Analysis

May 8, 2026

CRU Auto Outlook: Cost pressures rise in auto industry

Written by David Leah

Key takeaways

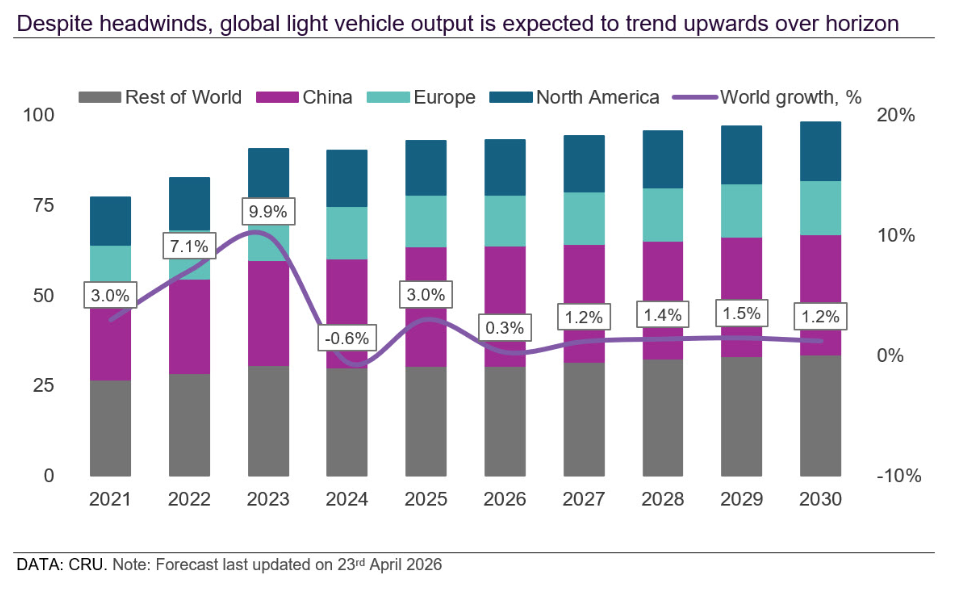

- Global production: Growth is set to be flat this year, with recent downgrades driven mainly by Europe, where expected demand-side headwinds, alongside ongoing cost, regulatory, and competitive pressures, have softened the outlook. Chinese automotive production was also revised down modestly on weaker domestic demand, reflecting policy and structural changes. While North America was broadly unchanged, it remains exposed to downside risk from weaker domestic demand.

- EV demand: While we expect a rebound, EV growth in China has been weak so far this year, held back by tighter incentives and regulations, as well as holiday-related timing distortions. North American EV sales appear to have bottomed out, with US BEV sales still weak, although there are more positive signs in Canada and Mexico, but we expect regional EV sales to contract this year. In contrast, EV sales in Europe remain strong, supported by increased competition, new model launches, and regulatory standards, leading to a modest upgrade to the EV outlook.

- Key risks: Multiple risks continue to cloud the automotive outlook, including semiconductor shortages, tariff uncertainty, weaker demand, policy changes, geopolitical disruption, the war in Iran, supply-chain shocks, protectionism, cost pressures, and intensifying competition. Overall, risks to production remain skewed to the downside, led by softer domestic demand in China and a subdued outlook in North America and Europe, and the ongoing conflict in the Middle East. In addition, rising material prices remain a concern.

OEMs are facing rising material prices

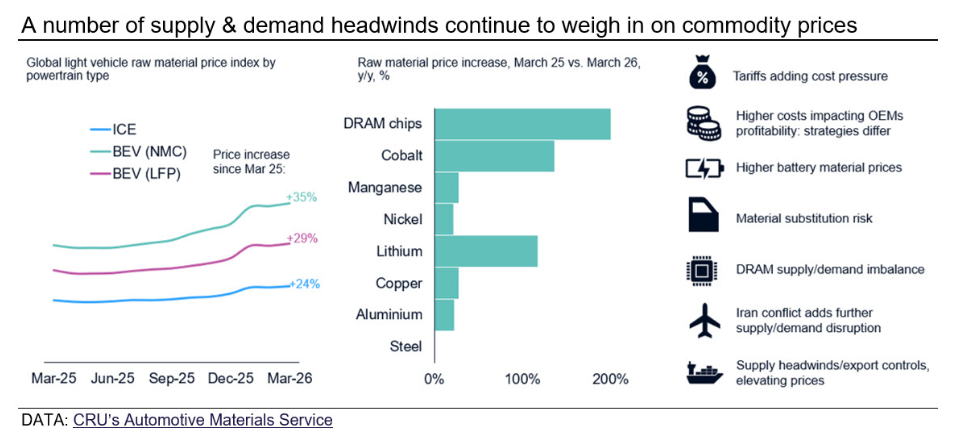

Compared with last year, prices across a number of commodities have risen substantially, increasing vehicle material costs. The increase is more pronounced for electric vehicles, given the rise in prices for several battery-related materials, driven by a combination of demand-side and supply-side factors. In addition, aluminum and copper prices have risen sharply, which disproportionately affects battery electric vehicles on average, given their higher content of these materials relative to ICE vehicles.

