Prices

September 22, 2022

Hot Rolled Futures: Black Smoke Rising

SMU contributor Bryan Tice is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. He and the firm design and execute risk management strategies for clients. They also provide process and analytical support. Before joining Metal Edge Partners, Bryan held commercial leadership roles involving purchasing, sales, and risk management for Feralloy Corp.,Cargill Steel Service Centers, and Plateplus Inc.

You can learn more about Metal Edge at www.metaledgepartners.com. Bryan can be reached at Bryan@metaledgepartners.com for comments or questions.

It is a bit embarrassing to admit that someone who writes only a handful of articles a year for SMU gets writers block. But I found myself in that very place today trying to think of something interesting to write about a topic that is fairly one dimensional.

As in the past I find myself going to my music playlist to see if I can find some inspiration from people who are 100x more creative than myself. Given my Michigan roots, I stuck to artists from my home state.

There I go, turn the page. (Bob Seger. Look it up if you didn’t catch the reference.)

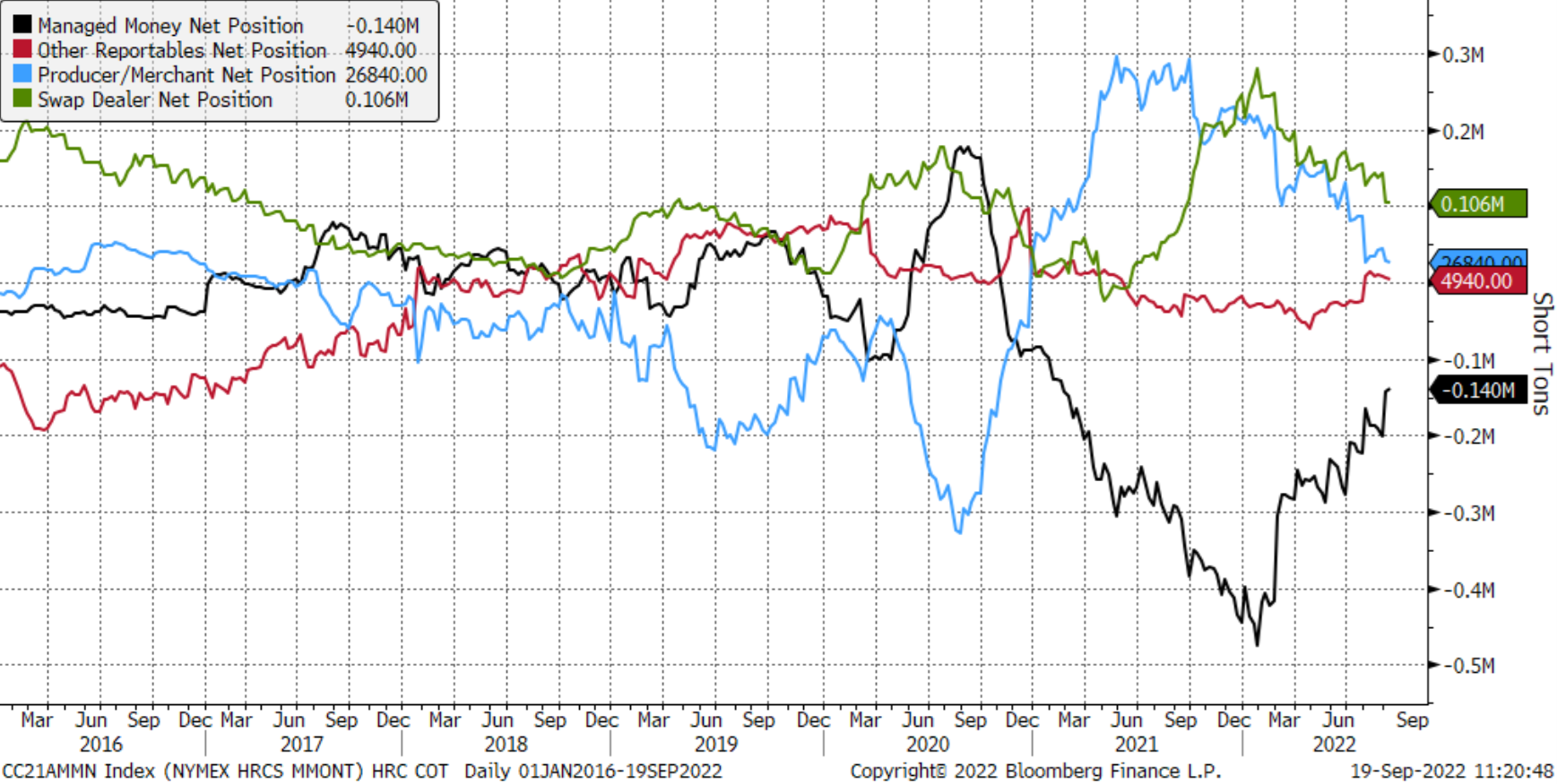

When looking for balance to the bearish narrative circulating in the market, we often look to the commitment of trader’s report. Those of us who trade the HRC contract have referenced this before in articles. A quick refresher: it captures the positions of those trading the contract and gives an objective look at how the different market participants are positioned.

We tend to focus on the managed-money category because those tend to be hedge funds and commodity trading advisors who may be speculating on the market. While not neutral, these managed money participants (black line) have continued to reduce their short positions, which suggests they may feel there is limited downside to current price levels. This does not necessarily mean they have a bullish view on the market. They may simply be happy taking profits and pulling some chips off the table.

Producers (blue line), in contrast, have also cut their long positions meaningfully over the last six months. Given the current trajectory of each segment, these lines could crossover for the first time since November 2020.

When that last occurred a few years back, the November contract settled at $715 per ton. Steelmaking cost structures have changed quite a bit in the last two years as has the supply landscape and sentiment in the market, so I am not suggesting this $715/ton price point is anything more than a historical anchor.

What is interesting is that, looking back over the past six years, we rarely see these lines cross. Most of the time we see them converge and then disperse. But in the last three cycles dating back to summer 2019, the bifurcation between managed money and producers’ paper positions has widened with each cycle.

All things being equal, if that trend were to occur into 2023, we would expect to see robust bids from those managed money participants looking to go long and ample liquidity for the producers looking to lay off risk by selling paper.

