Prices

September 15, 2020

SMU Price Ranges & Indices: Flat Rolled Up Another $20-40

Written by Brett Linton

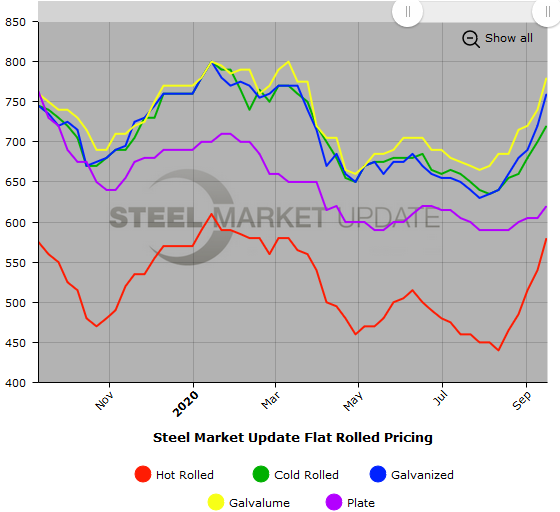

Better-than-expected demand and higher scrap prices have allowed the mills to boost flat rolled and plate steel prices, with the benchmark average for hot rolled reaching $580 per ton, according to Steel Market Update’s check of the market this week. With a few mills announcing new increases on flat rolled on Monday and Tuesday, the upward pressure on prices is likely to continue, at least for the short term. SMU’s Price Momentum Indicator continues to point Higher for flat rolled, though Neutral for plate, as the direction of plate prices is less clear.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $560-$600 per net ton ($28.00-$30.00/cwt) with an average of $580 per ton ($29.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $30 per ton compared to one week ago, while the upper end increased $50 per ton. Our overall average is up $40 per ton over last week. Our price momentum on hot rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Hot Rolled Lead Times: 4-8 weeks

Cold Rolled Coil: SMU price range is $700-$740 per net ton ($35.00-$37.00/cwt) with an average of $720 per ton ($36.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $40 per ton compared to last week, while the upper end remained unchanged. Our overall average is up $20 per ton over one week ago. Our price momentum on cold rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Cold Rolled Lead Times: 5-8 weeks

Galvanized Coil: SMU price range is $720-$800 per net ton ($36.00-$40.00/cwt) with an average of $760 per ton ($38.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end increased $60 per ton. Our overall average is up $40 per ton over last week. Our price momentum on galvanized steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $789-$869 per ton with an average of $829 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-9 weeks

Galvalume Coil: SMU price range is $760-$800 per net ton ($38.00-$40.00/cwt) with an average of $780 per ton ($39.00/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range increased $40 per ton compared to last week. Our overall average is up $40 per ton from one week ago. Our price momentum on Galvalume steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,051-$1,091 per ton with an average of $1,071 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 7-9 weeks

Plate: SMU price range is $590-$650 per net ton ($29.50-$32.50/cwt) with an average of $620 per ton ($31.00/cwt) FOB delivered to the customer’s facility. The lower end of our range remained unchanged compared to one week ago, while the upper end increased $30 per ton. Our overall average is up $15 per ton over last week. Our price momentum on plate steel is Neutral until the market establishes a clear direction.

Plate Lead Times: 4-6 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.