As a result, OEMs are facing additional cost pressure, with a number of them flagging higher material prices as a drag on margins in recent quarterly investor updates. While OEMs are often not directly exposed to spot prices, as they also tend to source materials through longer-term contracts and supplier arrangements, if material prices remain elevated for longer, they are likely to become more exposed, which could in turn lead some to pass higher costs on to consumers.

However, strategies differ. We have seen some OEMs pass on higher costs for select models or trims, while others are more likely to absorb the costs to avoid losing sales and market share. Over the longer term, this could influence OEM decision-making, with potential substitution effects across certain materials, greater material thrifting, and reduced part counts on selected components such as semiconductors to help mitigate price increases and cost pressure.

While there are signs that prices for some commodities may ease over the short to medium term, downside risk remains, particularly if the Iran conflict becomes protracted or if other supply-demand imbalances persist.

All of these factors and trends are covered in CRU’s latest Automotive Materials Service.

For more information or to request a demo of the new service, please get in touch

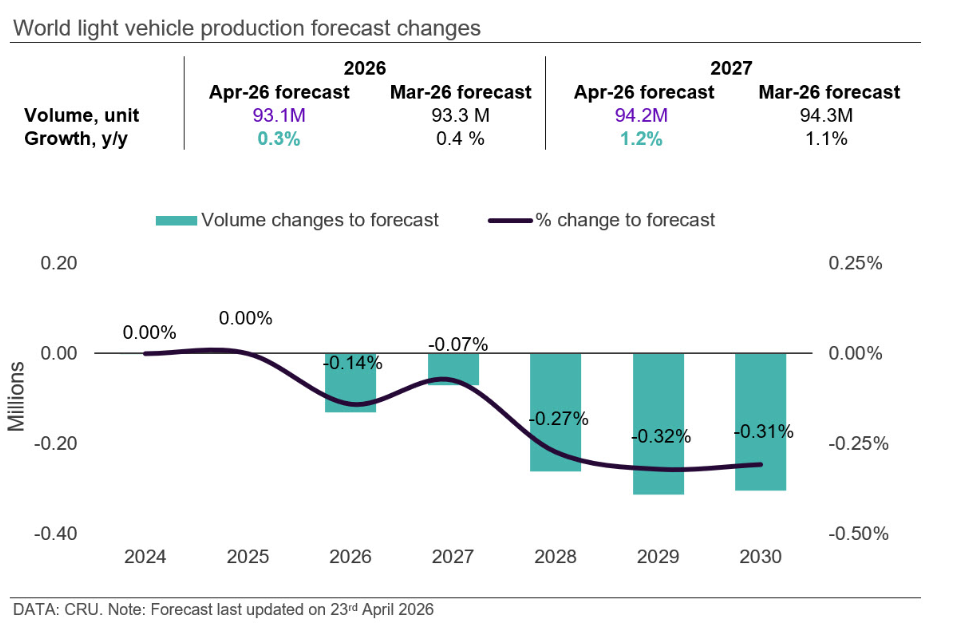

Global light vehicle production revised down

Auto outlook cut as Iran conflict hits costs, supply, and demand

Our current forecast is based on the ceasefire holding and a deal being struck before the end of May, with the Strait of Hormuz gradually reopening thereafter. However, any protracted conflict would likely lead to further downward revisions to the automotive outlook.

So far, the conflict has had a negative impact on the automotive outlook in the region, with Iran most affected. Globally, rising energy prices have increased inflationary pressure, with pump prices climbing, weighing on disposable income and consumer confidence. The longer the conflict persists and the longer fuel prices remain elevated, the more likely it is to negatively affect vehicle demand in other markets.

On the supply side, Iranian producers have seen production significantly disrupted since the onset of the conflict, although a number of carmakers have resumed production at lower utilization levels since the ceasefire took hold, and face supply constraints and shortages of some key components.

Globally, rising energy prices, logistical costs, bottlenecks, and material price increases have added to cost pressures on suppliers and carmakers, most notably for materials and feedstocks linked to the Middle East, such as aluminum and petrochemical inputs used in plastics production.

While some suppliers and carmakers have faced disruptions and used workarounds, direct production impacts outside the Middle East have been limited, with the exception of some vehicles destined for the Middle East. For instance, a number of Japanese OEMs have reduced output at their plants in Japan for vehicles destined for the Middle East. However, there are signs that supply bottlenecks are beginning to affect more suppliers and OEMs, particularly if the conflict and associated disruptions last for a prolonged period, with some suppliers reporting that they may start to see more pronounced disruption from June onwards.

As a result, if the conflict lasts longer than expected and becomes prolonged, costs are likely to remain elevated for longer, supply risk will increase, and demand could weaken further as inflationary pressure intensifies.

For more analysis of the impact of the Iran conflict, read our latest insight: Auto outlook cut as Iran conflict hits costs, supply and demand.