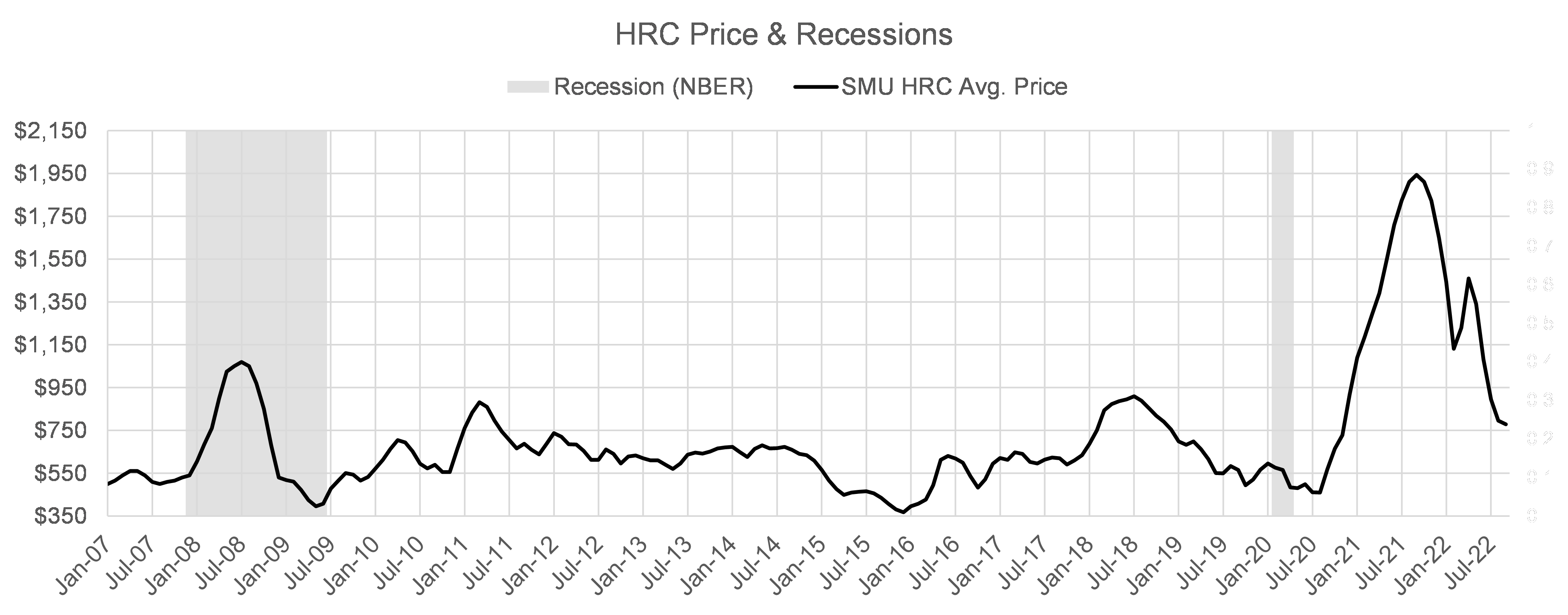

To be fair, the above comments about previous market behavior and them providing a clue toward future outcomes is tricky. Little of what we have endured over the last 2-3 years is rational or fundamental. With a hawkish Fed and recession fears raging, perhaps the last three years of trading history is not as much precedent as it is excrement. The chart below shows how HRC prices have fared during the last two recessions. 2008 was interesting in that we saw strong gains in HRC during the first part of the Great Recession. But we were also amid the Chinese-led commodity super cycle, which is not the case today. In both cases we exited those recessions with HRC prices lower than where we entered. If another recession is looming, then one must wonder how much lower HRC could go as a result.

