Market Data

June 23, 2019

SMU Steel Buyers Sentiment Index: Emotional Bottom?

Written by Tim Triplett

Industry optimism, as measured by Steel Market Update’s Steel Buyers Sentiment Index, remains in tepid territory despite slight upticks in both the Current and Future Index readings this week. This is the first time since early April that the indexes have not shown another decline, perhaps signaling some sort of emotional bottom. But weak steel prices and uncertain demand clearly continue to dampen industry attitudes.

The goal of the index is to measure how buyers and sellers of steel feel about their company’s ability to be successful today (Current Sentiment Index), as well as three to six months into the future (Future Sentiment Index). Results are posted as both single data points and as three-month moving averages (3MMAs) to smooth out the trend.

Current Sentiment measured as a single data point registered +42 in the latest data, up 7 points in the past two weeks but still far below the peak of +78 in January 2018.

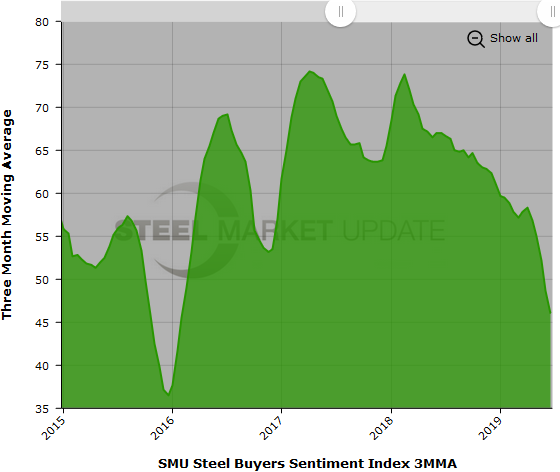

Measured as a 3MMA, Current Sentiment averaged 46.00, down more than 6 points from the reading a month ago. The last time the Current 3MMA was this low was February 2016. The 3MMA for Current Sentiment peaked at 74.17 in April 2017.

Future Sentiment

Respondents were asked to assess their chances for success in three to six months. Measured as a single data point, Future Sentiment registered +46, up a slight 4 points over the last two weeks. Future Sentiment peaked at +77 in February 2017.

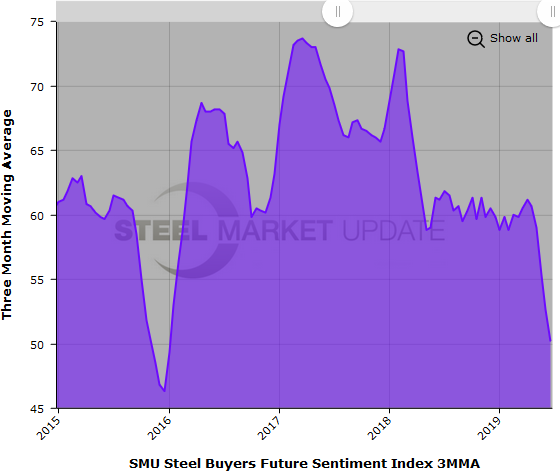

Measured as a 3MMA, the Future Sentiment Index averaged 50.17, down another 2.5 points and at its lowest point since January 2016. Future 3MMA peaked at 73.67 in March 2017.

Note that any figure above zero falls on the optimistic half of SMU’s scale. Therefore, industry sentiment remains positive, though far less so than last year.

What Our Respondents Had to Say

“Downward pressure on pricing is a major concern.”

“This is worse than 2009.”

“Prices need to stabilize so margins can stabilize.”

“The uncertainty of trade makes my customers nervous and less willing to buy long and makes imports less and less attractive. I see this uncertainty and cautious buying continuing into the future.”

“Nothing out there that makes me hopeful for a better second half.”

“I think we are fast approaching a bottom and once the market psychology changes prices will rebound nicely.”

“We are at the bottom.”

About the SMU Steel Buyers Sentiment Index

SMU Steel Buyers Sentiment Index is a measurement of the current attitude of buyers and sellers of flat rolled steel products in North America regarding how they feel about their company’s opportunity for success in today’s market. It is a proprietary product developed by Steel Market Update for the North American steel industry.

Positive readings will run from +10 to +100 and the arrow will point to the righthand side of the meter located on the Home Page of our website indicating a positive or optimistic sentiment. Negative readings will run from -10 to -100 and the arrow will point to the lefthand side of the meter on our website indicating negative or pessimistic sentiment. A reading of “0” (+/- 10) indicates a neutral sentiment (or slightly optimistic or pessimistic), which is most likely an indicator of a shift occurring in the marketplace.

Readings are developed through Steel Market Update market surveys that are conducted twice per month. We display the index reading on a meter on the Home Page of our website for all to see. Currently, we send invitations to participate in our survey to more than 600 North American companies. Our normal response rate is approximately 110-150 companies. Of those responding to this week’s survey, 39 percent were manufacturers and 44 percent were service centers/distributors. The balance was made up of steel mills, trading companies and toll processors involved in the steel business. Click here to view an interactive graphic of the SMU Steel Buyers Sentiment Index or the SMU Future Steel Buyers Sentiment Index.