North America: Headwinds cloud outlook

North American short-term production analysis

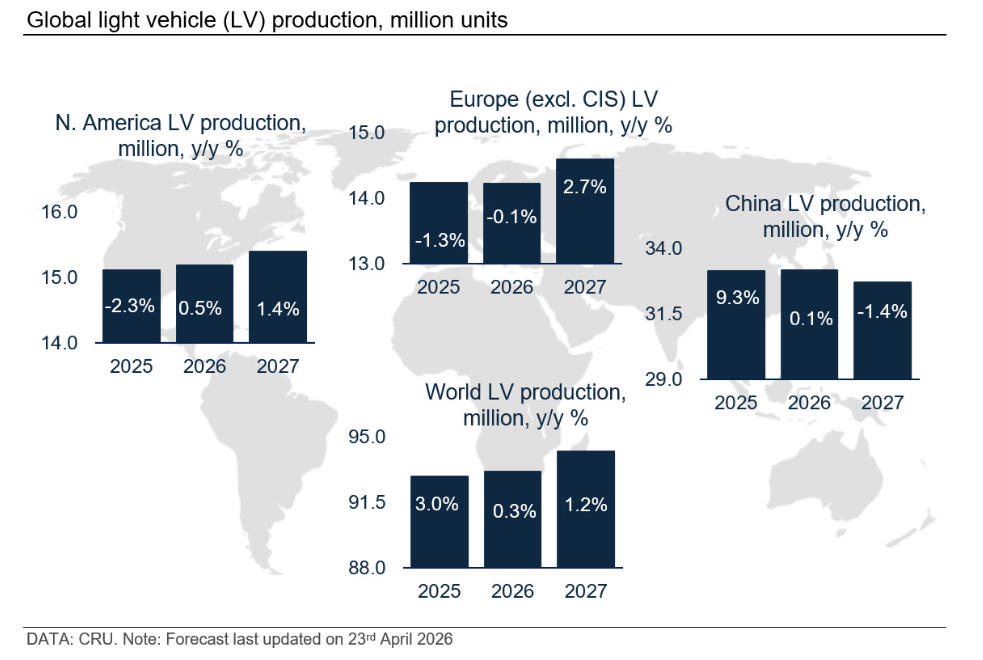

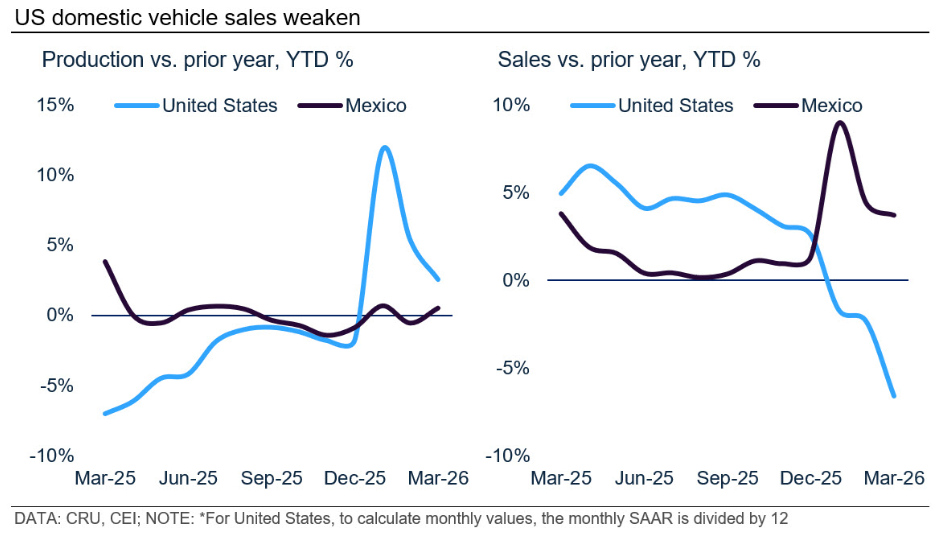

Preliminary March actuals indicate the region recorded modest growth compared with declines in the first two months of the year. Despite this, output remains relatively muted, constrained by a number of factors: weaker domestic demand, model changeovers, supply constraints, and seasonal factors.

Despite the relatively weak start, CRU expects overall output to grow modestly this year. Output will be supported by the ongoing ramp-up of newer models, localization, and inventory recovery following the retooling of some plants ahead of the introduction of newer models, as well as the recovery of some lost output from Ford, notably in H2 2026, following the Novelis hot mill fire last year. A proportion of this recovery will be pushed into 2027, when we expect GM to fully ramp up production of newer model generations.

There remains downside risk to our production outlook, given weaker domestic demand, ongoing tariff pressure, rising commodity prices, a DRAM chip supply imbalance, and the ongoing conflict in Iran, which could elevate inflationary pressure and weaken consumer confidence.

Domestic sales in the US have remained relatively subdued since the start of the year, weighed down by affordability concerns, and weak EV demand. Sales will continue to be soft over the coming months, particularly against the strong base of comparison from last year, when domestic sales were robust as consumers brought forward vehicle purchases ahead of higher tariffs. However, auto-loan interest deductions for buyers of US-assembled vehicles should provide some support to sales volumes, particularly from Q2 onwards.

