Market Data

June 23, 2022

Steel Mill Negotiations: In Buyers' Favor

Written by Brett Linton

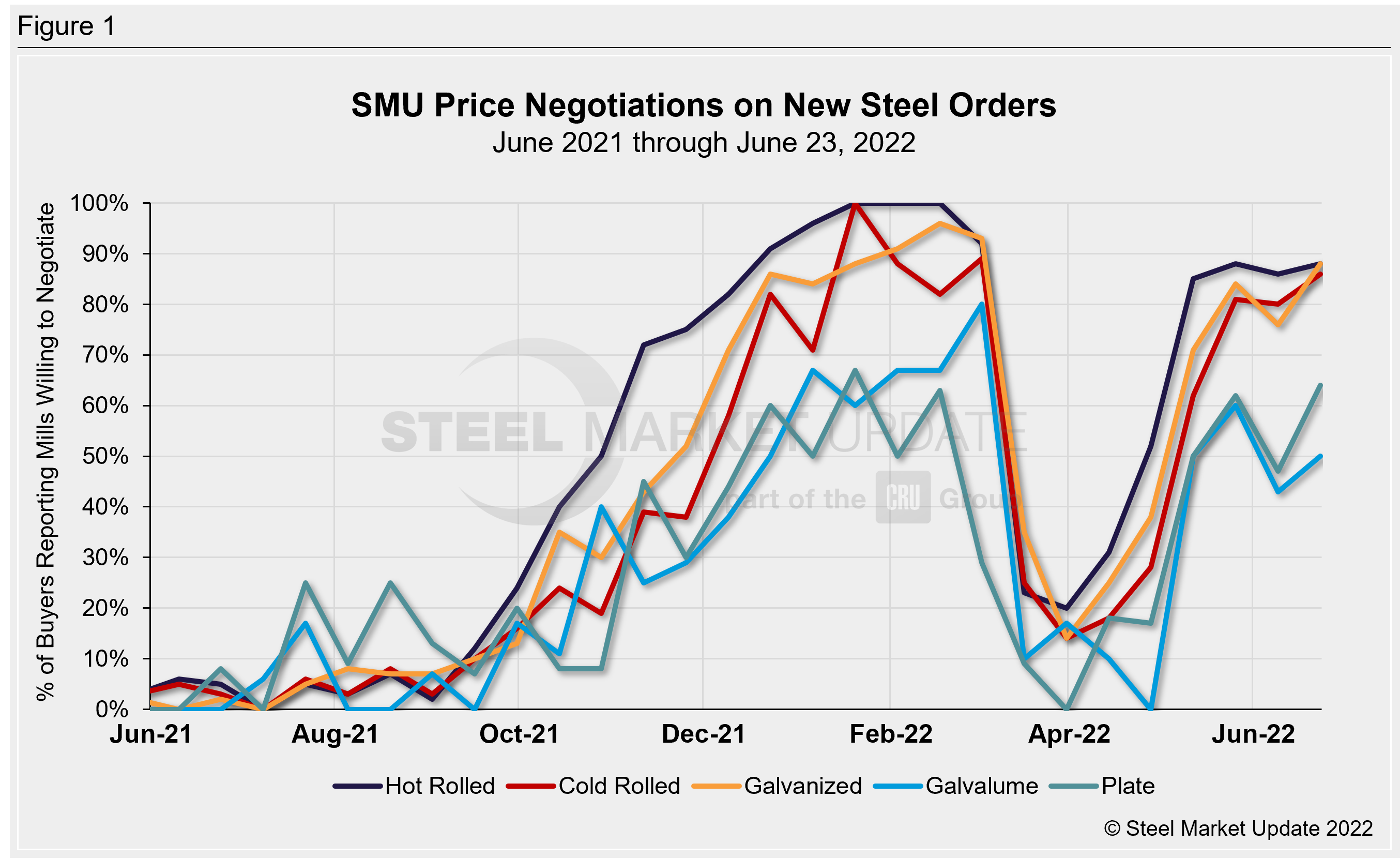

Approximately 84% of steel buyers report that mills are willing to talk price to secure an order, according to executives polled in our latest steel market survey. The rate of willingness to negotiate has remained over 50% in each of our market checks since early May and is now at the highest level since early March 2022.

Every other week, SMU asks survey respondents: Are you finding domestic mills are willing to negotiate spot pricing on new orders? On average this week, 84% of steel buyers report that mills were willing to negotiate lower prices on new orders, up from 74% when we polled the market two weeks prior and up from 81% one month ago. Recall we saw negotiation rates between 16-35% in March and April.

Broken down by product, 88% of hot rolled buyers surveyed this week responded that mills were willing to negotiate lower prices, in line with the levels we’ve recorded since mid-May. Cold rolled and galvanized respondents have also told the same story since late May, with 86-88% of buyers now reporting that mills are now negotiable. Negotiations on Galvalume products are mixed, with 50% reporting that mills are willing to negotiate, up from 43% two weeks prior but down from 60% one month ago. Note that Galvalume figures can be more volatile due to the limited size of that market and our smaller sample size.

Negotiations had been less common in the plate market, but our latest survey shows that 64% of plate buyers report mills are willing to bargain. This is up from 47% two weeks ago and up from 62% one month prior. Recall we saw plate negotiation rates of 0-18% in March and April.

SMU’s Price Momentum Indicator remains at Lower since our May 10th adjustment, indicating we expect prices to decline over the next 30–60 days.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.

By Brett Linton, Brett@SteelMarketUpdate.com