Market Data

December 3, 2019

SMU's November At-a-Glance

Written by Brett Linton

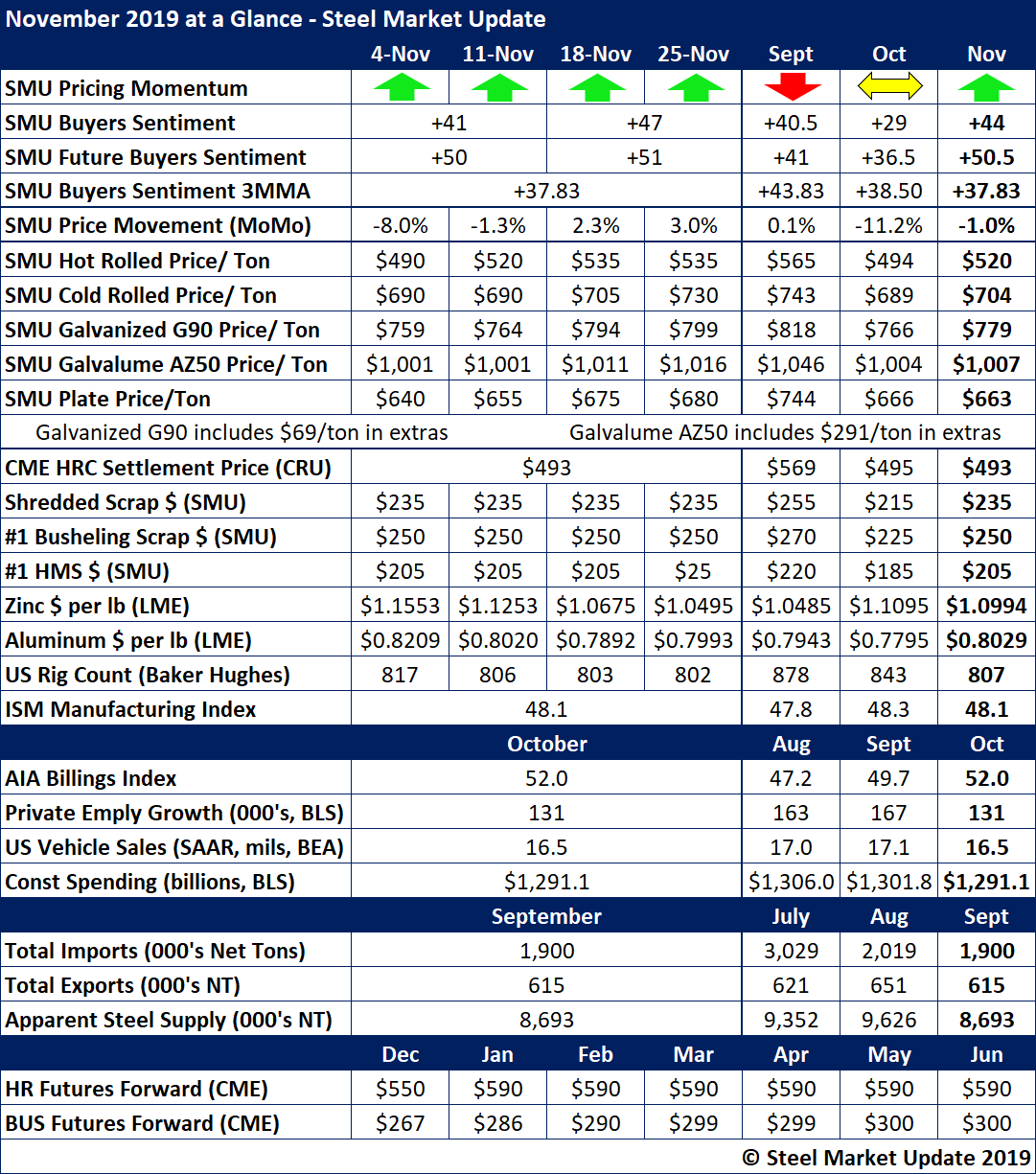

Steel prices had upward momentum in November following multiple price increase announcements by the mills on flat rolled and plate products. Steel Buyers Sentiment moved upward along with the prices as service centers and OEMs anticipated a strengthening market.

After bottoming in mid-October at around $480 per ton, the benchmark price for hot rolled steel moved up to about $535 per ton by the end of November, for a monthly average of $520. Other steel product prices increased to a similar degree, except for Galvalume and plate which were fairly flat.

Lending support to higher finished steel prices were ferrous scrap prices, which increased significantly in November from declines in October and for much of 2019.

True steel demand remained a question mark in November as ISM’s Manufacturing Index remained in contraction below the 50-point level and the U.S rig count in the energy sector continued to decline, among other measures of steel consumption.

See the chart below for other key benchmarks.