC, CRC, HDG, OMC, cut to length (CTL) plate and coiled plate). This month we are focusing on plate products. The intent of these regional updates is to bridge the gap between our monthly license data summaries and the detailed monthly reports we produce for premium subscribers that cover import volume by port and source.

![]()

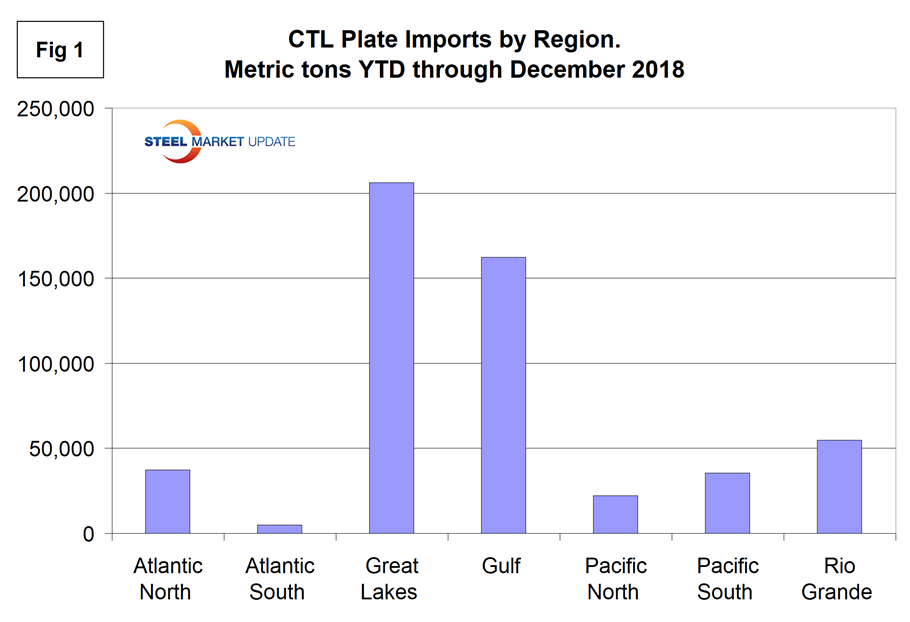

In 2018 YTD December, 39.4 percent of all cut to length plate imports came in through the Great Lakes ports. The Gulf was in 2nd place with 31.0 percent and the Rio Grande Valley third with 10.5 percent. Only 8.0 percent of the total came into the whole Atlantic coast and only 11.0 percent into the whole Pacific coast (Figure 1).

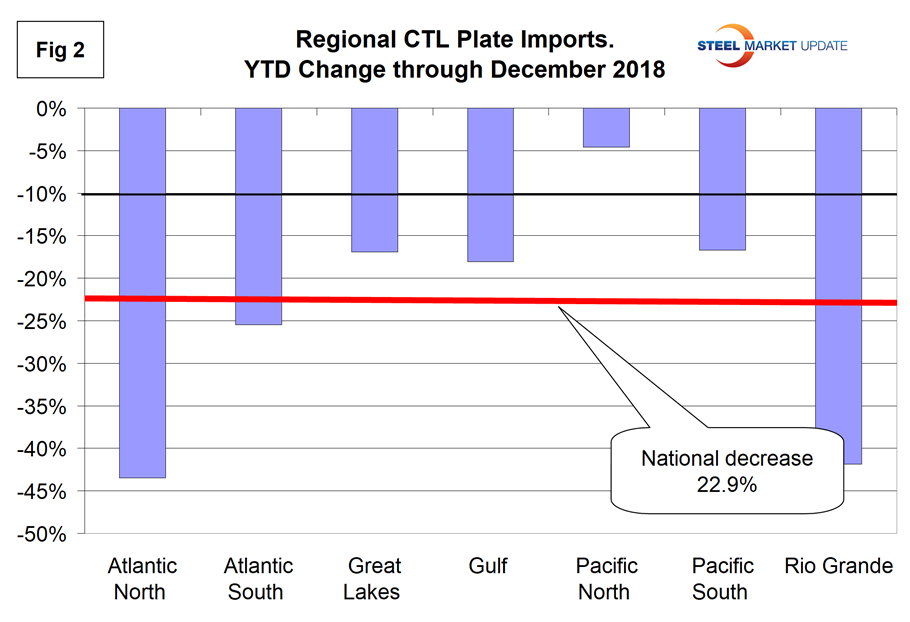

Imports into the U.S. as a whole were down by 22.9 percent in 2018 compared to 2017, but the tonnage coming over the Rio Grande was down by 41.9 percent and tonnage into the Great Lakes, which was the highest volume district, was down by 16.9 percent. Figure 2 shows the percent change by region in 2018 compared to 2017.

