Analysis

December 12, 2025

CRU: Data center demand drives US rebar toward June 2023 highs

Written by Alexandra Anderson

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

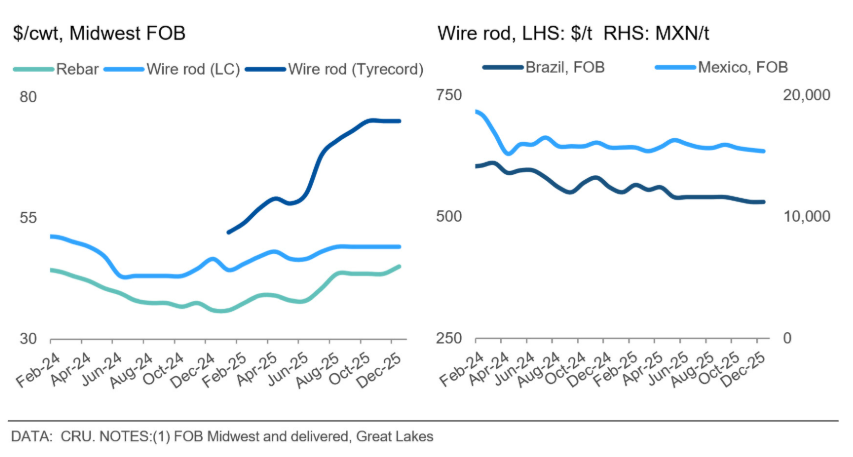

US longs prices diverged in early December, with rebar and structurals prices rising on data center demand while wire rod remained flat, as domestic mills balanced the market. Import volumes, in November, declined sharply across all longs.

Rebar prices increased following mill announcements in early November, approaching $1,000/metric ton mark, the highest level since June 2023. Fewer imports and higher demand for domestic material extended lead times as mill order books filled.

The market benefited from infrastructure activity surrounding AI data centers, although some market participants questioned the sustainability of this demand. Mills also increased structurals prices as supply tightness and strong data center-related end-use demand put upward pressure on the market.

Wire rod prices remained flat m/m as end-use consumption lagged rebar and beams. However, significantly reduced imports have supported demand from domestic mills. The rise in infrastructure activity has also supported HC wire rod, but LC and tyrecord demand have slowed seasonally. Buyers noted that international tyrecord suppliers sought to push prices higher based on increased freight costs but were unsuccessful. Scrap prices were flat in November, limiting the opportunity for mills to justify any cost-related price increases.

While the US Department of Commerce has updated import statistics from the government shutdown period, final data is not yet available. Thus far, US import license data have shown sharp declines in long products in November. Rebar imports fell to approximately 31,000 mt, down from 51,000 mt in October, with material primarily sourced from Turkey and Brazil, according to the US Department of Commerce. Wire rod import licenses declined 94% m/m to approximately 39,000 mt in November.

In Brazil, domestic long prices are stable m/m. According to IABr, longs production increased by 5.9% m/m in October but was down by 4.5% y/y. Year-to-date cumulative production volume continued to trend down and is currently flat y/y. In terms of trade, imports increased by 45% m/m in October but were 11% lower y/y. With this lower y/y volume, the accumulated year-to-date import volumes continue to decrease and are currently 4% lower y/y. The main sources of imports were China, Egypt and Russia. After three months of lower volumes, imports from Egypt increased again in October.