Prices

January 23, 2023

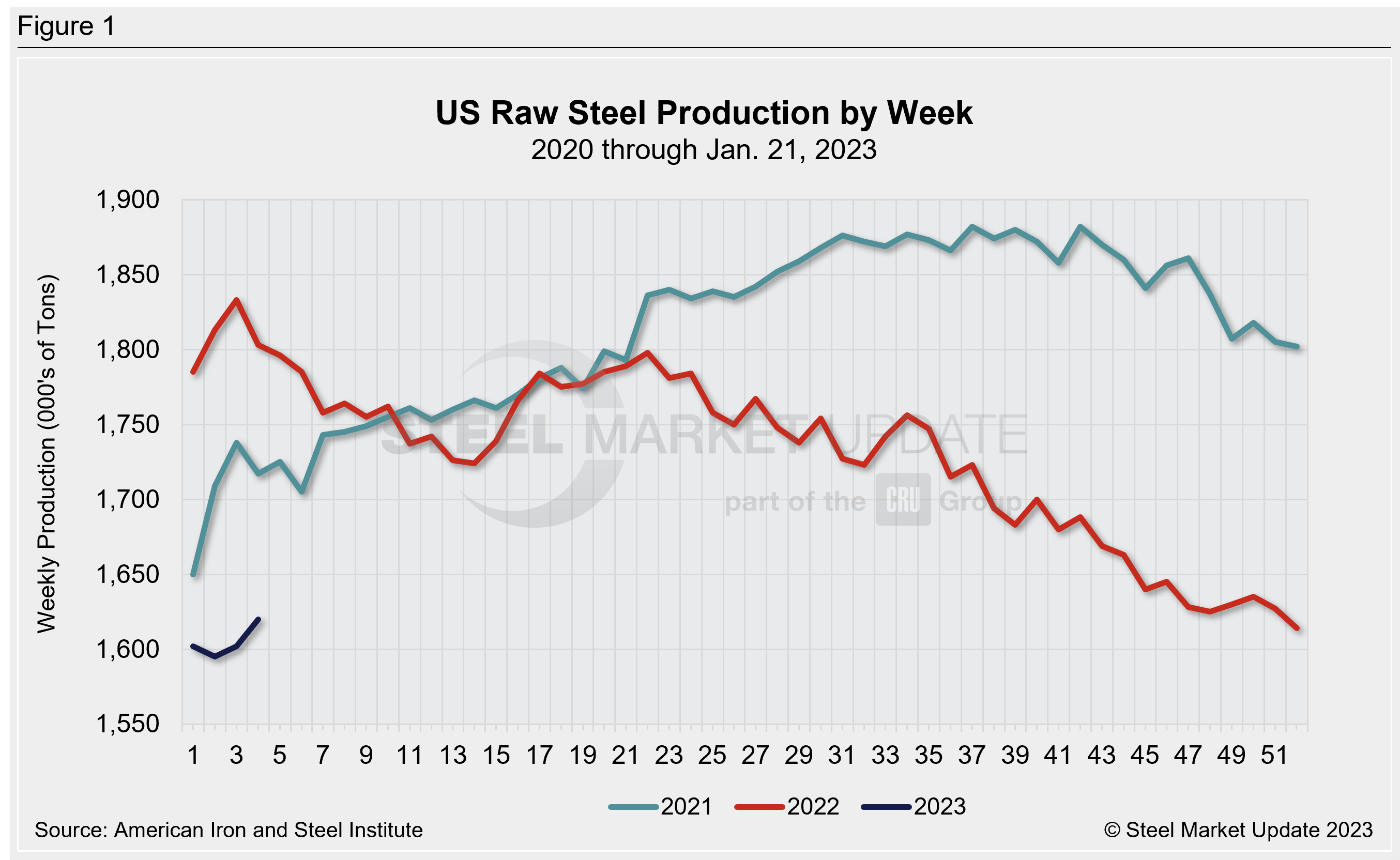

AISI: Weekly Raw Steel Output Edges Up Again

Written by David Schollaert

Raw steel production by US mills rose for the second consecutive week after falling for four straight weeks, according to data released by the American Iron and Steel Institute (AISI) on Tuesday, Jan. 23.

The increase pushed capacity utilization up to just 72.5%, driven by increases in tons in the South and Northeast regions.

Domestic mills produced 1,620,000 net tons in the week ending Jan. 21, up 1.1%, or 18,000 tons, from the previous week, and down 6.6% from 1,735,000 tons in the same week last year.

US mills ran at a capacity utilization rate of 72.5% last week, up from 71.7% the week prior, and down from 79.8% a year ago.

Adjusted year-to-date (YTD) production through Jan. 21 was at 4,817,000 tons, with YTD capacity utilization at 71.8%. That’s 7.5% below the 5,206,000 tons in the same YTD period in 2022 when capacity utilization was 79.8%, AISI said.

Production by region for the week ending Jan. 21 is below. (Note: week-over-week change is in parentheses.)

- Northeast, 127,000 tons (up 3,000 tons)

- Great Lakes, 524,000 tons (down 22,000 tons)

- Midwest, 202,000 tons (down 3,000 tons)

- South, 681,000 tons (up 24,000 tons)

- West, 68,000 tons (down, 2,000 tons)

Note: The raw steel production tonnage provided in this report is estimated. The figures are compiled from weekly production tonnage provided by approximately 50% of the domestic production capacity combined with the most recent monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The AISI production report “AIS 7,” published monthly and available by subscription, provides a more detailed summary of steel production based on data supplied by companies representing 75% of US production capacity.

By David Schollaert, david@steelmarketupdate.com