Canada

March 31, 2023

Rig Counts Down in US and Canada

Written by Becca Moczygemba

Rig counts are down in the US and Canada this week, according to the latest data from oilfield services company Baker Hughes.

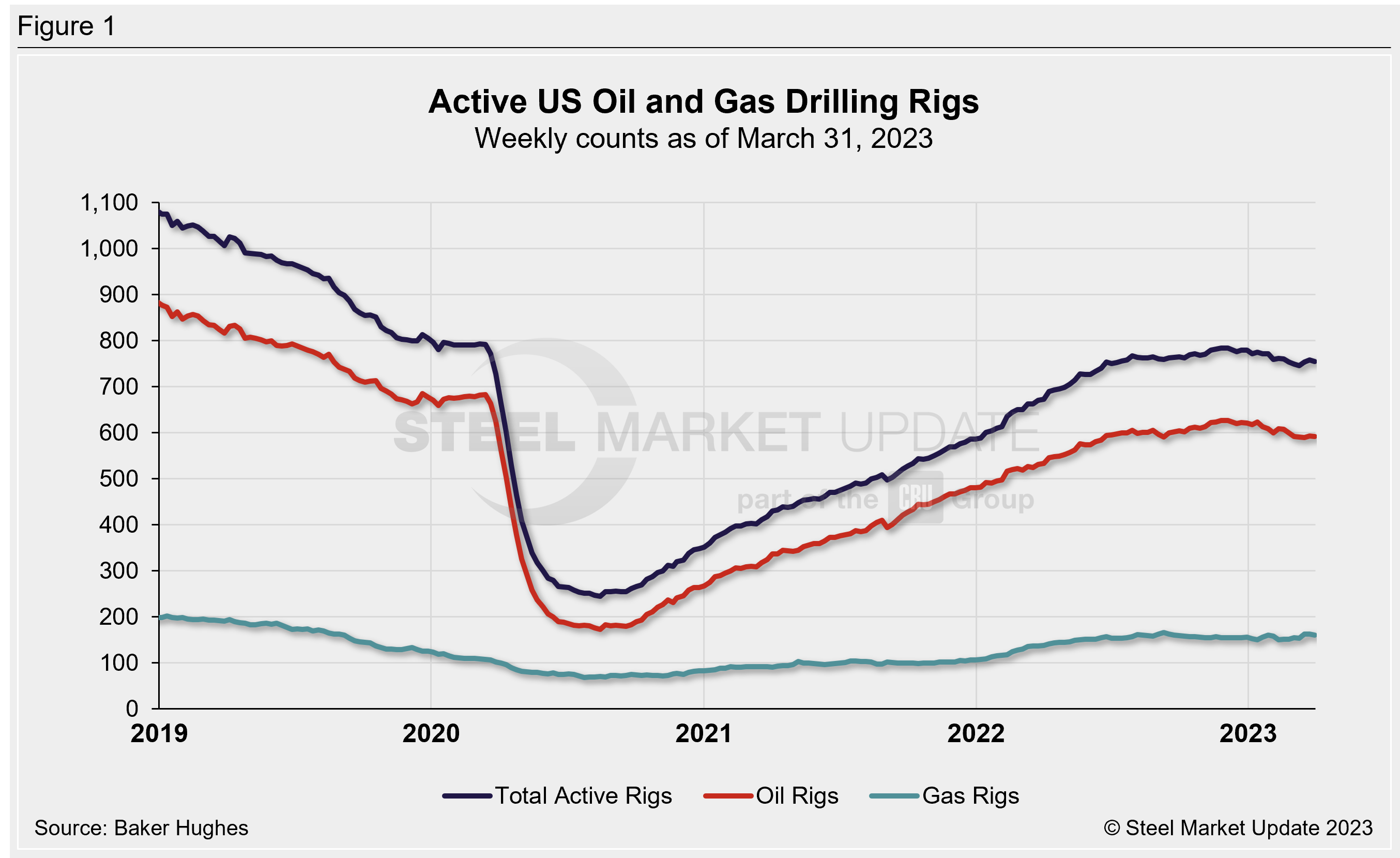

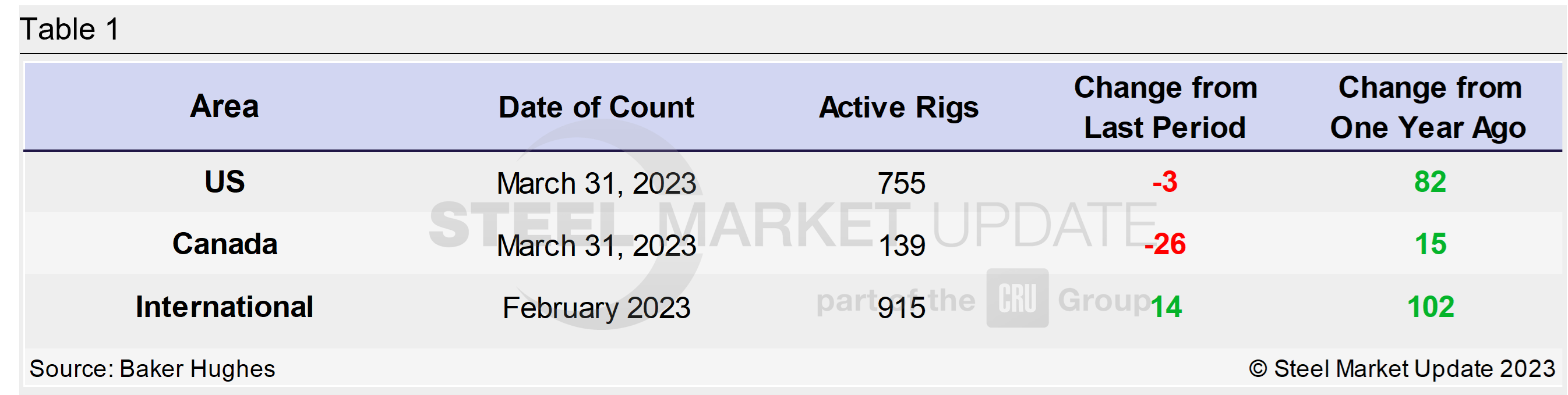

The total US rig count was 755 for the week ended March 31, down three rigs from the week prior. The number of active oil rigs in the US dropped by one from the prior week’s 593. The number of gas rigs fell by two to 160. Compared to this time last year, the US count is up by 82 rigs, with oil rigs up 59, gas rigs up 22, and miscellaneous rigs up one, respectively.