The policy backdrop remains uncertain. The US administration has shown a willingness to adjust trade policy and, with the USMCA review scheduled for July 2026, further changes remain possible. The outcome of the USMCA trade renegotiation could have significant implications for the automotive landscape, given how integrated suppliers and OEMs are across borders. Canada and Mexico are likely to push for the reduction of Section 232 tariffs, while the US could push for stronger domestic-content requirements.

North American electric vehicle trends and outlook

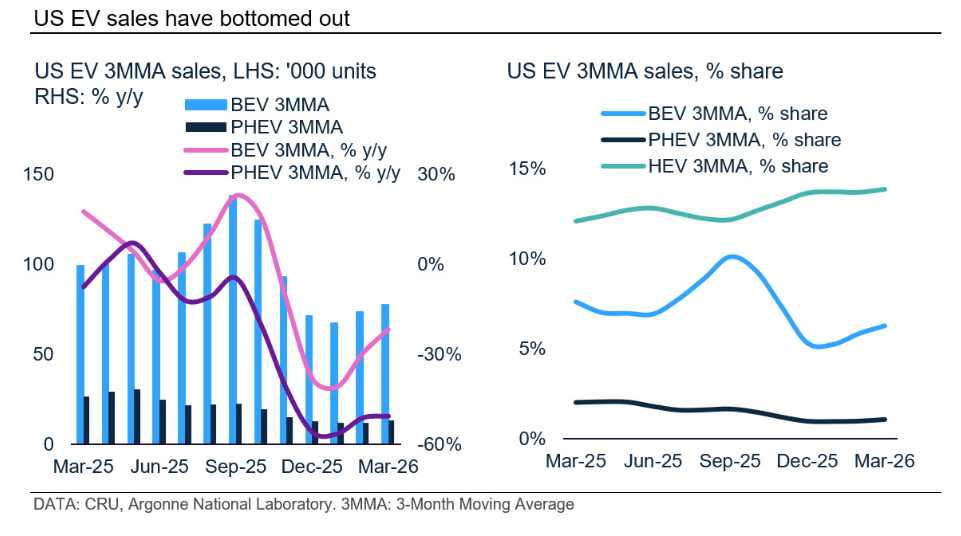

The North American BEV share remains low, particularly compared with the same period last year, although the BEV sales share surpassed 6% for the first time since before the removal of the US consumer tax credit at the end of September, indicating a modest improvement.

While BEV sales in the US fell slightly less than in each month since subsidies were removed, supported by improved pricing and some OEM/dealer incentives, sales were still down by almost a third y/y, pointing to a structurally weak BEV market. New BEV sales were not helped by rising used BEV demand, which was boosted by lower resale prices and rising inventory due to increased lease returns. BEV sales are likely to remain weak in 2026 amid softer consumer sentiment and the absence of incentives.

Several OEMs have reset their EV strategies amid weaker demand and limited policy support. These have included canceling BEV programs, repurposing plants with excess capacity, and shifting back towards ICE and hybrid line-ups.

Mexico saw stronger EV demand, supported by improved model availability and rising competition, while in Canada, there are signs that the recently introduced EV subsidy is boosting sales. We expect the solid BEV growth in Mexico and Canada to continue, given the relatively low base, some policy support, and increased model availability.

Europe: Automakers continue to face mounting headwinds

European short-term production analysis

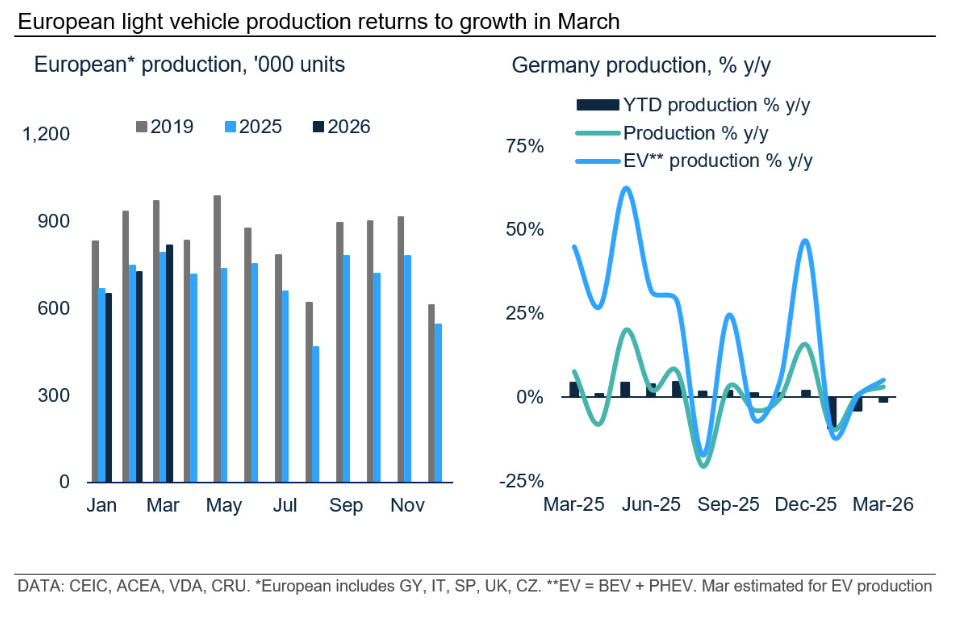

Using the latest actuals from Germany, the United Kingdom, Spain, Italy, and the Czech Republic as a proxy for European production (see chart below), output grew by 3% y/y in March, following two consecutive months of decline.

