Analysis

August 15, 2025

July service center shipments and inventories report

Written by Estelle Tran

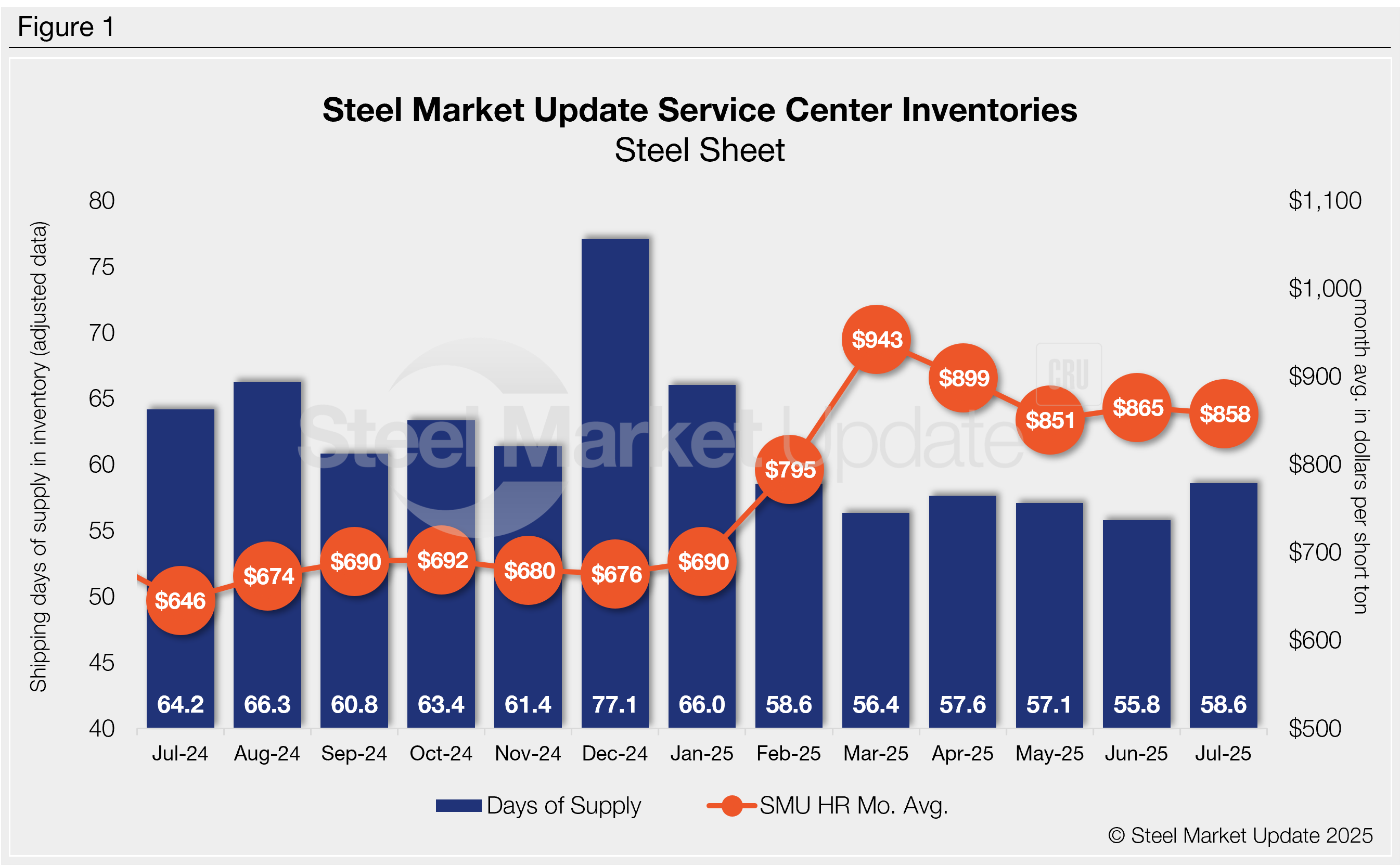

Flat rolled = 58.6 shipping days of supply

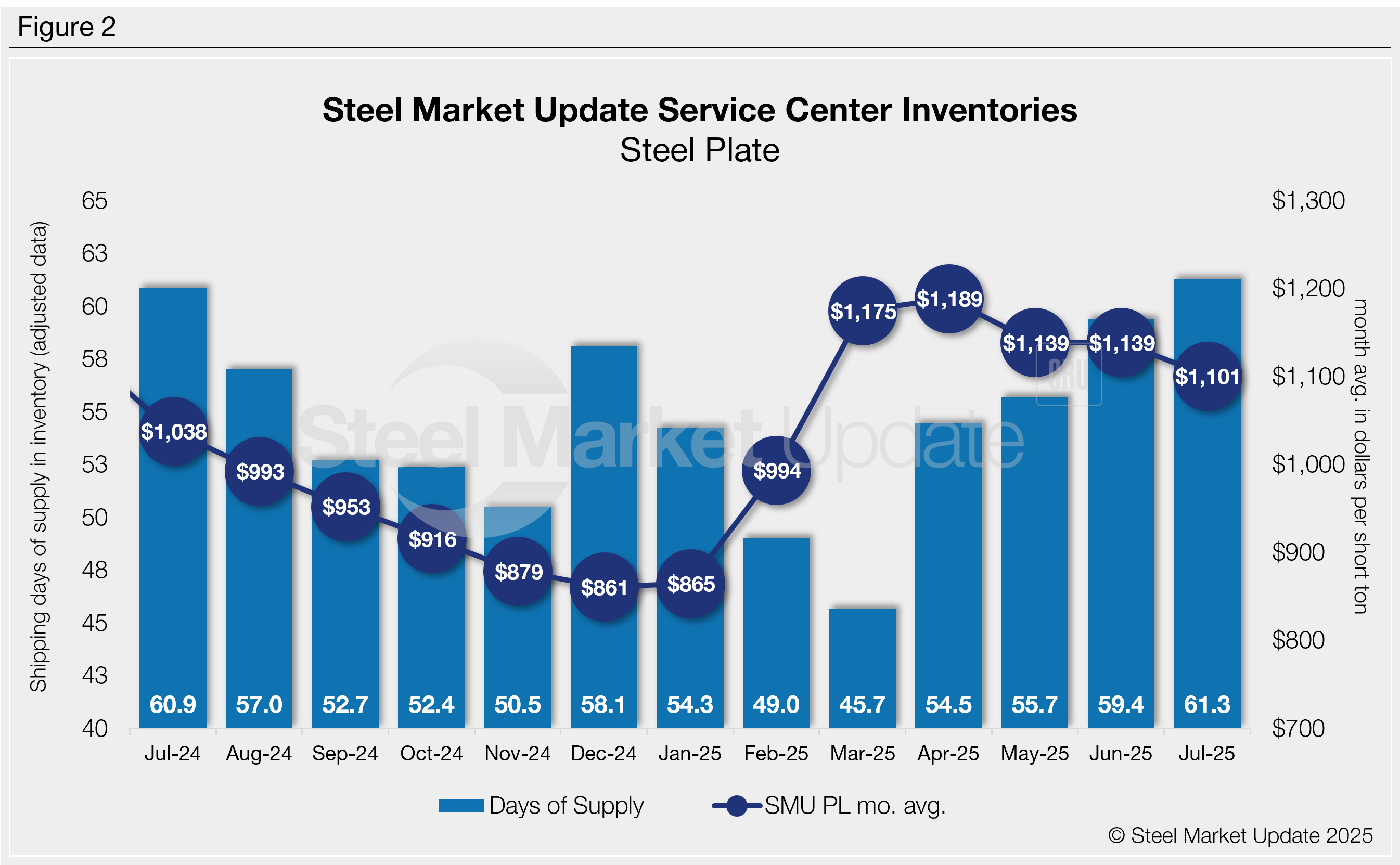

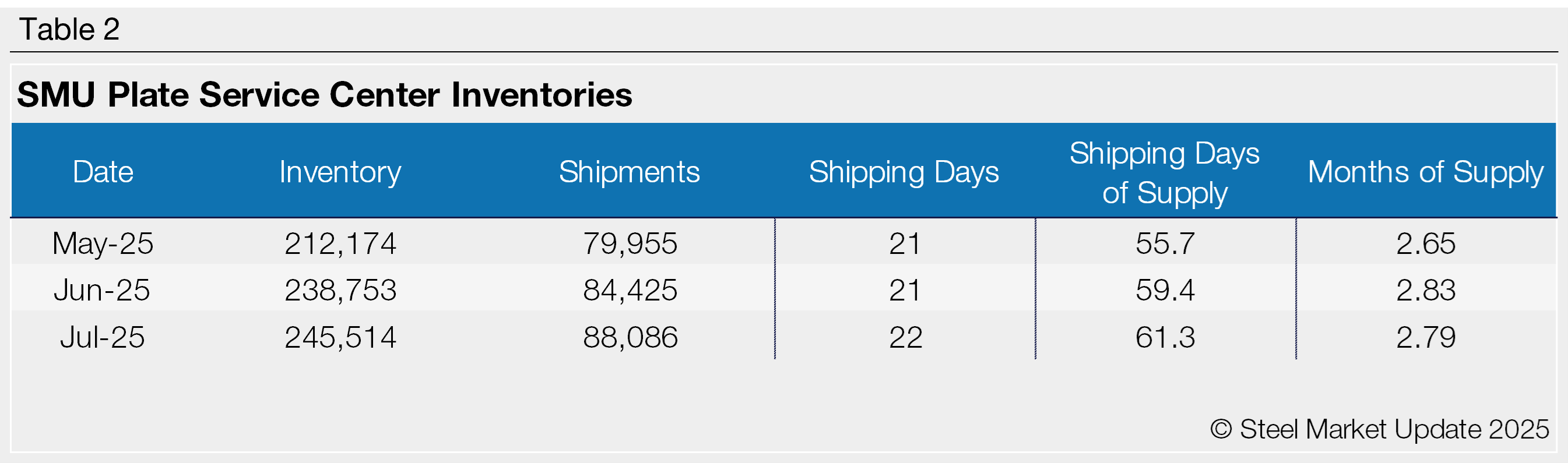

Plate = 61.3 shipping days of supply

Flat rolled

In July, US service centers’ flat-rolled steel supply increased month on month, following the seasonal summer trend of inventory build with slowing shipments. At the end of July, service centers carried 58.6 shipping days of supply on an adjusted basis, according to SMU data, up from 55.8 shipping days of supply in June. Flat roll inventories represented 2.66 months of supply in July, flat compared to June.

July had 22 shipping days, which is one more shipping day than in June. In July, service centers usually try to reduce inventories to align with slowing demand.

In the latest SMU survey published August 8, 69% of service centers said they were maintaining inventory, while 25% said they were reducing inventory. The latest SMU survey also found that 34% of companies surveyed did not meet their business forecasts last month, while 49% met their forecasts and 17% exceeded forecasts.

Given weaker-than-expected demand, we see inventories in surplus. Some of this can be attributed to larger buyers making opportunistic purchases in the last several weeks – instead of destocking.