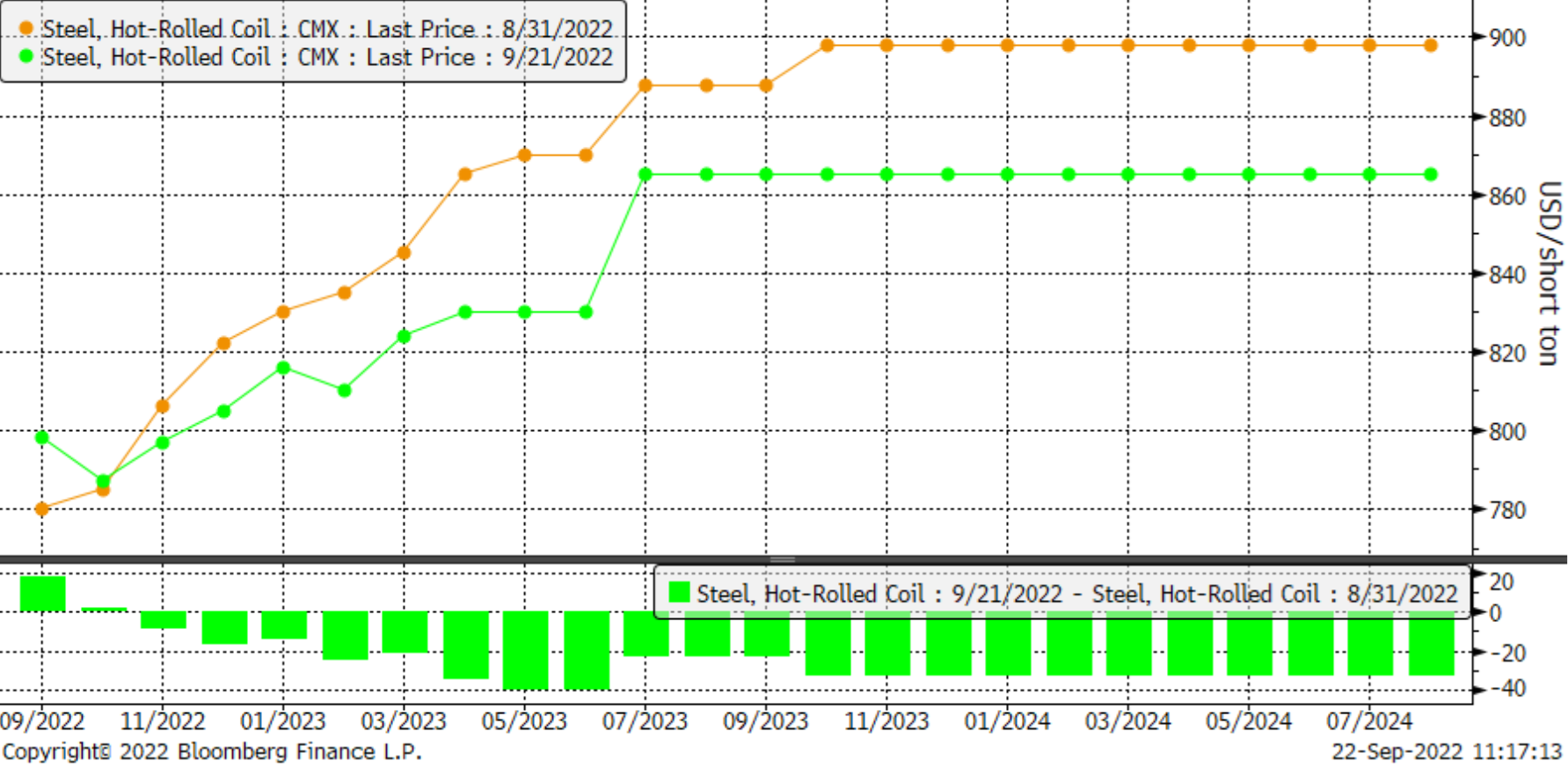

Despite the mills valiant efforts to avoid the dumpster fire that began a year ago with HRC prices falling by more than half their value, the black smoke is rising once again when looking at changes in the forward curve from the end of August to now. While the absolute dollar declines are not as significant as what was occurring all summer long, the % declines in the q2’23 and outer months are still 3+ % lower than just three weeks ago. Since April of this year, it has been a bit of a stranglehold if you have been on the long side of the HRC market.

