Analysis

August 12, 2025

HVAC equipment shipments fall through June

Written by Brett Linton

Total heating and cooling equipment shipments eased from May to June, according to the latest data released by the Air-Conditioning, Heating, and Refrigeration Institute (AHRI). Shipments of water heaters, warm-air furnaces, and air conditioners/heat pumps all declined month over month (m/m).

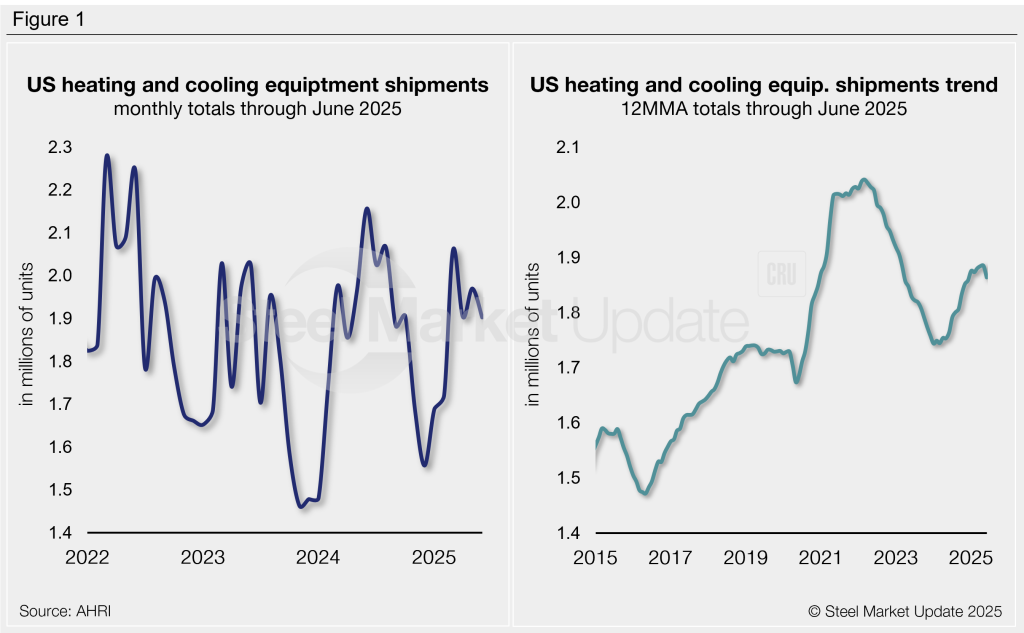

Total June shipments were down 3% m/m to a four-month low of 1.90 million units, 12% less than the same month last year (Figure 1, left).

June is typically one of the stronger shipping months of the year, but this June marks the lowest rate seen since 2015. Although total shipments fell this month, year-to-date volumes remain strong. Over 11.2 million units were produced in the first six months of the year, the third-highest rate in our 19-year data history.

Trends

To smooth out seasonal swings, shipments can be annualized using a 12-month moving average (12MMA). On this basis, total shipments peaked in early 2022 following the post-Covid surge, then declined through late 2023. A recovery began in early 2024 and continued through May of this year, with annualized shipments climbing to a two-and-a-half year high of 1.89 million units. In June, we saw this streak break as the 12MMA slipped to 1.86 million units, still up 6% year over year (y/y) (Figure 1, right).