Italy continued to record strong growth, boosted by a low base and by production of several new Stellantis models in the country, such as the Jeep Compass and Fiat 500 Hybrid, which entered production at the end of last year.

In the UK, output remained constrained, marking the eighth consecutive month of y/y contraction. Production was weighed down by weaker export demand outside the EU, as well as supply disruption at JLR’s Solihull plant, which led to around two weeks of downtime.

Despite a relatively more upbeat March and some positive domestic demand indicators in the first quarter of the year, regional output this year remains relatively weak, especially in the context of pre-Covid-19 levels and after the decline seen last year. Output is set to remain constrained by weaker export demand in the US and China, with the former considering increasing tariffs from 15% to 25%, which would add further pressure to domestic producers. In addition, rising competition, notably from imports, is adding pressure on domestic producers, while higher margin and cost pressures due to regulatory changes, such as emissions standards, commodity and energy price rises, and the ongoing conflict in Iran.

We expect European output to decline this year before rebounding next year, supported by a relatively low base, some localization, and the ramp-up of some high-volume models. However, risks remain tilted to the downside, given the significant headwinds.

European short-term sales analysis

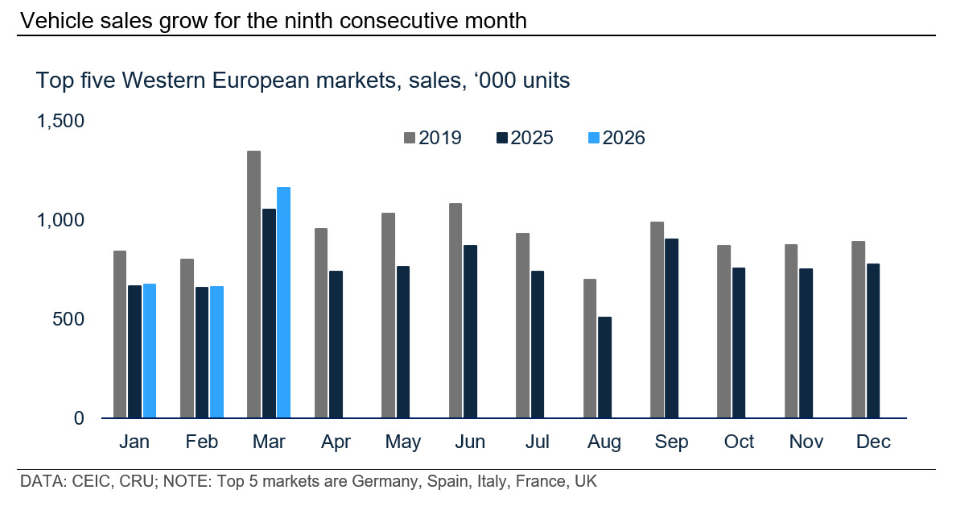

Total light-vehicle sales across the “Big 5” Western European markets (Germany, France, the UK, Italy, and Spain) rose y/y in March 2026, marking the ninth consecutive month of growth.

All five markets recorded gains in March. Germany benefited from an extra working day and robust BEV demand, supported by favorable subsidies. Spain posted double-digit growth, continuing its positive start to the year, boosted by the reintroduction of some tax benefits for EVs and charging installations. The UK also recorded solid growth, driven mainly by private vehicle demand and rising EV sales.

Despite the relatively upbeat first quarter, we expect European sales growth to remain relatively flat this year, given the economic impact of the ongoing conflict in Iran on consumers. Higher energy costs and fuel prices are expected to weigh on consumer confidence and purchasing behavior. As a result, and given the risk of a prolonged conflict, risks to the forecast remain tilted to the downside.

