Prices

November 16, 2020

Regional Imports Through September: Other Metallic Coated

Written by Peter Wright

National level import reports do a good job of measuring the overall market pressure caused by the imports of individual products. The downside is that there are huge regional differences. This report examines other metallic coated imports (mainly Galvalume) by region through September 2020.

![]()

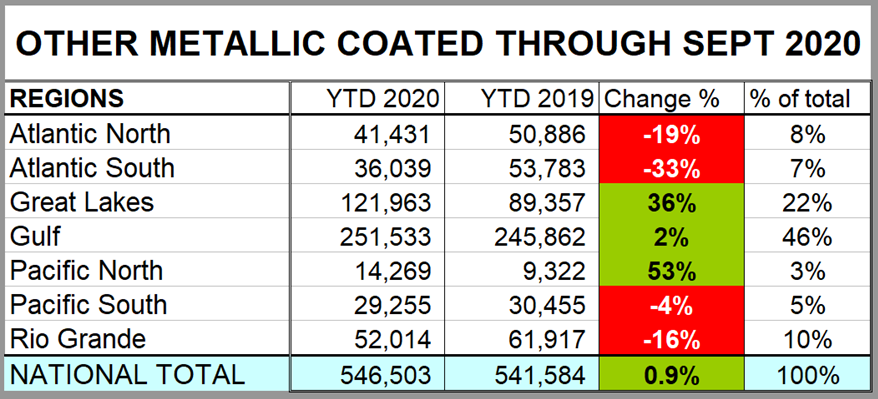

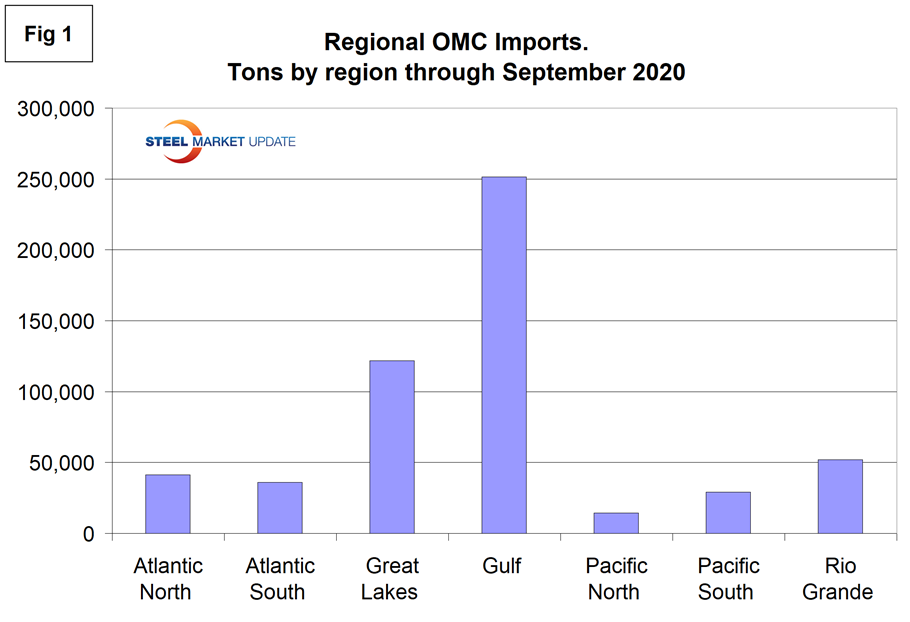

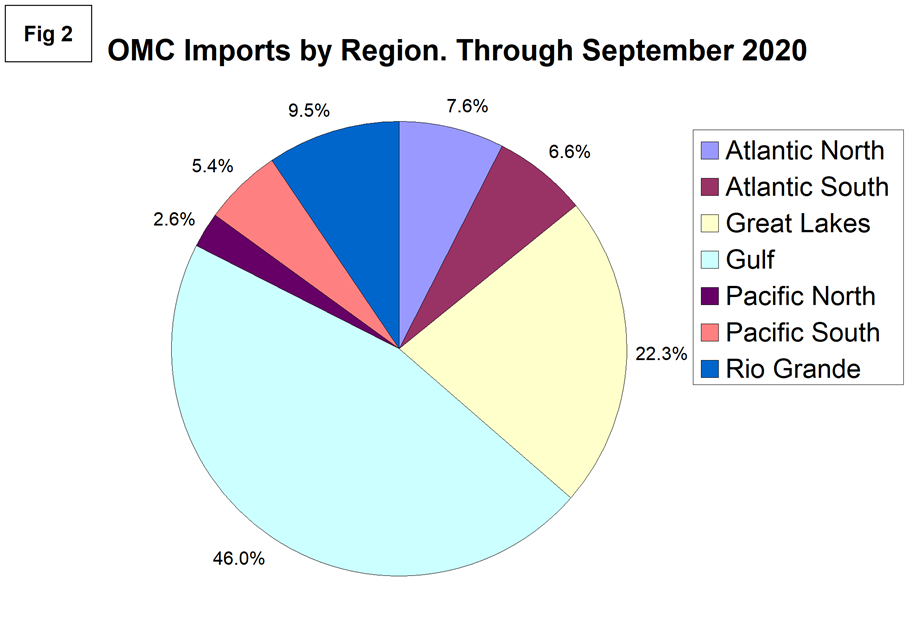

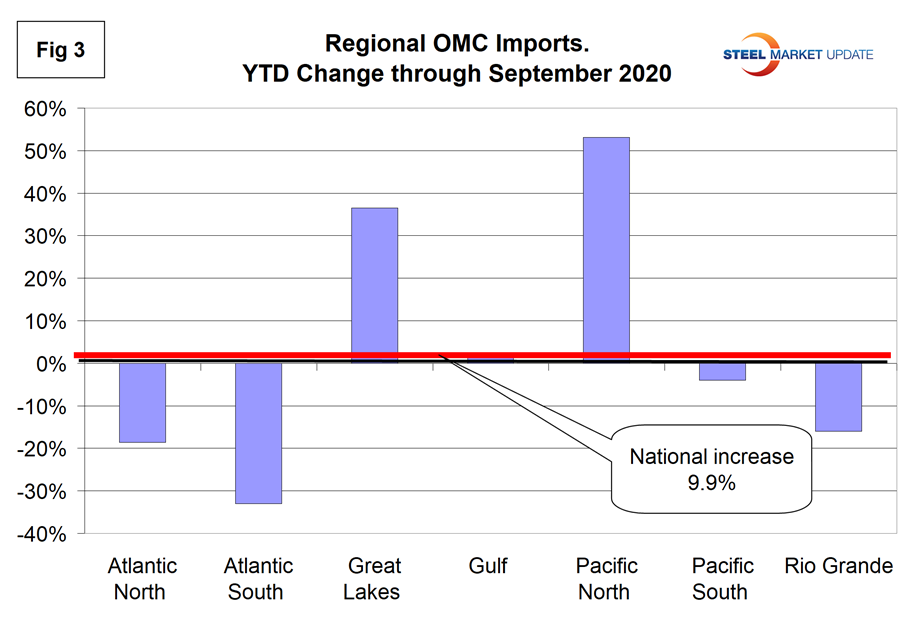

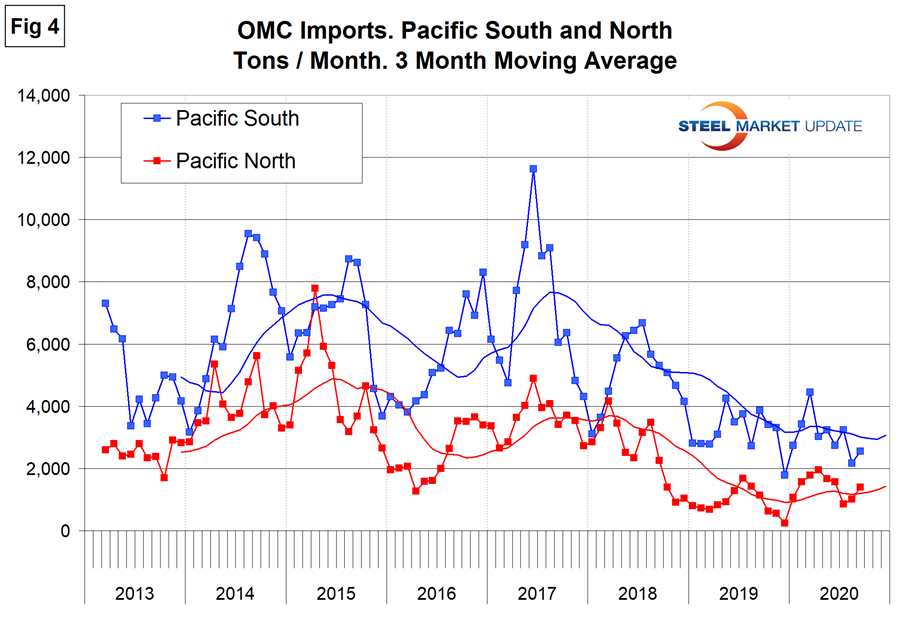

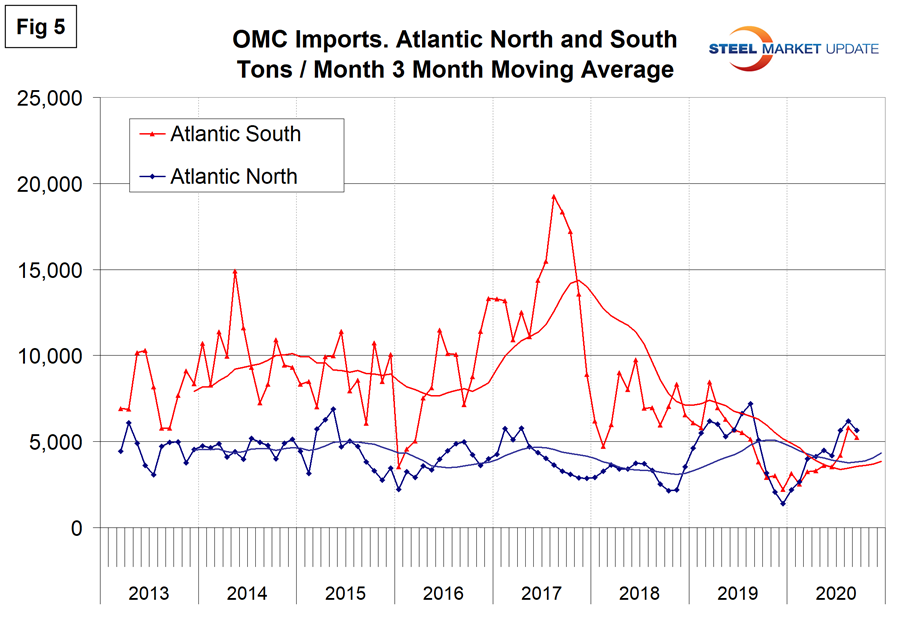

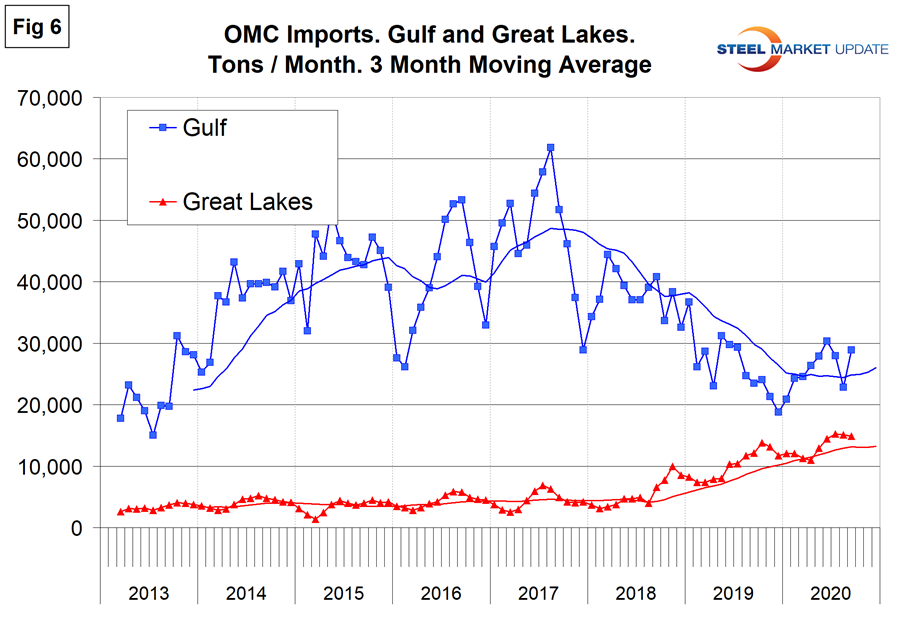

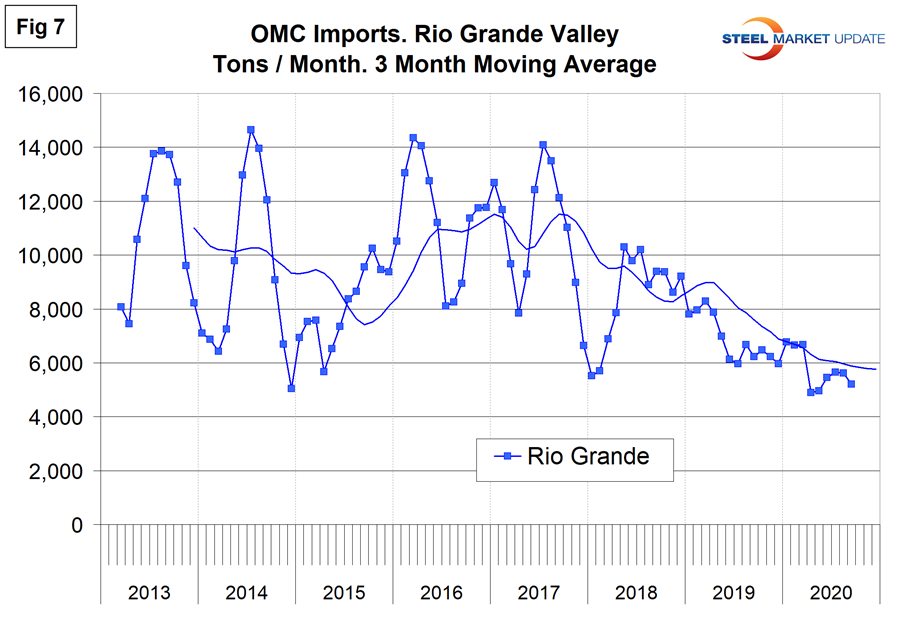

In September, OMC imports were up by 0.9 percent at the national level. This was the only flat rolled product to experience a year-over-year