CRU

November 15, 2024

CRU: Sheet prices hit bottom in Europe, pressure in other markets

Written by Ryan McKinley

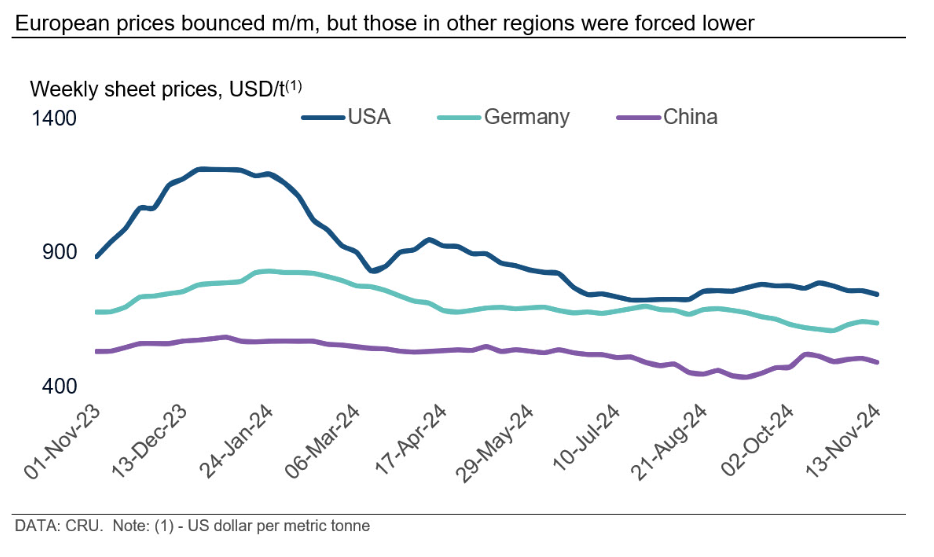

The CRUspi was essentially unchanged m/m, edging 0.6% lower in November to 175.2. Price rises in Europe mostly offset declines in Asia and North America, although demand remains weak across all these regions.

Sheet prices in Europe managed to rebound this month after import offers lost their attractiveness and some positional buying occurred. However, this was not the case in North America or Asia. In North America, demand remains weak, and inventories are too high to support price increases, even following the decisive conclusion of the US election. Prices in Asia also drifted lower after uncertainties about newly announced stimulus measures in China led to a gradual decline in spot buying, although there was an unusual rise in prices in India.

While stockholders in Europe do not appear to have any immediate need to restock, we understand some in Northern Europe took positions after it appeared prices had bottomed in Asia. However, this price uptrend in Northern Europe was far weaker in Italy, and rises were constrained by intense competition between service centers for market share and an increase in imports following the opening of the Q4 quota period last month.

Chinese prices fell m/m after a spike driven by the announced stimulus measures earlier this year faded. This sharp increase had taken some by surprise, and many traders reduced purchases from mills and lowered prices in an effort to destock. Pushback on higher prices from end users also helped facilitate price falls. However, the Indian market was unusually strong following a relatively weak October.

US prices again came under pressure from weakening demand during a time when capacity is rising. Despite a small uptick in orders following a strong win by the Republican party during the recent elections, inventory levels are too high relative to demand for mills’ price increase attempts to gain traction. In fact, many mills continued to offer steeply discounted prices in order to secure deals, particularly for large-volume orders.

Editor’s note: This article was first published by CRU. To learn more about CRU’s services, click here.