CRU

May 1, 2026

CRU: Iron ore firms on high freight costs

Written by Yusu Mao

This item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

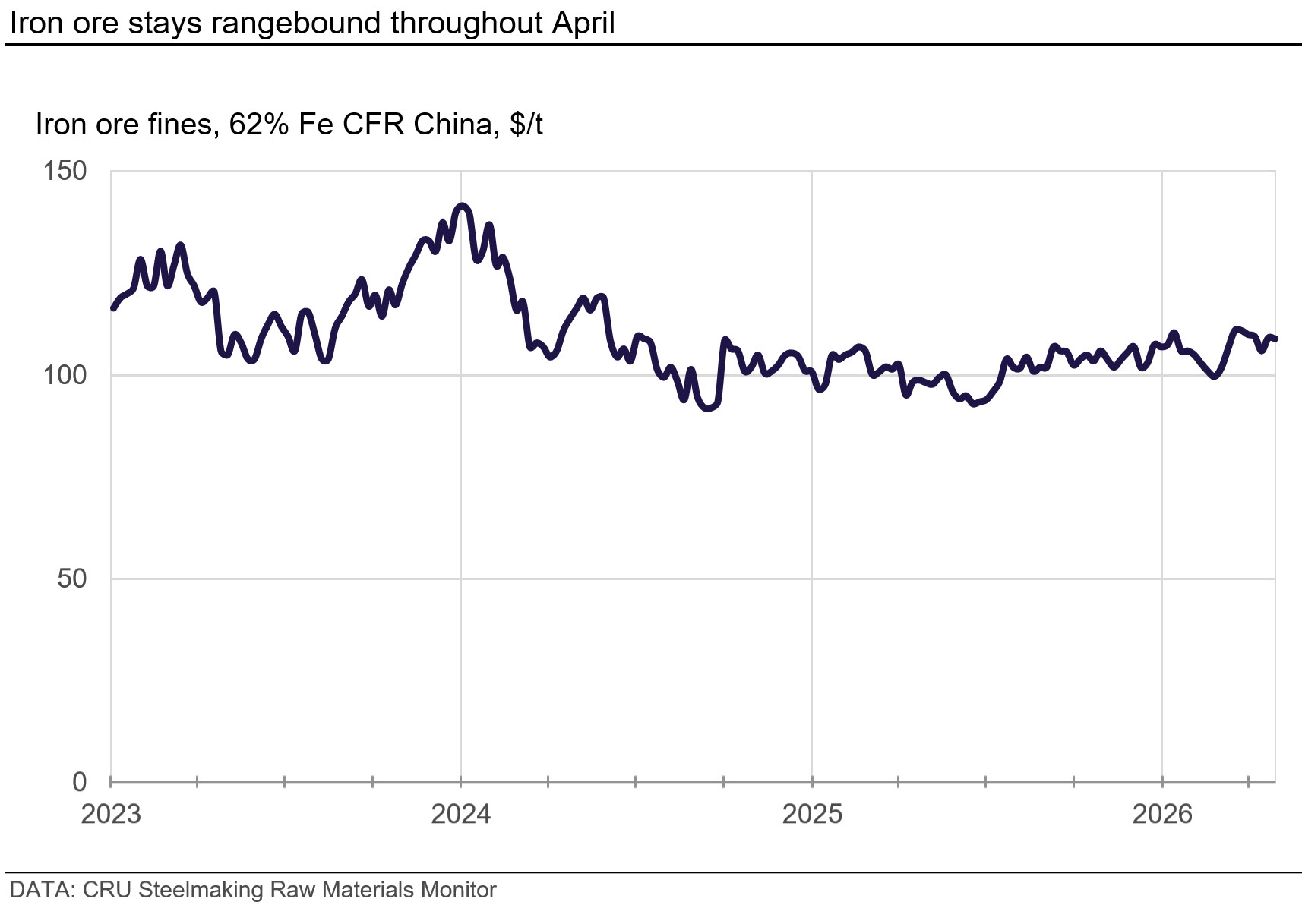

In April, iron ore prices remained rangebound in the $105–110 per dry metric ton (dmt) range for 62% Fe fines, following the surge in the first half of March. While news of an agreement between BHP and CMRG has eased supply concern and caused prices to edge lower, robust iron ore consumption in China and elevated freight costs continue to support iron ore prices.

