Prices

October 13, 2020

SMU Price Ranges & Indices: Not Much Change

Written by Brett Linton

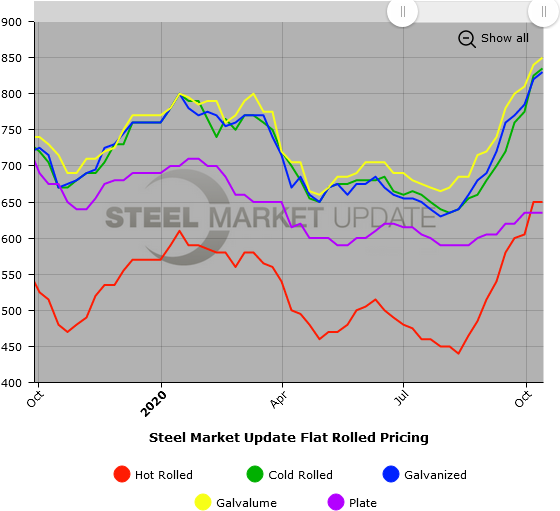

The benchmark price for hot rolled remained unchanged at around $650 per ton, according to Steel Market Update’s check of the market this week, even as the mills worked to collect the price increases announced earlier in the month. Other flat rolled products saw a modest increase. Begging the question: Is the upward price momentum beginning to slow? Forty percent of the respondents to SMU’s questionnaire this week said they believe prices are peaking. Almost all see the HR price leveling out somewhere south of $700 in the next 30-60 days. SMU’s Price Momentum Indicators continue to point Higher on both flat rolled and plate products, but we are keeping a close eye on the trend.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $640-$660 per net ton ($32.00-$33.00/cwt) with an average of $650 per ton ($32.50/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to one week ago. Our overall average is unchanged from last week. Our price momentum on hot rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Hot Rolled Lead Times: 6-8 weeks

Cold Rolled Coil: SMU price range is $800-$870 per net ton ($40.00-$43.50/cwt) with an average of $835 per ton ($41.75/cwt) FOB mill, east of the Rockies. The lower end of our range remained the same compared to last week, while the upper end increased $20. Our overall average is up $10 per ton from one week ago. Our price momentum on cold rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Cold Rolled Lead Times: 7-8 weeks

Galvanized Coil: SMU price range is $800-$860 per net ton ($40.00-$43.00/cwt) with an average of $830 per ton ($41.50/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range increased $10 per ton compared to one week ago. Our overall average is up $10 per ton from last week. Our price momentum on galvanized steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $869-$929 per ton with an average of $899 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-10 weeks

Galvalume Coil: SMU price range is $840-$860 per net ton ($42.00-$43.00/cwt) with an average of $850 per ton ($42.50/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range increased $10 per ton compared to last week. Our overall average is up $10 per ton from one week ago. Our price momentum on Galvalume steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,131-$1,151 per ton with an average of $1,141 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 8-10 weeks

Plate: SMU price range is $610-$660 per net ton ($30.50-$33.00/cwt) with an average of $635 per ton ($31.75/cwt) FOB delivered to the customer’s facility. Both the lower and upper ends of our range remained the same compared to one week ago. Our overall average is unchanged from last week. Our price momentum on plate steel is Higher, meaning prices are expected to rise in the next 30 days.

Plate Lead Times: 5-8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.