Overseas

March 25, 2023

Worldsteel: Global Steel Output Edges Down in February

Written by David Schollaert

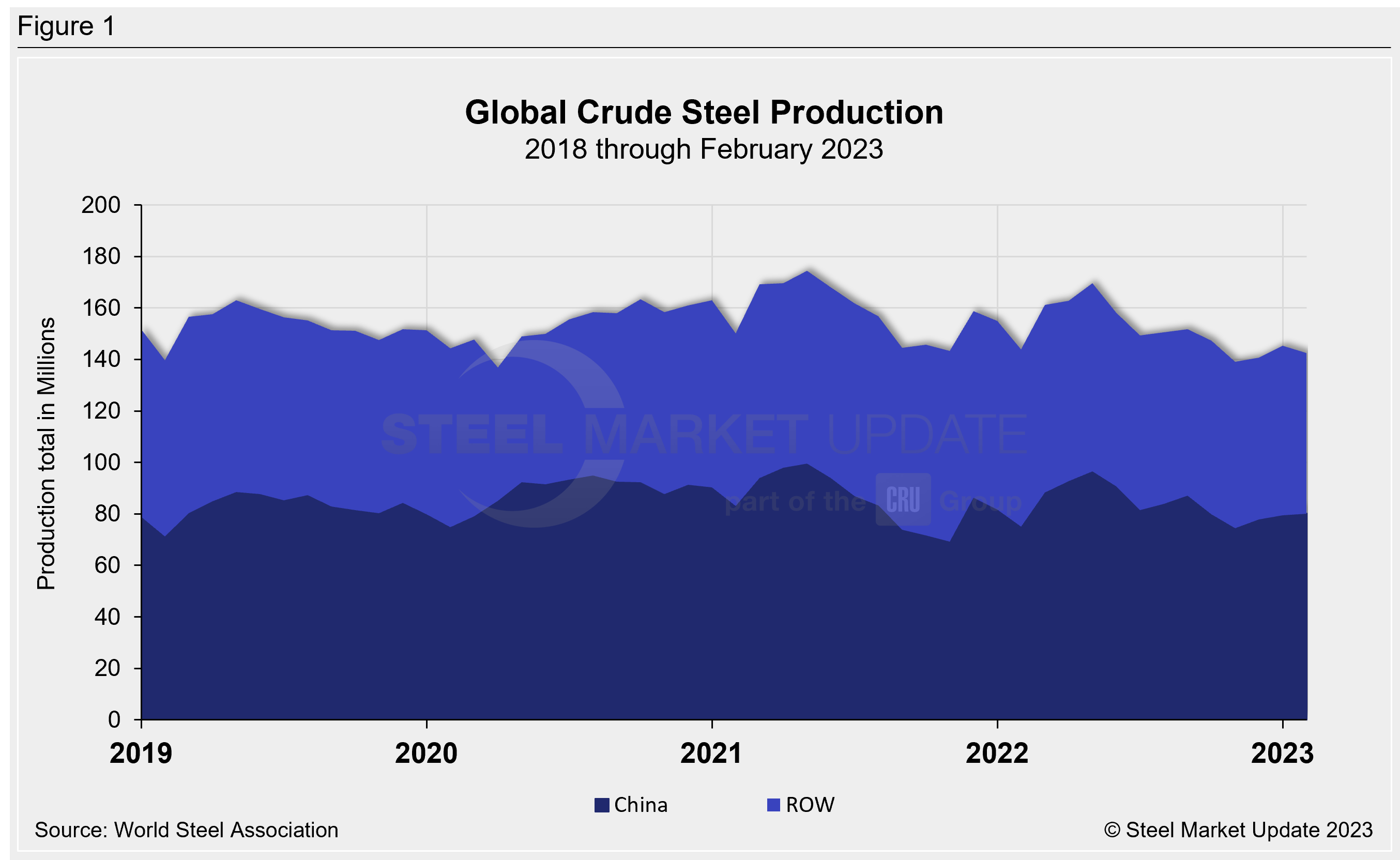

Global crude steel production was estimated at 142.3 million metric tons in February, as steelmakers around the world cut output by 1.4 million metric tons vs. the same year-ago period, the World Steel Association (worldsteel) reported.

Last month’s estimated production was also down sequentially, declining 2%, or 2.9 million metric tons, from January’s total crude steel output.

After reaching an all-time high of 174.4 million metric tons in May 2021, global steel output has varied. The lack of consistency has been heavily determined by Chinese production. After slipping to the lowest total in nearly three years in November, Chinese raw steel output has risen repeatedly since.

And while Chinese production has been on the rise, overall global output has now dipped repeatedly over the past three months.

Last month eight of the top 10 steel-producing nations saw production declines vs. January.

When compared to the same year-ago period, results were similar. Again, only two out of 10 saw production totals increase — China and South Korea were the exceptions. When compared to the pre-pandemic period of February 2019, global crude steel production was up 2%, or 2.77 million metric tons, last month.

China’s steel production in February totaled an estimated 80.1 million metric tons, up 600,000 metric tons (+0.8%) MoM, and up 5.1 million metric tons (+6.8%) from the same year-ago period. Worldwide steel production, ex-China, totaled 62.3 million metric tons last month, down 3.5 million metric tons (-5.3%) compared to January. Output was also down 9.4%, or 6.5 million metric tons fewer vs. February 2022.

Chinese steel output accounted for 56.3% of worldwide production in February, up 1.5 percentage points vs. January.

The US saw output decrease by 500,000 metric tons, or -7.7% last month.

By David Schollaert, david@steelmarketupdate.com