Higher bunker prices underpin iron ore prices

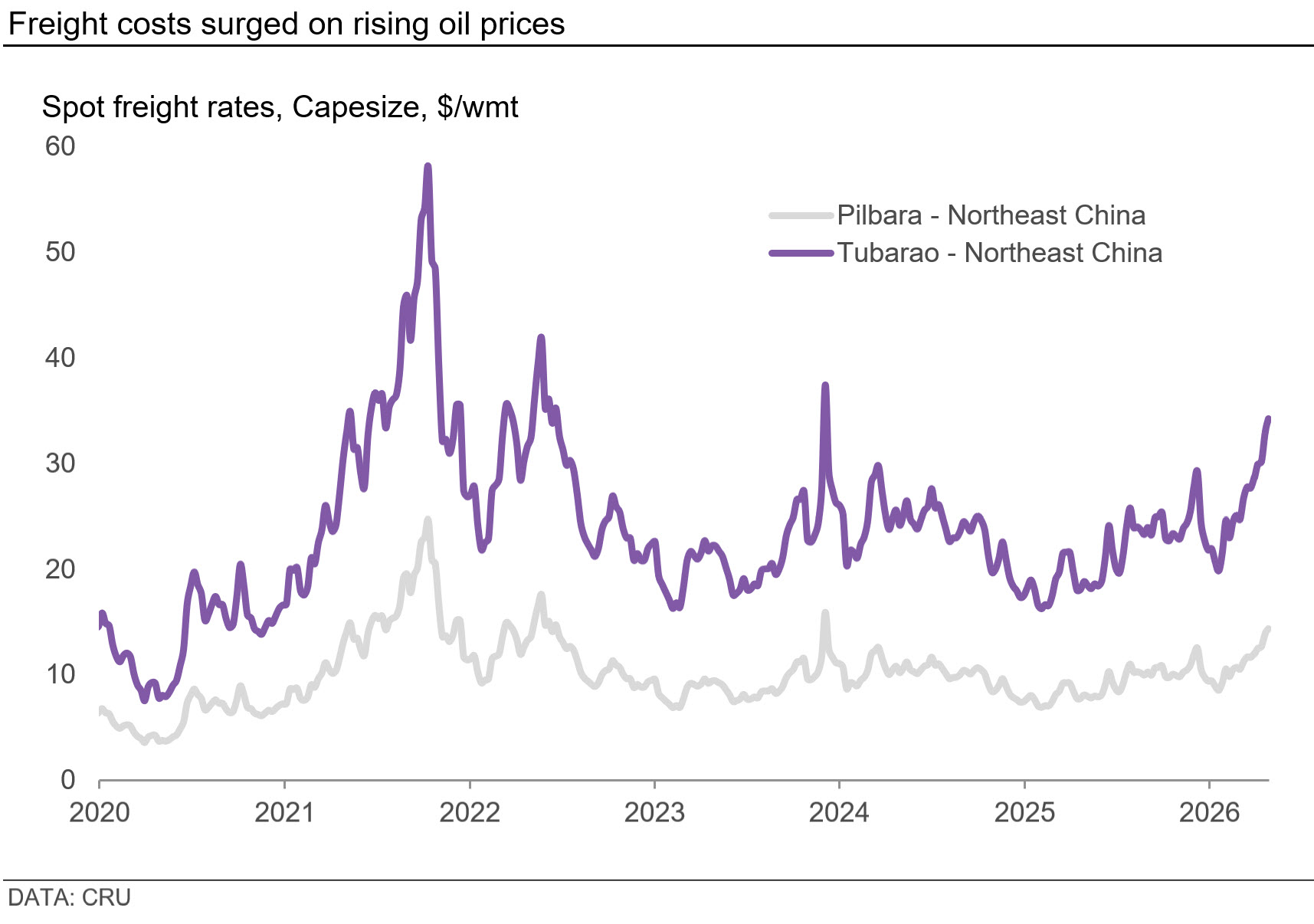

Brent crude oil prices continued to climb, jumping up to a four-year high of over $125 per barrel on April 30 amid deepening concerns over a prolonged closure of the Strait of Hormuz. Higher oil prices have cascaded into skyrocketed bunker fuel costs, and freight costs for both Brazil-China and Australia-China routes rose to the highest levels since end-2023.

In addition to sea freight, high energy prices are also feeding through to:

• Higher diesel costs, a significant input for open-pit miners and producers that truck ore to port

• Higher gas prices that raise the costs of processing iron ore

The impact of cost inflation has been disproportionate across regions. Producers with greater exposure to sea freight, particularly those shipping over longer distances to key markets, have been the most affected, including West Africa, Cananda and Brazil. Continued freight increases will put supply from Brazilian junior miners under growing pressure. While Australian producers face less freight cost pressure, diesel shortages become a real risk for operators rely on trucks to haul ore to ports.

Major producers maintain strong shipment volumes

Iron ore supply increased seasonally in April, with robust shipments across major producers keeping the market well-supplied. In Australia, Rio Tinto maintained strong shipments following solid performance in Q1. Higher production relative to shipments imply that the company has built up inventories and will sustain strong deliveries into Q2. Port Hedland shipments were broadly steady year over year (y/y) in April, with higher volumes from BHP and Fortescue who are also on track with strong performance in Q2, partially offset by reduced shipments from Roy Hill due to maintenance.

Brazilian April shipments rose both month over month (m/m) and y/y, supported by increased volumes from southern Brazil, mainly Vale and CSN with ample low-grade high-silica supply. While there are signs that buying appetite in China is shifting to higher-grade materials, both producers are well-positioned to supply. Vale, with its own vessels and backward freight pricing, faces much less pressure from freight surge. For CSN, CRU’s iron ore team learned from a recent trip to Brazil that the company has high operating flexibility with blending, although high freight remains a concern.