increase. On a regional basis, this ranged from a 53 percent increase in the North Pacific to a 33 percent decline in the South Atlantic. The Gulf has received by far the most tonnage in 2020 and accounts for 46 percent of the national total. Tonnage into the Atlantic N. and S. and Pacific N. and S. each accounted for less than 8 percent of the total.

Note the tonnage scales on the Y axis of Figure 4-7 are not the same.

Pacific Coast: The tonnage into both Pacific regions has been fairly consistent since the beginning of 2019, with the South having about twice the tonnage of the North.

Atlantic Coast: The tonnage into both Atlantic regions declined in 2019 and has increased in 2020, but the whole Eastern Seaboard is only 15 percent of the national total. Sixty-five percent of the East Coast tonnage enters through Philadelphia.

Gulf and Great Lakes: Tonnage into the Great Lakes ports has been steadily increasing since February 2018 and was up by 36 percent in 2020 through September. The Gulf receives the most tonnage of the seven regions and has accounted for 46 percent of the total this year.

Rio Grande: The river crossings only account for 10 percent of the national total and in 2020 year to date were down by 16 percent. Almost all of this tonnage comes in through Laredo and has steadily declined since May 2018.

Notes: SMU presents a comprehensive series of import reports ranging from the first look at licensed data to a detailed look at volume by district of entry and source nation. The report you are reading now is designed to plug the gap between these two. This report breaks total year to date import tonnage of six flat rolled products into seven regions and the growth/contraction for each product and region. There is a summary table for each product group and a bar chart showing volume by region for the first seven months of 2020. These are reference documents with no specific comments. These charts have been developed as a guide for buyers and sellers to have a broader understanding of what’s going on in their own backyard.

Regions are compiled from the following districts:

Atlantic North: Baltimore, Boston, New York, Ogdensburg, Philadelphia, Portland ME, St. Albans and Washington. DC.

Atlantic South: Charleston, Charlotte, Miami, Norfolk and Savannah.

Great Lakes: Buffalo, Chicago, Cleveland, Detroit, Duluth, Great Falls, Milwaukee, Minneapolis and Pembina.

Gulf: Houston, New Orleans, Mobile, San Juan, St. Louis and Tampa.

Pacific North: Anchorage, Columbia Snake, San Francisco and Seattle.

Pacific South: Los Angeles and San Diego.

Rio Grande Valley: Laredo and El Paso.