Most service centers have been content to stay on the sidelines, though, as prices have slid this summer and lead times have remained short. The latest SMU survey found mill lead times for hot-rolled coil were at 4.44 weeks, down from 4.55 weeks the month before.

Material on order at the end of July was like that of June. At the end of July, flat-rolled steel on order in shipping days of supply was up slightly from June. This uptick is attributed to the lower daily shipping rate. Material on order as a percentage of inventories in July was like June but much lower than the year-ago level. This difference reflects buyers’ views on prices this year.

In July 2024, service centers bought heavily at the end of the month, anticipating the bottom of the market. The latest SMU survey, published August 8, had 28% of respondents say that prices had already bottomed, while 28% said prices would bottom in August, and 22% anticipated prices to reach a floor in September.

Moving into the fall months, material on order should pick up, though we expect inventories to remain in surplus into November.

Plate

US service center plate supply also rose in July, amid ongoing demand weakness. At the end of July, service centers stocked 61.3 shipping days of plate supply on an adjusted basis, according to SMU data. This is up from 59.4 shipping days of supply in June and July 2024’s 60.9 shipping days. Inventories represented 2.79 months of supply in July, down slightly from 2.83 months in June.

Market contacts have reported softer demand in the last couple of months, beyond the typical summer slowdown. Some major construction projects have been postponed indefinitely, and H2 demand outlooks are unclear, according to service center contacts. Total US construction in the first half of the year was down 2.2%, according to non-seasonally adjusted data from the US Census Bureau. In June, total construction spending declined 3% y/y, while non-residential construction spending declined 0.5% y/y.

Meanwhile, mill lead times have hovered just over five weeks for plate, according to SMU data, though some market contacts have indicated shorter lead times.

Inventories in July were more than sufficient to meet current demand, and service centers have backed off on new orders. At the end of July, plate on order represented in shipping days of supply was down from June. July’s material on order was higher than July 2024’s, though.

Material on order as a percentage of inventories in July was down vs. June. Some of the drop-off in material on order could also be the pullback of import orders, which service center contacts said could help support pricing in Q4.