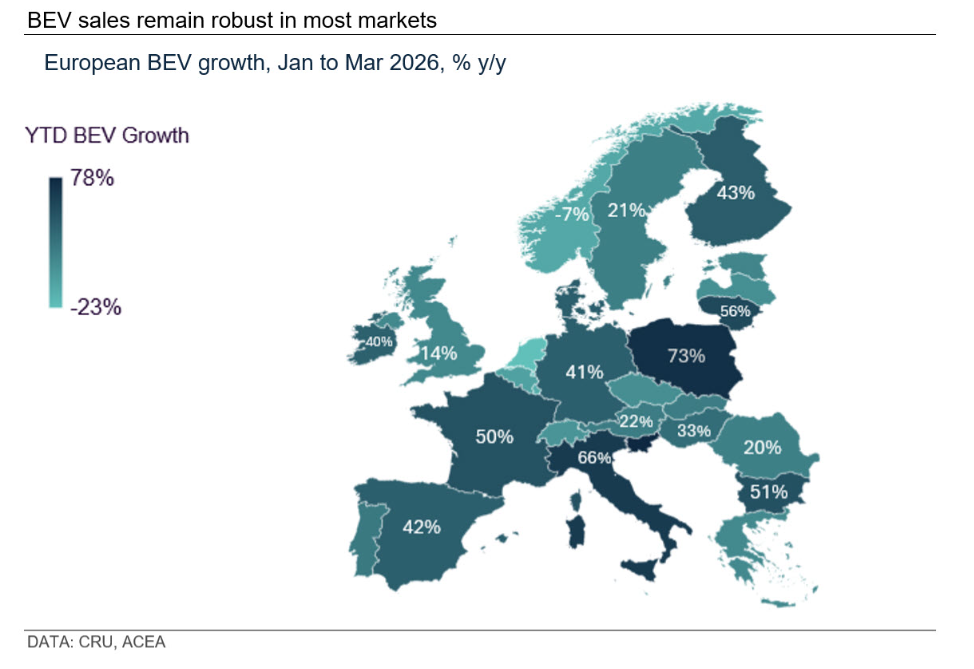

European electric vehicle trends and outlook

BEV sales reached record levels in March, with BEV market share rising to the second-highest level on record. Sales continued to grow, supported by widespread incentives in key markets, additional model launches, rising competition, and price reductions by a number of carmakers aimed at boosting sales and helping them meet emissions standards. For example, in France, BEV sales grew strongly, supported by a low base, various incentives such as the social leasing scheme and ecological bonus, as well as manufacturer incentives. Tesla, for instance, offered a trade-in bonus that helped boost sales.

PHEV sales also continued to climb in several key markets, most notably Spain and Italy, where the PHEV share is higher than the BEV share. Despite the stricter utility factor rules coming into force in 2026, PHEV demand remains strong, supported by a broader model offering, larger batteries, and growing competition from Chinese carmakers.

Chinese-made PHEVs are subject to a 10% import duty, compared with BEVs, which face tariffs of up to 45%. This gives these carmakers an opportunity to offset higher tariffs, diversify their offering, and boost sales by launching PHEVs.

We expect both BEV and PHEV sales to continue outpacing the overall market this year, increasing their share. Imports of Chinese-made EVs should continue to rise over the medium term, although we expect some Chinese OEMs to localize over time, which will help them mitigate supply risk, offset higher tariffs, and qualify for incentives that favor domestic producers.

China: Domestic demand remains weak

China short-term analysis

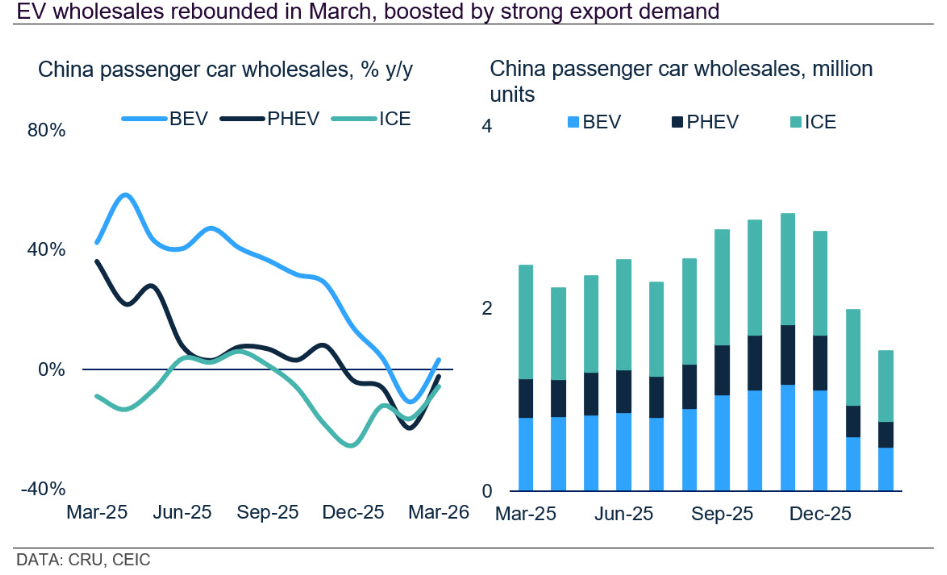

According to the China Association of Automobile Manufacturers (CAAM), passenger car wholesales declined by 0.5% y/y in March, marking the fourth consecutive month of y/y declines. Meanwhile, the China Passenger Car Association (CPCA) reported a 15% y/y decline in domestic sales, the sixth consecutive month of y/y contraction.

Chinese domestic vehicle sales continued to decline in March, although sales rose sharply in comparison to the previous month. Despite this, domestic demand has started the year off on a weak footing, weighed down by policy changes, such as the tightening of the trade-in policy, and weaker consumer confidence.

