Market Data

July 6, 2023

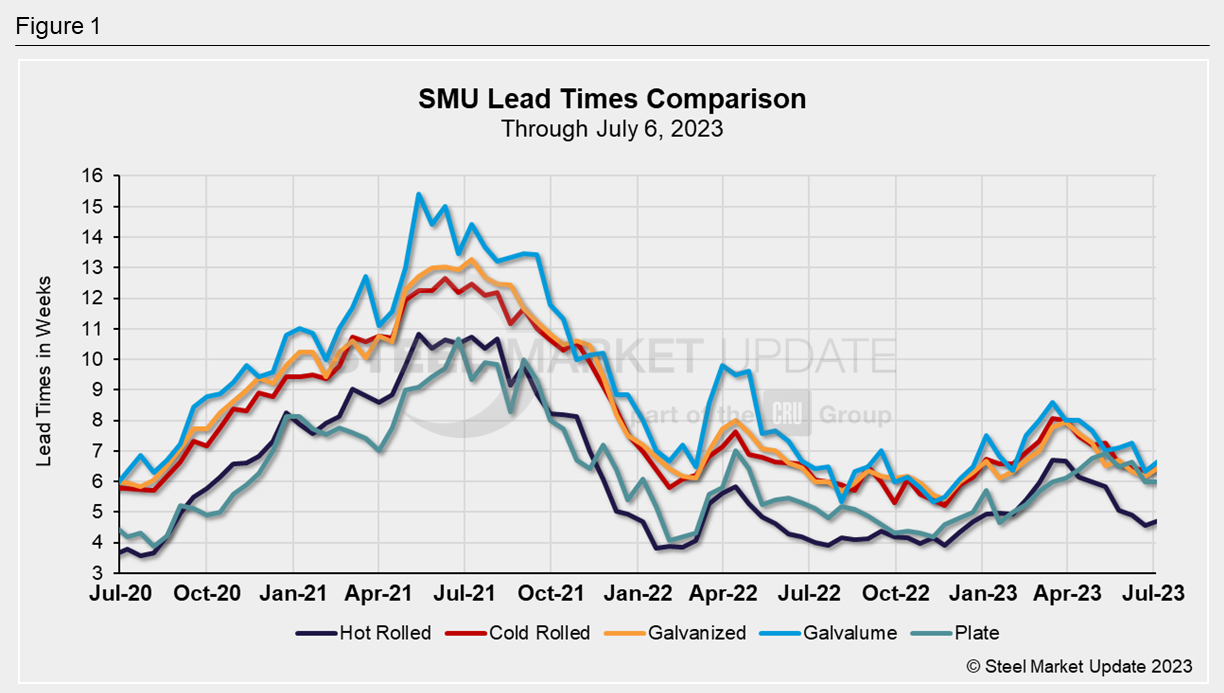

Sheet Lead Times Rise Modestly, Plate Unchanged

Written by Laura Miller

Lead times were broadly stable this week, with sheet products rising modestly and plate unchanged from SMU’s market check two weeks ago.

More meaningful movements in lead times should be seen in the coming weeks as buyers return to the market after the Fourth of July holiday. Should the mills’ recent sheet price hikes take hold, we should see lead times begin to extend. We’ll poll buyers again two weeks from now and keep you updated on what the market is seeing.

Are you a steel buyer interested in sharing the numbers you’re seeing and hearing with SMU? Reach out to david@steelmarketupdate.com to take part in our weekly surveys.

Steel buyers this week reported lead times ranging from 3 to 6 weeks for hot rolled, with an average of 4.71 weeks. This was an extension of 0.15 weeks from the 26-week low of 4.56 weeks registered in the market check two weeks ago.

Lead times of 5 to 9 weeks were reported for cold-rolled sheet this week, with an average time of 6.42 weeks. This was stable from the 6.36 weeks reported two weeks prior and the 6.46 weeks reported a month earlier.

For galvanized sheet, lead times were said to be between 5 and 8 weeks, with an average of 6.45 weeks as of July 6. Galvanized lead times lengthened by 0.26 weeks from SMU’s market check two weeks ago and have been between 6 and 7 weeks since early May.

Lead times for Galvalume averaged 6.67 weeks, with buyers reporting times between 4 and 9 weeks. Lead times were 0.34 weeks higher than the June 22 market check.