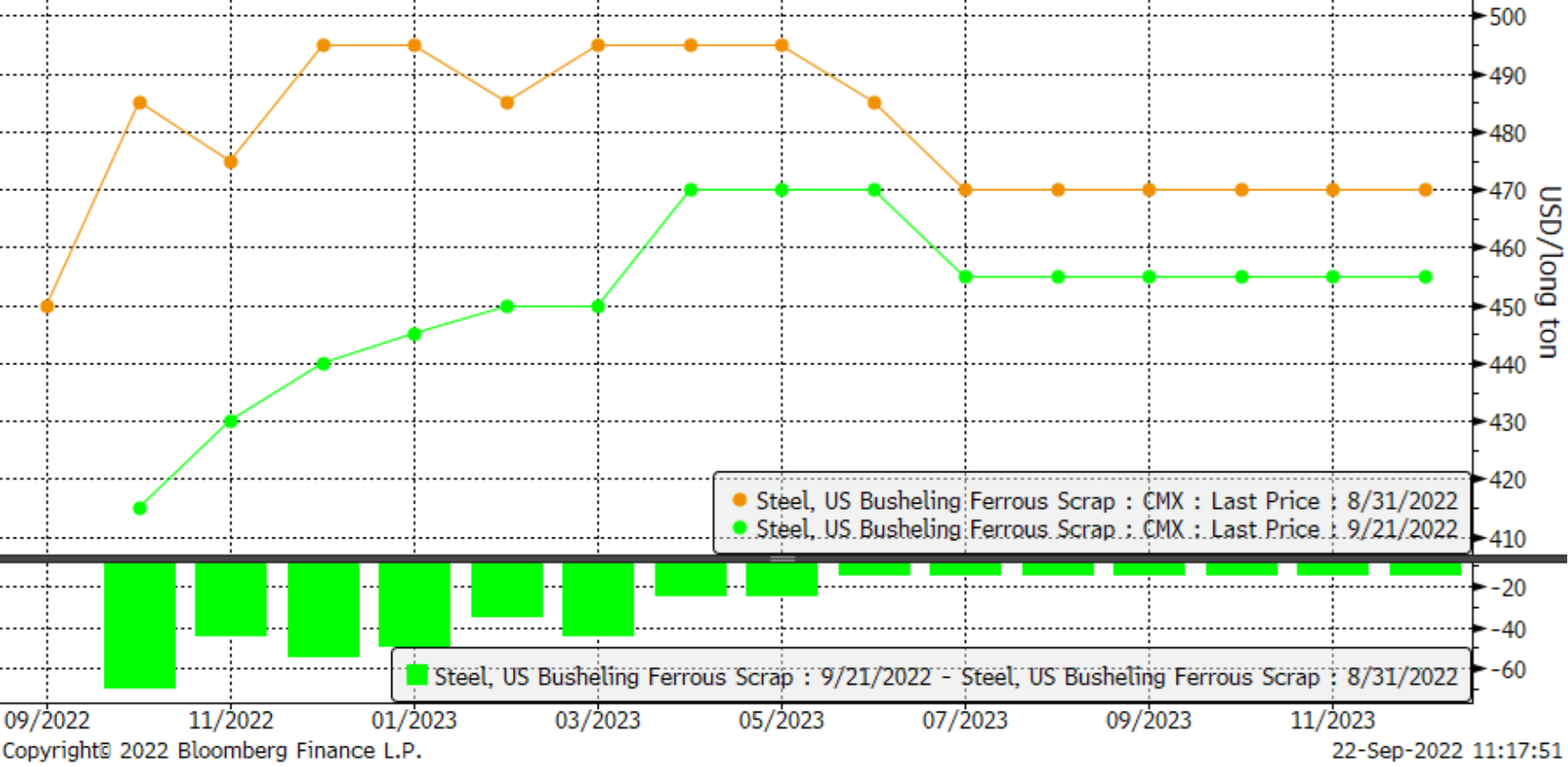

It is possible that they are taking a cue from the busheling scrap futures market outlook, which looks even worse on percentage terms as they have dropped ~10% through the January 2023 contract.

What’s going on?

It is hard to say exactly the reasons behind the continued declines in futures outside the weaker scrap outlooks. On the one hand, it does seem that some mills continue to press for orders at lower than index levels, and market participants debate whether other mills will stay unified and risk losing market share. On the other hand, the domestic mills have idled a fair bit of capacity, and there have been some recent comments about slight improvements in automotive and appliance demand. Meanwhile, energy related steel demand is as good as it has been in quite some time and service centers’ flat rolled inventories appear to be balanced, so all those things are a touch more positive than a few months ago. We do wonder how buyers behave in the fourth quarter as they inch closer to consummating new 2023 supply contracts, which could be more favorable than those concluded in 2022.

As usual we have lots of uncertainty in the market, which is why we advocate utilizing the futures market to help bring some certainty to your business.

Thanks for reading and have a great rest of the week.

Disclaimer: The information in this write-up does not constitute “investment service,” “investment advice,” or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information.