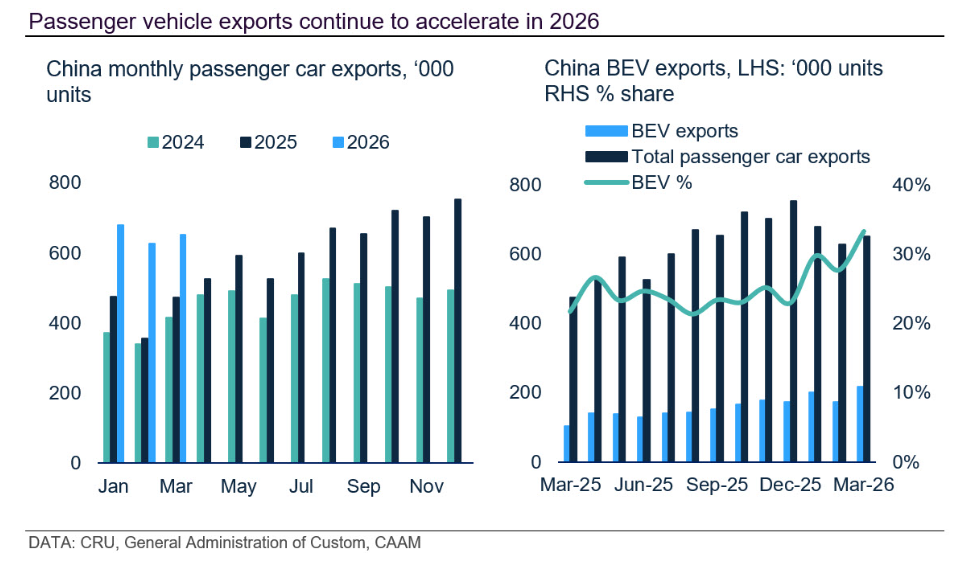

Despite weaker domestic sales, exports continue to grow strongly, as Chinese carmakers continue to penetrate overseas markets to gain market share and help offset domestic margin pressure and intense competition. Export growth was seen across all major powertrain types, with BEVs and PHEVs recording the fastest gains, as Chinese carmakers continue to leverage their competitive advantage in these segments. Growth in these categories is also somewhat inflated relative to ICE vehicles because of a lower base, as the bulk of vehicles exported from China are still ICE models, although the gap is narrowing as Chinese brands expand their EV offerings. Chinese brands’ strategies vary by region, depending on local demand and regulations.

Since the turn of the year, the Chinese administration has tightened a series of measures centered on regulation and incentives, designed both to ensure the industry stands on its own feet and to provide targeted support for innovation and technological development, particularly in electric vehicles. For instance, the government has adjusted both the trade-in policy and the EV purchase tax.

China electric vehicle trends and outlook

Chinese BEV sales continued their weak start to 2026, although BEV share improved in March versus the first two months of the year. The overall market remained subdued in Q1, while EV sales were hit particularly hard by the tightening of trade-in policy, EV tax exemptions, and stricter technical requirements, weighing on demand more than pure ICE sales, with the A-segment most affected.

PHEV sales fell more sharply than BEV sales, pressured by stricter incentive criteria, including a minimum electric-only range of over 100 km. As a result, PHEV share is below the same period last year.

Despite the weak start, EV demand should recover, although growth will be slower than last year. We expect a pickup from Q2, with most growth in H2, supported by new product launches and improved confidence. Higher fuel prices, driven by the Iran conflict, could also support EV demand, although the government has limited fuel price rises.

Despite weak domestic BEV sales, NEV exports remain robust, with more Chinese carmakers expanding overseas to offset domestic pressure and support overall sales.

Domestic sales are set to contract y/y this year for the first time since 2020, as incentives taper and a period of structural reform takes hold. However, while we expect vehicle sales to decline, output should still increase marginally, supported by strong export demand. However, rising inventory levels and growing cost pressures pose downside risks. OEMs are facing cost pressures from semiconductors, lithium, aluminum, and copper, prompting some carmakers to raise prices on certain models.

Policymakers have sought to curb aggressive pricing under the “involution” banner, with recent measures aimed at preventing carmakers from selling vehicles below cost. Although competition is likely to remain intense, there are signs that the market is shifting from volume towards value as price cuts begin to ease. However, strategies vary by OEM.

Over the medium to long term, we continue to expect BEVs to become the dominant powertrain, with ICE share declining, albeit at a slower pace and with meaningful variation by segment. PHEV share is likely to plateau over our forecast horizon before gradually easing as consumer preference shifts increasingly towards BEVs. However, in certain segments and use cases, particularly where range requirements and charging constraints persist, and in the absence of an ICE phase-out target, ICE vehicles and PHEVs are likely to remain attractive options.

Established key trends

These are some of the key established trends that CRU believes are having a profound effect on the automotive industry. (newly added, existing trend)

- Supply risk – Protectionism remains an ongoing supply-side risk. In addition, concerns around the availability of certain semiconductor chips remain firmly on automotive stakeholders’ radar. While the Nexperia-related chip shortage has eased somewhat, there are signs that another supply squeeze may be emerging. Reports suggest demand for DRAM (dynamic random-access memory), used in infotainment and ADAS systems, may exceed supply, which could drive price increases and potentially lead to supply disruption. Given DRAM content is typically higher in more premium vehicles, the impact may be more pronounced at the premium end of the market, although premium OEMs generally have more room to absorb price increases.