Plate lead times, meanwhile, were unchanged at 6.0 weeks this week, with buyers reporting times between 4 and 8 weeks. Lead times for plate have been averaging between 6 and 7 weeks since mid-March.

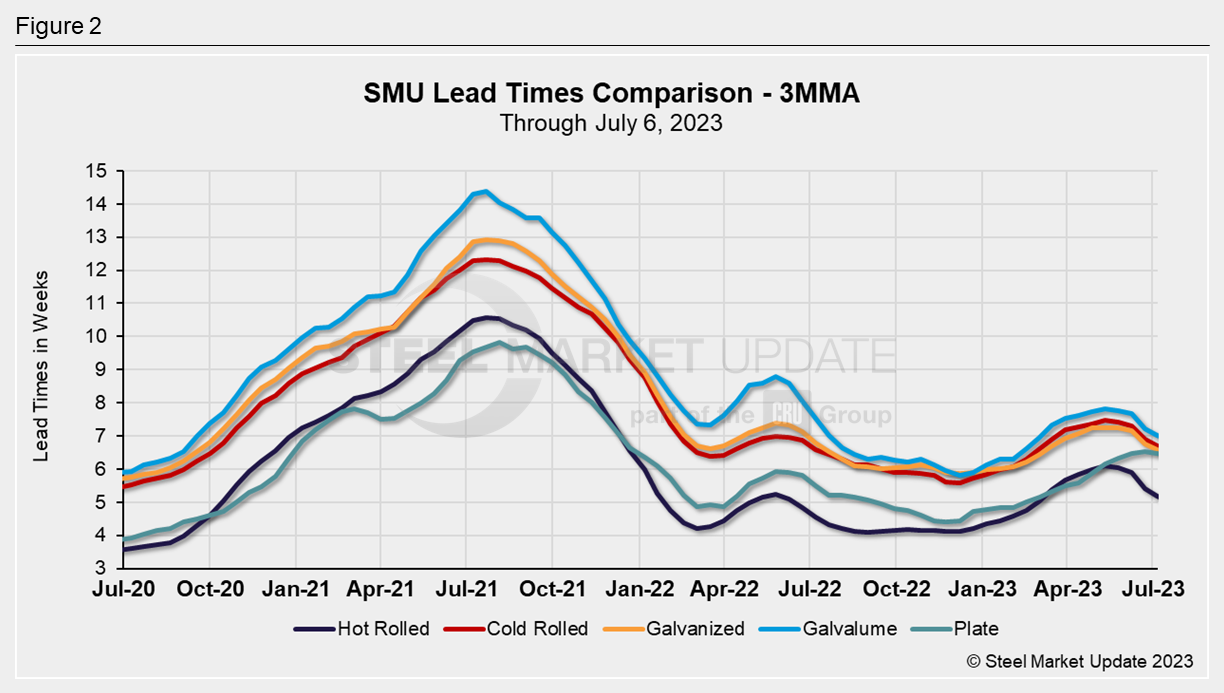

Looking at lead times as three-month moving averages (3MMA) can smooth out the variability in SMU’s biweekly readings.

For hot rolled and cold rolled lead times, the 3MMAs fell back for a fourth consecutive market check, while those for galvanized and Galvalume declined for a third consecutive check.

The 3MMA for plate lead times has been steady at 6.5 weeks since early June and has been above the 6.0-mark since early May.

Over 72% of steel buyers surveyed this week predicted lead times will be flat two months from now – that’s up from 64% two weeks ago. Almost 17% predict lead times will be contracting, while 11% believe they will be extending.

As one buyer put it, lead times will be “‘Flat,’ but flat at 3-4 weeks is a problem.”

Another buyer predicted lead times will have already extended and will be flattening two months from now.

Still another buyer said they anticipate lead times will be extending “slightly and gradually,” noting that flat-rolled imports are down year-to-date vs. 2022 and that “will be felt by late summer.”

Note: These lead times are based on the averages from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. SMU measures lead times as the time it takes from when an order is placed with the mill to when the order is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier, so look to your mill rep for actual lead times. To see an interactive history of our Steel Mill Lead Times data, visit our website.

By Laura Miller, laura@steelmarketupdate.com