Prices

February 27, 2023

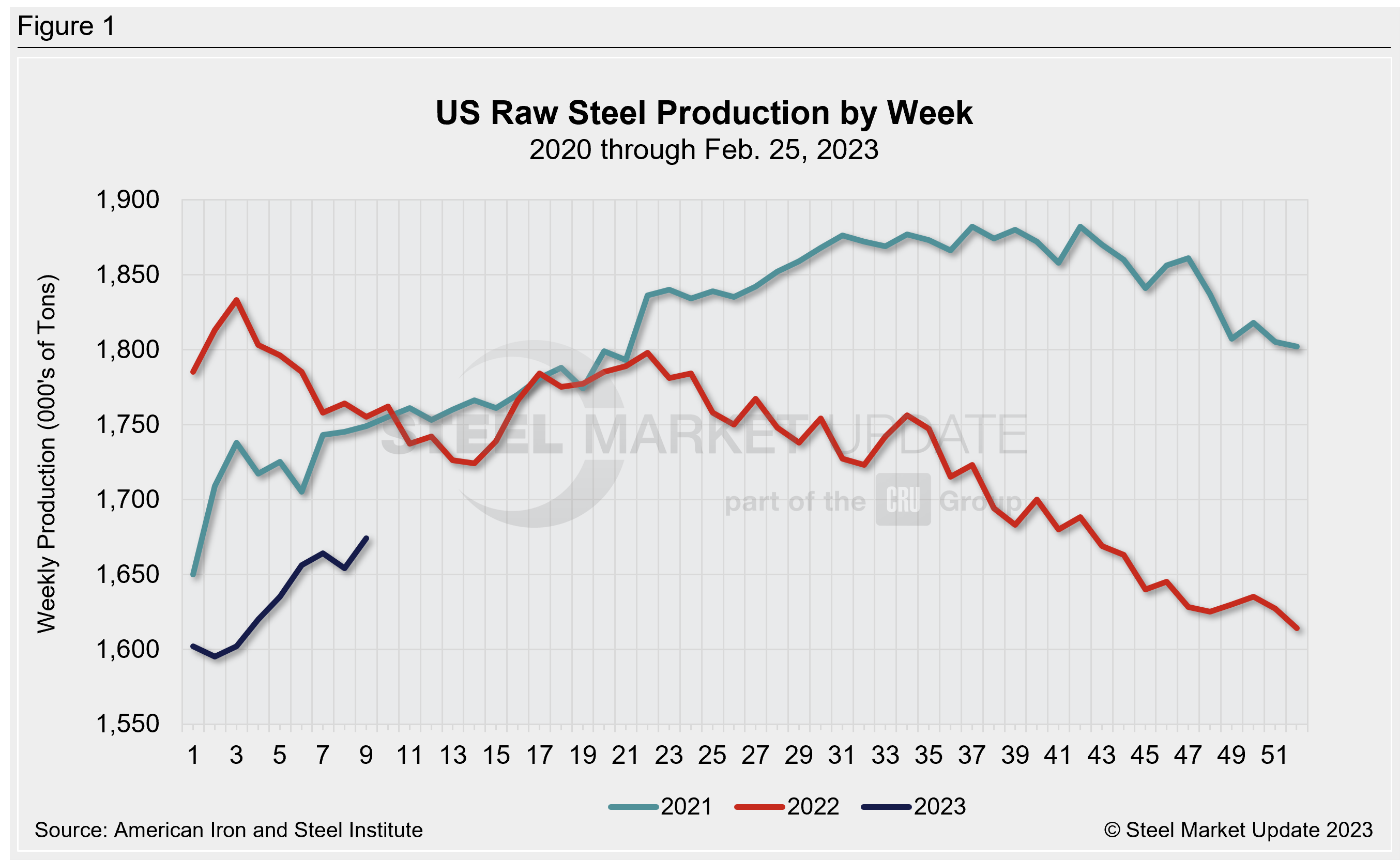

Weekly Raw Steel Production Rebounds: AISI

Written by David Schollaert

Raw steel production by US mills recovered last week after declining slightly the week prior, according to data released by the American Iron and Steel Institute (AISI) on Monday, Feb. 27.

The increase pushed capacity utilization up to 74.9%, driven by gains in tons in all regions except for the Northeast. This is up from the prior week’s 74%, but down from 80.8% a year ago.

Domestic mills produced 1,674,000 net tons in the week ending Feb. 25, up 1.2%, or 20,000 tons, from the previous week, but down 4.6% from 1,755,000 tons in the same week last year.

Adjusted year-to-date (YTD) production through Feb. 25 stood at 13,100,000 tons, with YTD capacity utilization at 73.2%. That’s 6.1% below the 13,854,000 tons in the same YTD period in 2022 when capacity utilization was 80.3%, AISI said.

Production by region for the week ending Feb. 25 is below. (Note: week-over-week change is in parentheses.)

- Northeast, 146,000 tons (down 8,000 tons)

- Great Lakes, 520,000 tons (up 8,000 tons)

- Midwest, 209,000 tons (up 7,000 tons)

- South, 732,000 tons (up 8,000 tons)

- West, 67,000 tons (up 5,000 tons)

Note: The raw steel production tonnage provided in this report is estimated. The figures are compiled from weekly production tonnage provided by approximately 50% of the domestic production capacity combined with the most recent monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The AISI production report “AIS 7,” published monthly and available by subscription, provides a more detailed summary of steel production based on data supplied by companies representing 75% of US production capacity.

By David Schollaert, david@steelmarketupdate.com