Shipments by product

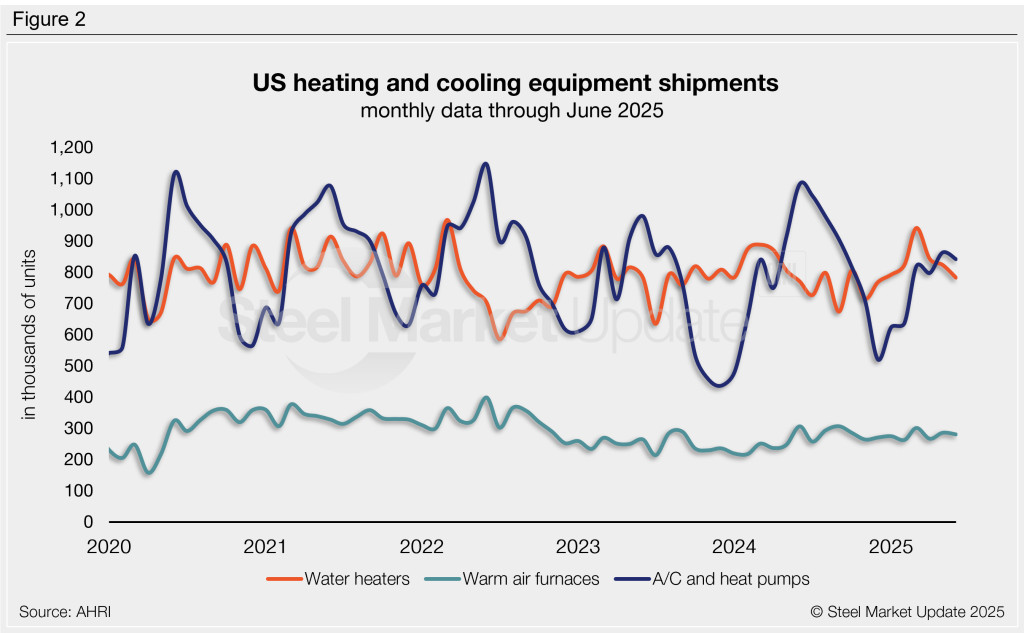

- Following March’s three-year high, water heater shipments fell for the third consecutive month to a six-month low of 782,000 units. Although down 5% m/m, June levels were up 2% y/y.

- Shipments of warm-air furnaces declined 2% m/m to 280,000 units in June, down 8% from the same month last year. This follows one full year of positive annual growth.

- Air conditioners and heat pump shipments fell 2% m/m from May’s eight-month high, falling to 841,000 units. June shipments are down 22% y/y. Note that these shipments are highly seasonal, as shown in Figure 2.

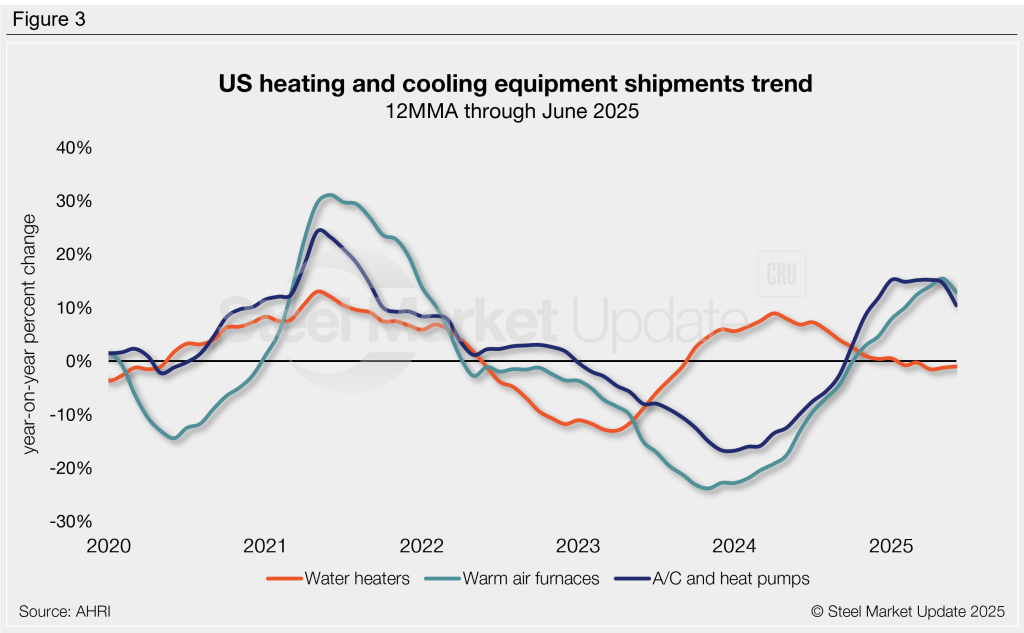

Annual growth driven by cooling equipment

Figure 3 shows the annual growth rate of shipments by product on a 12MMA basis. From this angle, annualized shipments are still holding up for most products, though weakness lingers in a few categories:

- Air conditioner and heat pump shipments were 10% higher on an annualized basis compared to the same period one year ago. June represents the ninth-consecutive month of positive annual growth but is one of the lower rates seen this year.

- Warm-air furnace shipments experienced the largest annualized gain, rising 13% y/y and the eighth month in a row to see growth.

- Water heater shipments contracted for the fifth-consecutive month, down 1% y/y. This rate has steadily eased following the mid-2024 peak.

An interactive history of heating and cooling equipment shipment data is available here on our website. If you need assistance navigating our website, please contact us at info@steelmarketupdate.com.