Market Data

August 22, 2019

Steel Mill Negotiations: Little Change in Tone of Talks

Written by Tim Triplett

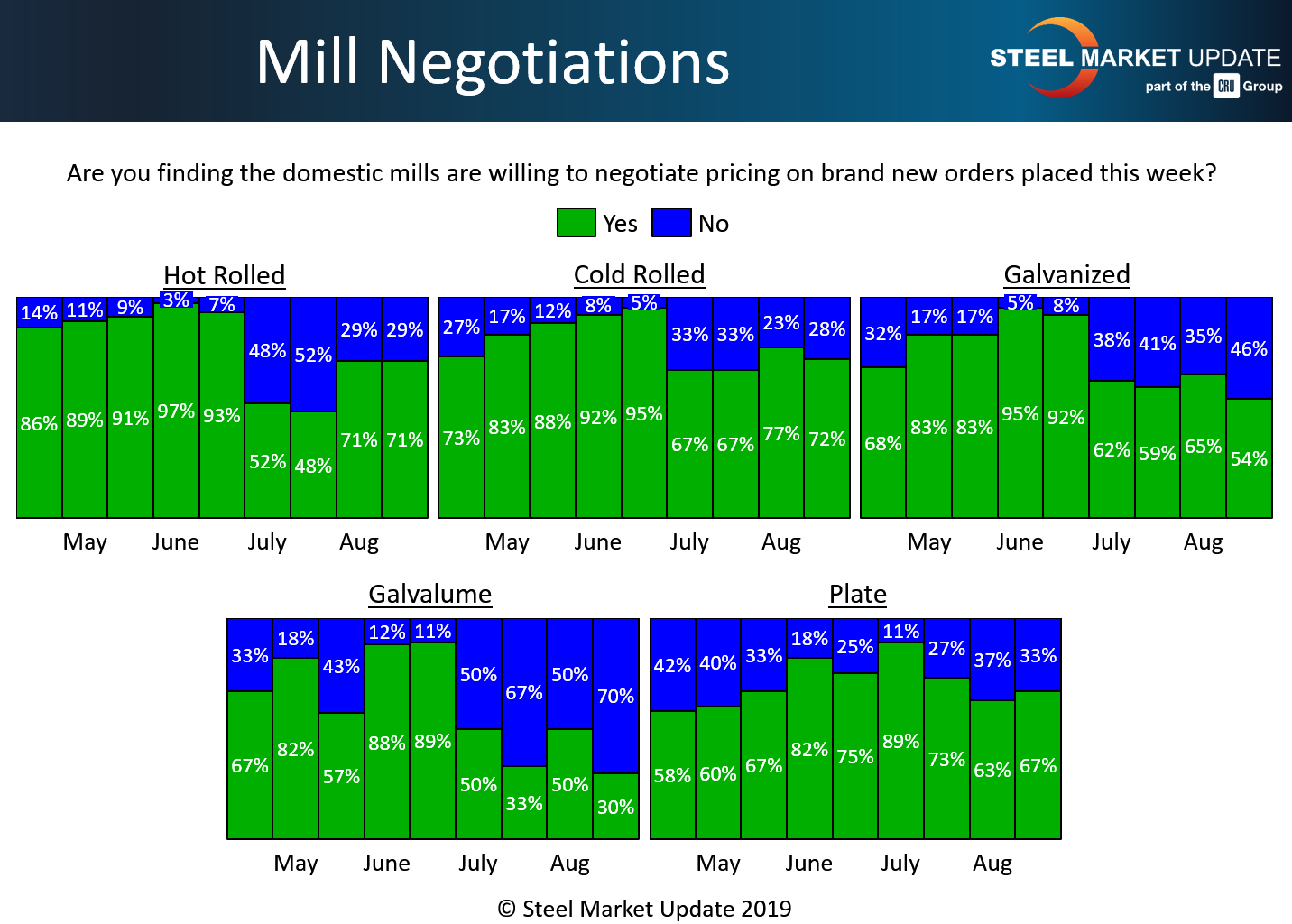

There has been little change in the tone of price talks over the past two weeks. The majority of buyers continue to report that mills generally are willing to negotiate to secure spot orders, even as they work to collect recent price increases on flat rolled and plate products.

Since late June, the mills have increased flat rolled prices three times for a total of $120 per ton, and plate prices twice for a total of $80 per ton. SMU’s average benchmark price for hot rolled has risen to $585 per ton this week from a low of $520 on June 25, so the mills have managed to collect a portion of the increase. SMU’s Price Momentum Indicator is still pointing Higher, but prices appear to be very open for discussion.

In the hot rolled segment, 71 percent of respondents to Steel Market Update’s market trends questionnaire said the mills were still open to price talks on HR this week, unchanged from earlier in the month. Just 29 percent said their mill suppliers were holding the line.

In the cold rolled segment, a slightly smaller percentage said the mills were negotiating. But at 72 percent (down 5 points in the past two weeks), it’s clearly still common for the mills to talk price. Only 28 percent report the mills holding firm on cold rolled prices, a percentage that has seen little change since the price increases were announced.

Suppliers of galvanized steel appear to be the least likely to discount. Forty-six percent of respondents said the galvanized mills just say no when asked to compromise on price. Yet the majority, 54 percent, said even galv producers were negotiating. Seventy percent of respondents reported that the mills are standing pat on Galvalume prices.

Plate prices are clearly in play as two out of three buyers report the plate mills willing to negotiate. Yet the mills are hoping to reverse a decline that has seen plate prices slide from more than $1,000 per ton at the beginning of the year. Following a small bump in early August, plates prices have settled around $790 per ton, according to SMU data.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.