Simandou shipped six vessels in April, totaling 2.8 million metric tons year to date in 2026. Despite the pick-up in April compared to January–March, shipment volumes still largely lag behind the target, especially that Guinea is entering the rain season in May. Shipments will begin to face more weather-related disruptions.

Chinese buying activity holds firm ahead of May holiday

Iron ore consumption in China increased on strengthening hot metal production, underpinned by a seasonal recovery in domestic steel demand. Buying activity has remained solid with steelmakers maintaining their usual pace of iron ore procurement, which has increased with restocking activity ahead of the May 1-5 holiday. Slightly slower import arrivals and increased portside transactions led iron ore port inventories to trend lower from an elevated level throughout April, although remaining largely above prior-year levels.

Market contacts indicate that mills in China are increasingly shifting towards medium- and high-grade ores. Rising coal prices prompted discussions about another coke price increase. Together with improving mill margins, steel producers will prefer higher-grade ores, including concentrate and pellet feed, to reduce fuel consumption and increase productivity. Lump demand has also improved as it became more cost competitive compared to other products.

Prolonged conflict drives forecast upgrade on cost pressures

CRU’s iron ore price forecast has been upgraded for the rest of 2026, and we now expect prices to average $104/dmt for the full year, reflecting higher-than-expected energy prices due to the prolonged conflict in the Middle East. Two months of Strait of Hormuz closure and halted shipments within the Persian Gulf mean that DRI producers are running out of pellet stocks and facing increasing risks of halting operations. As a result, pellet restocking once the strait reopens is expected to provide meaningful support to pellet premium.