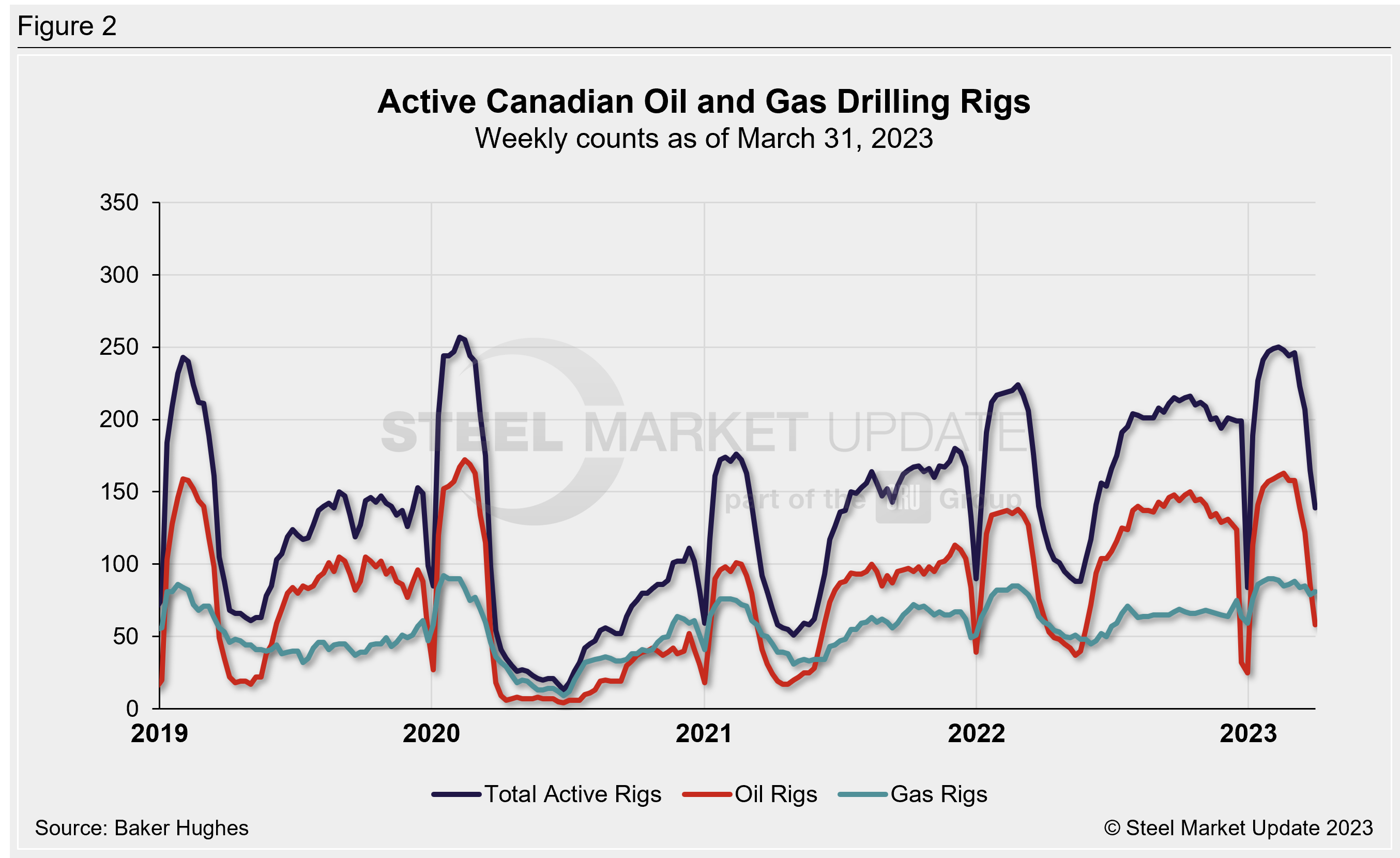

The total number of active Canadian rigs fell to 139 this week, down by 26 from the previous week. Oil rigs in Canada dropped to 58 from 86, while gas increased from 79 to 81. The Canadian count is up by 15 rigs compared to last year, with oil rigs accounting for most of those gains.

The international rig count increased by 14 to 915 rigs for the month of February vs. the prior month and is up by 28 rigs from the same month last year.

The number of oil and gas rigs in operation is important to the steel industry because it is a leading indicator of demand for oil country tubular goods (OCTG), a key end-market for steel sheet.

A rotary rig is one that rotates the drill pipe from the surface to either drill a new well or to sidetrack an existing one. Wells are drilled to explore for, develop, and produce oil or natural gas. The Baker Hughes Rotary Rig count includes only those rigs that are significant consumers of oilfield services and supplies.

Steel Market Update regularly publishes an in-depth “Energy Update” report covering oil and natural gas prices, detailed rig count data, and oil stock levels. That is available here for Premium members.

For a history of both the US and Canadian rig count, visit the Rig Count page on the Steel Market Update website here.

By Becca Moczygemba, becca@steelmarketupdate.com