- Material price increase – Recent price rises in a number of raw materials, such as aluminum, copper, and battery raw materials, have pushed underlying vehicle prices upwards, with BEV raw material costs rising disproportionately relative to ICE vehicles. There is also a risk that energy prices could rise due to the ongoing conflict in Iran. This could add further cost pressure on stakeholders, such as OEMs, potentially resulting in higher costs for consumers and weighing on vehicle demand.

- Rising protectionism –The US administration has imposed an additional 25% tariff on imported vehicles and key components. While there has been some flexibility for USMCA-compliant parts and vehicles, as well as through bilateral agreements with key trading partners, tariffs remain significantly higher than pre-2025 levels. In addition, uncertainty persists regarding future policy measures, including the 2026 USMCA negotiations. There is also a lingering risk that tariffs could escalate into broader protectionist actions.

- Rising protectionism continued – China’s growing control over the automotive supply chain is becoming increasingly evident. Export controls on rare earths, restrictions on battery materials, and recent limits affecting semiconductor supply are heightening industry uncertainty. We expect China to continue leveraging its strategic position, while other countries move to diversify and secure access to critical materials and components. As a result, downside risks to automotive supply are likely to persist.

- Rising protectionism continued – The EU’s Industrial Accelerator Act proposes new measures, including “Made in the EU” (Union origin) requirements for vehicles and low-carbon requirements in a range of energy-intensive industries, and is designed to increase investment and localization in the EU. While many EV models may already source a substantial share of components domestically (excluding the battery), some components and models are likely to fall below the thresholds set out in the proposal. As a result, OEMs will need to weigh the costs of increasing domestic sourcing against the risk of becoming ineligible for public intervention and financial support schemes for corporate vehicles. These measures could also increase trade frictions with countries that are not exempt from the act, such as China.

- Protracted Iran conflict – A protracted conflict in Iran would have significant repercussions not only in the Middle East but globally. Inflationary pressures, particularly through higher energy prices, would weaken consumer confidence and increase costs across the automotive value chain. In addition, disruption to the supply of key materials and trade routes would add further cost and sourcing pressures, potentially affecting production and build rates. Ultimately, a prolonged conflict would weaken demand relative to our base case, with all regions affected, albeit to varying degrees.

- Regionalization – Increased protectionism, trade barriers, and diverging EV demand and consumer preference are prompting OEMs to increasingly regionalize their operations and product offerings, aimed at ensuring they remain responsive and competitive in an ever-changing market landscape.

- EV and emissions policy rollback – The US administration has rolled back IRA consumer tax credits, as well as taken steps to water down EPA and CAFE regulations. These changes are dampening EV demand and reducing compliance pressure on automakers, potentially prompting a shift back toward ICE and hybrid vehicles.

In the EU, the European Commission has also adopted a more flexible approach to emissions targets, allowing compliance to be measured over a three-year period instead of annually. Despite this adjustment, we remain optimistic about BEV growth. Automakers must still manage their emissions performance, even if regulations are softened. Additionally, the introduction of more affordable, high-volume models, increasing competition from Chinese brands, and the UK’s ZEV mandate will continue to drive BEV sales growth.

The European Commission has announced an Automotive Package designed to support EU manufacturers and introduce greater flexibility in emissions regulation. A central proposal is to relax the 2035 mandate for a 100% tailpipe emissions reduction (versus 2021 levels), replacing it with a 90% target. As a result, we have revised our BEV forecast lower, with the reduction largely reallocated to a higher share of PHEVs and other ICE powertrains. Even so, BEVs are still expected to remain the dominant powertrain type. - Competition in China – Competition remains intense in China, with cost pressures felt across the value chain. As a result, the Chinese government has increased scrutiny on the industry to curb aggressive price cuts and stabilize the market. Given the fierce competition, further brand consolidation is expected over the forecast period. Foreign brands are facing growing challenges, particularly in the EV segment, prompting some to reconsider their strategies –including potential market exits or deeper partnerships with local players.

- Chinese expansion – Chinese carmakers are increasing their footprint globally. A reversal of historical trends is possible, with western OEMs potentially forming joint ventures with Chinese brands in western markets or even selling underutilized plants to Chinese automakers seeking to localize production. Chinese brands aim to increase their BEV and plug-in hybrid penetration across various regions, intensifying competition in those markets.

- Opportunity for Chinese carmakers in Europe – Postponement of the 2035 effective ICE ban, the planned introduction of a minimum import price for Chinese-made BEV exports (potentially replacing higher BEV tariffs), Chinese OEMs’ localization plans, and increasingly compelling battery and EV offerings should provide Chinese automakers with an opportunity to build on their growing success in Europe and continue gaining market share.

- Anti-involution in China – China’s anti-involution campaign has eased price wars as automakers shift to value-based incentives—such as offering higher-spec vehicles at the same price—while the government tightens oversight by warning OEMs against aggressive discounting and low-price dumping. Reinforcing this push to curb aggressive competition, regulators have also moved to require export licenses for electric-vehicle makers starting in 2026, adding to measures aimed at stabilizing the market.