Analysis

April 17, 2026

CRU: US domestic market still awaiting imports to relieve tightness

Written by Matthew Abrams

This item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Conditions in the US market remain tight as domestic demand is holding up with support from border wall projects and data center investments. The supply side has struggled to keep pace with weak import volumes, impacting the market.

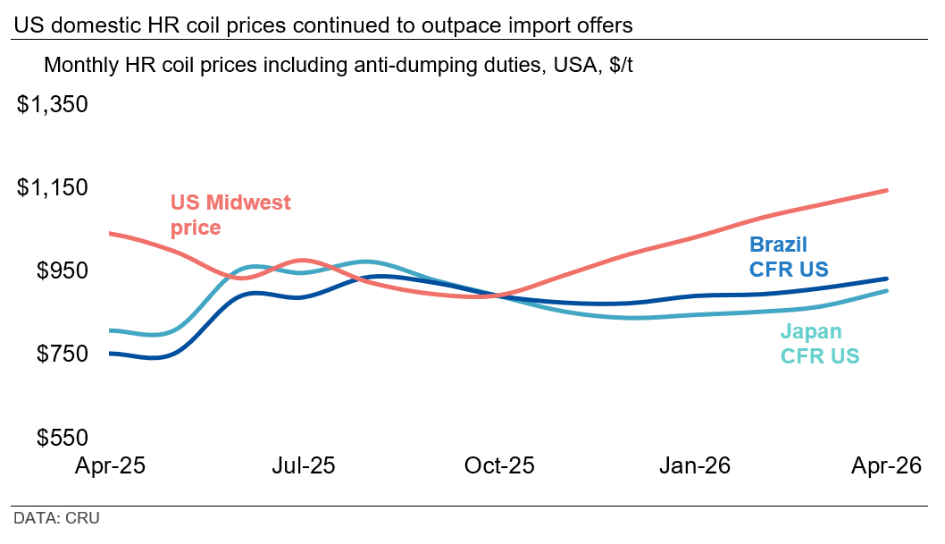

US domestic steel prices have thus continued to edge higher throughout March across sheet and plate products. Longs prices mostly flattened out in our latest assessment. However, there is still upside pressure in the market, with mills trying to raise prices for both rebar and wire rod. This has helped domestic pricing continue outpacing import offers.

Even with higher domestic steel prices, import volume has yet to pick up meaningfully. Imports of light flat-rolled products are now down 50% YTD through March. Imports of wire rod are down 22%, and rebar is down 4%.

The conflict in the Middle East has been playing a role in delaying imports. The conflict pushed ocean freight, insurance costs, and inland fuel costs higher, which raised the landed costs of imports and supported higher domestic pricing. In addition, supply chain disruptions also added to the delay, with lead times for imports of roughly three to four months. These factors have supported the extended price rally.

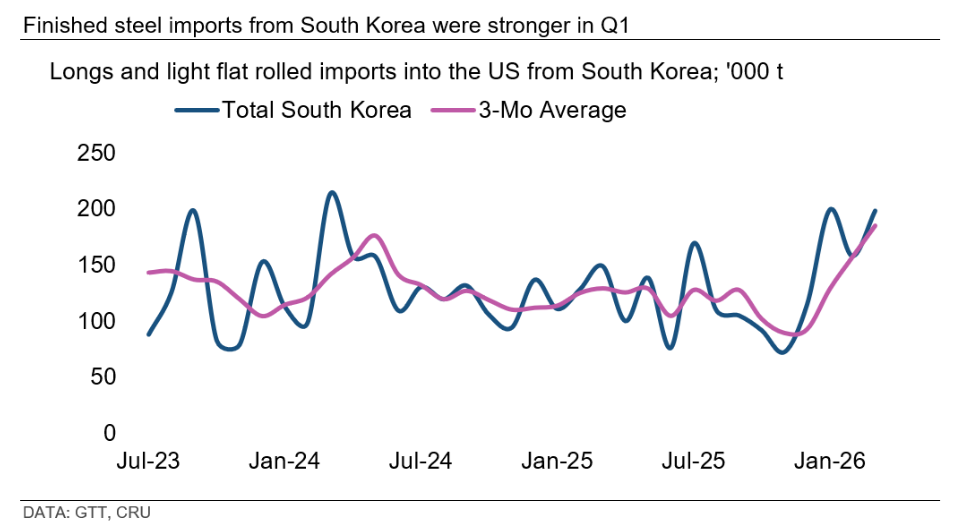

Imports from South Korea, however, continued to gain momentum. The USD-KRW exchange rate still sits at one of the highest points in history as the near-term peak reached global financial crisis levels. It has since come off that peak but still remains elevated. This has helped attract more imports from the country, with the 3-month average of longs and light flat-rolled reaching 185,000 metric tons, its highest point post-pandemic.

On April 3, there were sweeping changes announced to the Section 232 tariffs. The US administration changed the tariffs to include four different tariff rates. Commodity grades are still 50%, but derivative products now have varying rates from 15-25%. The duty is now applied to the full customs value rather than just the metal content.

One change that did not draw as much attention initially is the addition of a 10% tariff on imports of the listed derivative products if the metal is melted and poured in the US. Originally, these products were excluded from the tariffs. Some importers and processors reported making efforts to source more American-made steel to qualify for this exemption, so this is a meaningful change.

Brazilian slab export prices increase again due to tight global supply

Brazilian slab prices continued to rise m/m in April, increasing by $50/mt to $590/mt FOB Brazil, as global demand remained steady amid tight supply and higher prices from Asia. Iran is an important slab exporter to Asian markets, and the country’s supply has been significantly curtailed due to the ongoing conflict in the Middle East. This has reduced the availability of material globally and further supported demand for Brazilian slabs among European buyers. In addition, higher HR coil prices in the USA and Europe also provided support to Brazilian slab prices.