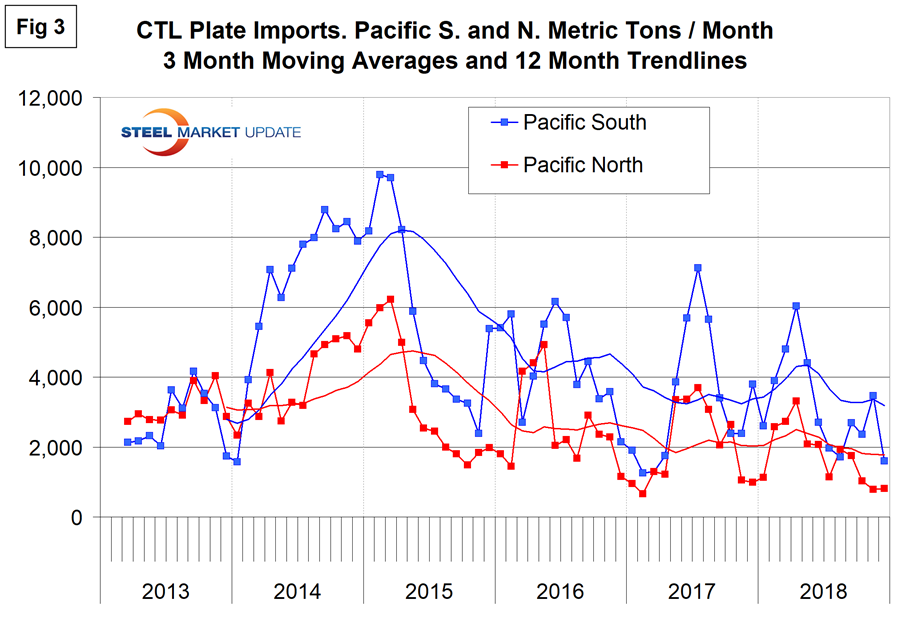

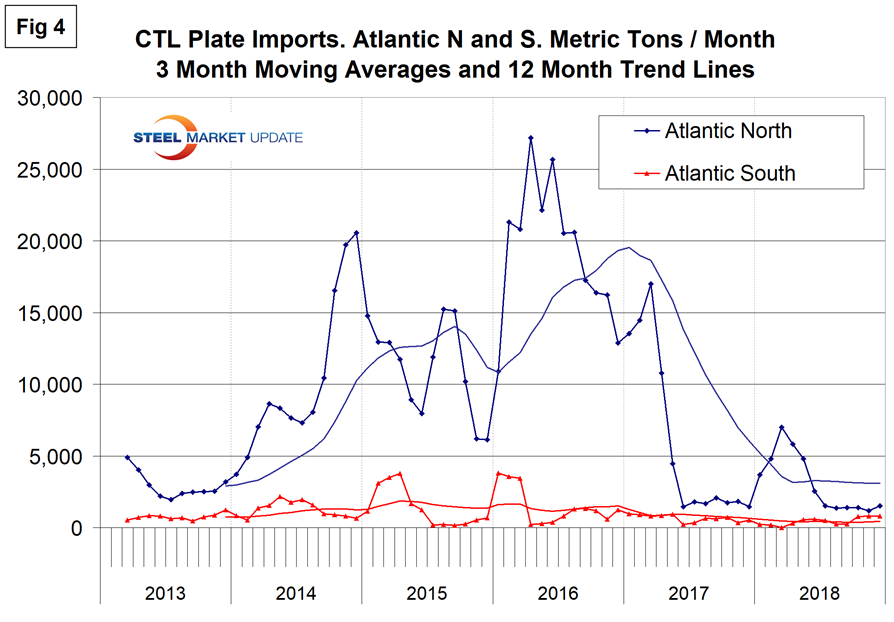

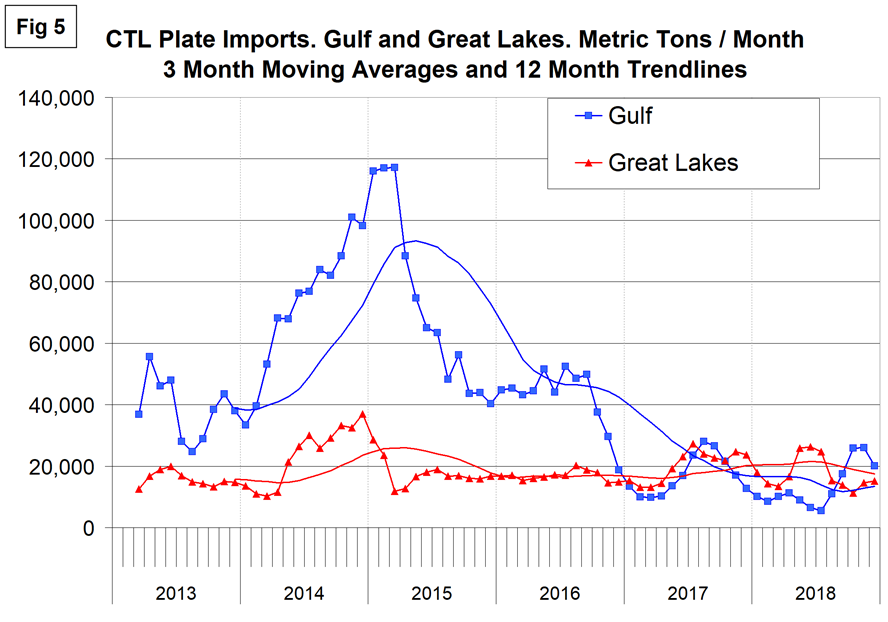

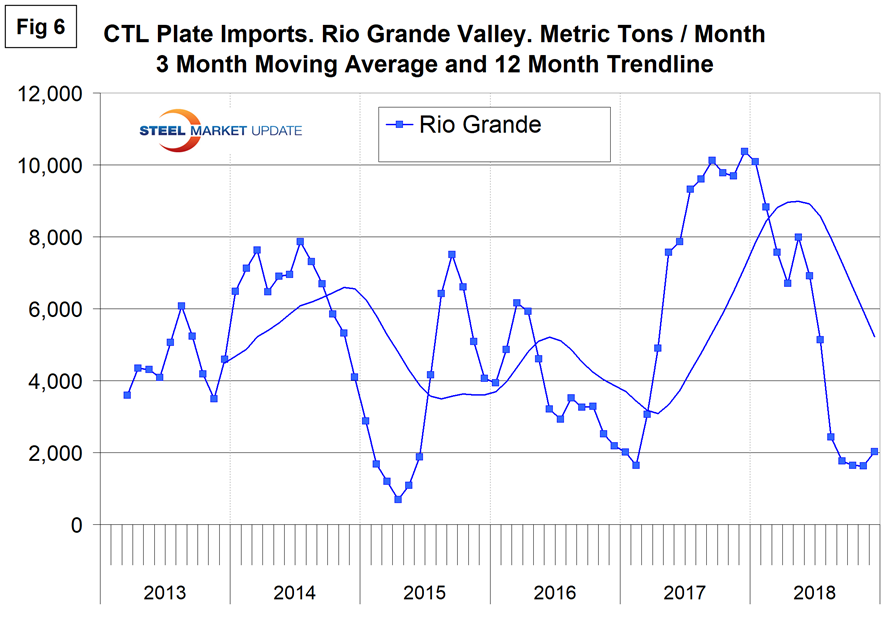

Figures 3, 4, 5 and 6 show the history of CTL plate imports by region since March 2013 on a three-month moving average basis.

Imports through the Pacific coast ports has been very erratic since the beginning of 2016 and currently both the North and South ports are at a low point.

CTL plate imports into the North Atlantic ports collapsed from mid-2016 to mid-2017. There was a partial recovery in early summer of 2018 before another collapse. Imports into the South Atlantic have been minimal throughout the whole time frame of this study.

Import volume into the Gulf has declined drastically since early 2015, but has been fairly consistent since late 2016. Imports into the Great Lakes have been fairly consistent since 2013.

Tonnage out of Mexico, mostly through Laredo, increased strongly in 2017 and lost by the same amount in 2018.

Premium subscribers have access to detailed reports by district and source nation on our website in the Analysis> Imports/Export section.