Prices

December 29, 2020

SMU Price Ranges & Indices: Holiday Lull

Written by Brett Linton

Recently we were asked how we can produce our flat rolled and plate price indices when there are limited transactions either due to high prices or a holiday period like we are in now. In both scenarios there continue to be transactions (although few and far between), but we are careful not to overheat or overcool a market when limited transactions are occurring.

In past years, SMU has tended not to change prices between the Christmas and New Year Holidays due to the limited responses we were able to gather from the market.

This year is no different. We have limited actual transaction data points, which gives us pause when considering changing our average. However, at the same time, the data we did collect is indicative of a market that continues to move higher. Through a hazy lens, we see hot rolled probably averaging $1,000 per ton ($50.00/cwt) rather than the $985 per ton we published last week. Even so, we would like to have more data points to announce to the market that hot rolled has reached or exceeded $1,000 per ton.

The same goes for cold rolled, galvanized, Galvalume and plate products. On galvanized, we received base pricing of $59.00/cwt up to $65.00/cwt (one data point was an order for 60 tons, the other a quote). To complicate matters, we have a plate market that is fundamentally altering how the steel is being sold by the domestic steel mills (FOB Mill versus delivered pricing). We are in the process of changing how we will reference plate prices going forward. The question is, how do we tie the old prices and new prices so they can be compared against one another effectively?

We are making a conscious decision not to move prices this week, which will allow us to gather more data over the holidays and early next week. We do anticipate prices will rise, and our SMU Price Momentum Indicator continues to point toward higher prices on all products.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $950-$1,020 per net ton ($47.50-$51.00/cwt) with an average of $985 per ton ($49.25/cwt) FOB mill, east of the Rockies. Our price momentum on hot rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Hot Rolled Lead Times: 6-10 weeks

Cold Rolled Coil: SMU price range is $1,040-$1,100 per net ton ($52.00-$55.00/cwt) with an average of $1,070 per ton ($53.50/cwt) FOB mill, east of the Rockies. Our price momentum on cold rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Cold Rolled Lead Times: 7-12 weeks

Galvanized Coil: SMU price range is $1,050-$1,120 per net ton ($52.50-$56.00/cwt) with an average of $1,085 per ton ($54.25/cwt) FOB mill, east of the Rockies. Our price momentum on galvanized steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,119-$1,189 per ton with an average of $1,154 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 8-13 weeks

Galvalume Coil: SMU price range is $1,100-$1,150 per net ton ($55.00-$57.50/cwt) with an average of $1,125 per ton ($56.25/cwt) FOB mill, east of the Rockies. Our price momentum on Galvalume steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,391-$1,441 per ton with an average of $1,416 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 8-12 weeks

Plate: SMU price range is $840-$910 per net ton ($42.00-$45.50/cwt) with an average of $875 per ton ($43.75/cwt) FOB delivered to the customer’s facility. Our price momentum on plate steel is Higher, meaning prices are expected to rise in the next 30 days.

Plate Lead Times: 5-8 weeks

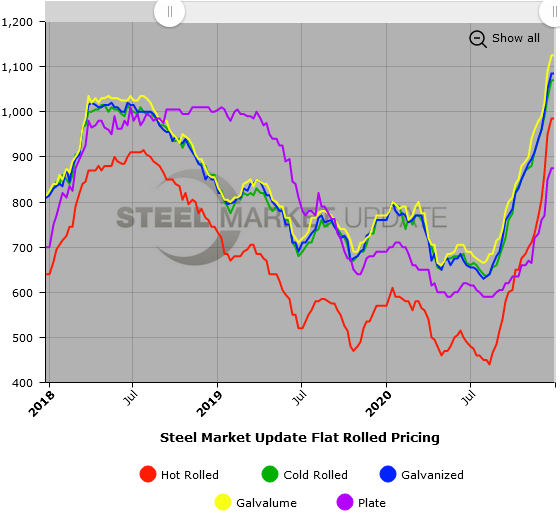

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.