Analysis

October 30, 2019

Final Thoughts

Written by John Packard

London, Brexit, new election, split country. As I was standing in line to enter the House of Lords, the gentleman to my left began discussing how Brexit has severed parties and even families. No longer can British families talk about their government openly. I heard the theme on many occasions as I traveled about London attending meetings associated with CRU events.

![]()

It is interesting watching TV here as there is very little about President Trump. Nice departure from the constant talking heads…. Well, almost, as this week there have been nonstop votes on Brexit with the deadline being today (Oct. 31). The EU has extended Brexit until the end of January, and after failing to approve Boris Johnson’s agreement with the EU, the government called for new parliamentary elections. The third election in four years. A new election does not guarantee Parliament will be able to come to a consensus.

If it is beginning to sound a little bit like what is going on back home in the United States….

But, I am here to visit the CRU London offices, meet with various heads of departments and work on next year’s SMU Steel Summit. I attended the CRU breakfast at LME Week on Tuesday and the CRU 50th anniversary celebration at The House of Lords on Wednesday.

We will be rolling out our 2020 SMU Steel Summit webpages around the middle of the month of November. I have been working on the outline of the agenda and penciling in speakers/panels that will meet the goals we have for the 2020 conference. I have been speaking with attendees to gather insights into what worked at this year’s conference and what changes our attendees would like to see. We will have a greater focus on forecasting in steel prices as well as industry segments affecting the flat rolled and plate steel markets.

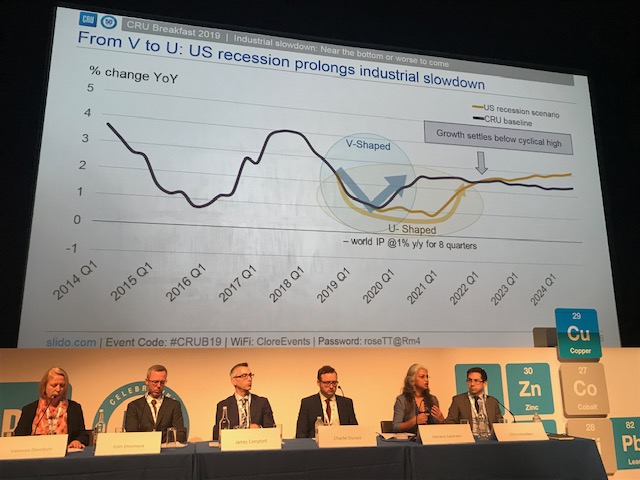

On Tuesday, CRU conducted a “breakfast meeting” that was essentially a half-day discussion of various metals markets and the world economy, with a focus on forecasting the U.S. economy. I was very impressed with the way CRU conducted their economic, steel and aluminum panel and I think it would be an excellent model for the 2020 SMU conference. I have discussed with Dr. Jumana Saleheen, the Chief Economist for the CRU Group, about her coming to Atlanta to replicate the panel I got to see on Tuesday.

The CRU Breakfast panel during LME Week in London on Tuesday.

A quick note, CRU is forecasting very slow growth in the U.S. economy for 2020. However, they presented two forecasts and how each would affect the metals (including steel) industries. There is a chance, due to negative effects of the Trump administration trade policies, for the U.S. economy to be pushed into a mild recession.

On Wednesday, I had the interesting experience to attend a reception for CRU’s 50th anniversary, which was held at the House of Lords (part of Parliament). Security to get in was very tight, but the reception was eye-opening for me, having not been associated with the CRU Group for that long. I was impressed by the history of the beginnings of the company (one of the original founders is a member of the House of Lords), the quality of the individuals who have worked and continue to work for the company, as well as the creativity the company has exhibited over the years in the metals, mining and fertilizer spaces.

Chairman Robert Perlman addressing staff, directors and key customers at the 50th anniversary of CRU at the House of Lords.

After three days of meetings and events with CRU, I am still very pleased that they are the owners of Steel Market Update. There will be some changes over the years, but I believe CRU understands the value of the SMU brand, and they will work to improve and expand SMU as a company in the years to come.

I will not return to my office until Monday, Nov. 4, as I am spending a couple of extra days here in chilly London to enjoy the city.

A reminder our next Steel 101: Introduction to Steel Making & Market Fundamentals workshop will be held in Ontario, Calif. (Los Angeles area). This is a very convenient location as there are multiple airports you can use to get there (Ontario being the closest; LAX is also an option). We will tour the California Steel Industries steel mill, and if time permits their pipe and tube mills. We have been updating the program with new instructors, and with changes to the program to make it a little more interactive as we work towards providing a better understanding of how the industry works. You can find more details on our website: www.SteelMarketUpdate.com/events/steel101

As always, your business is truly appreciated by all of us here at Steel Market Update.

John Packard, President & CEO