Analysis

September 17, 2025

August service center shipments and inventories report

Written by Estelle Tran

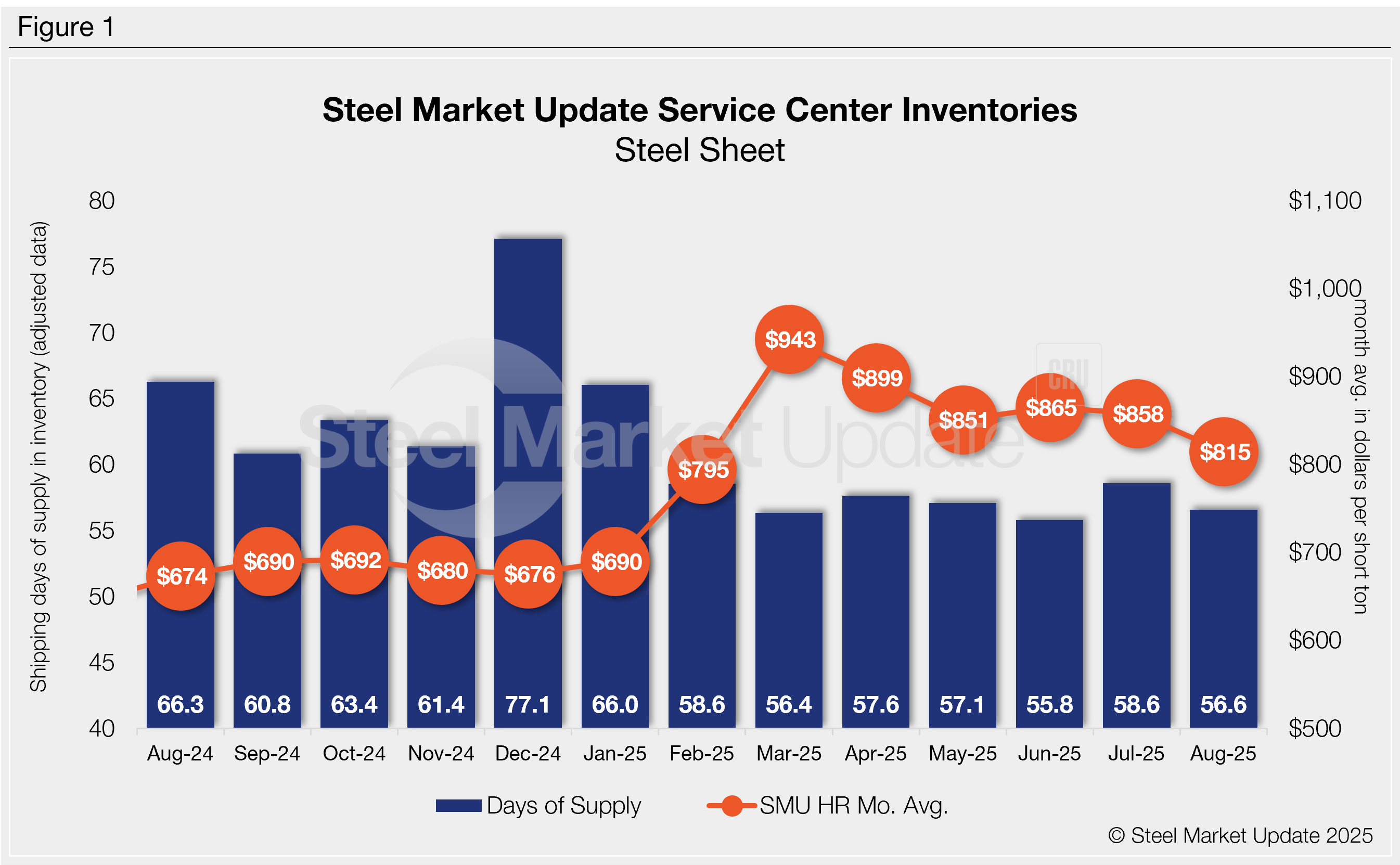

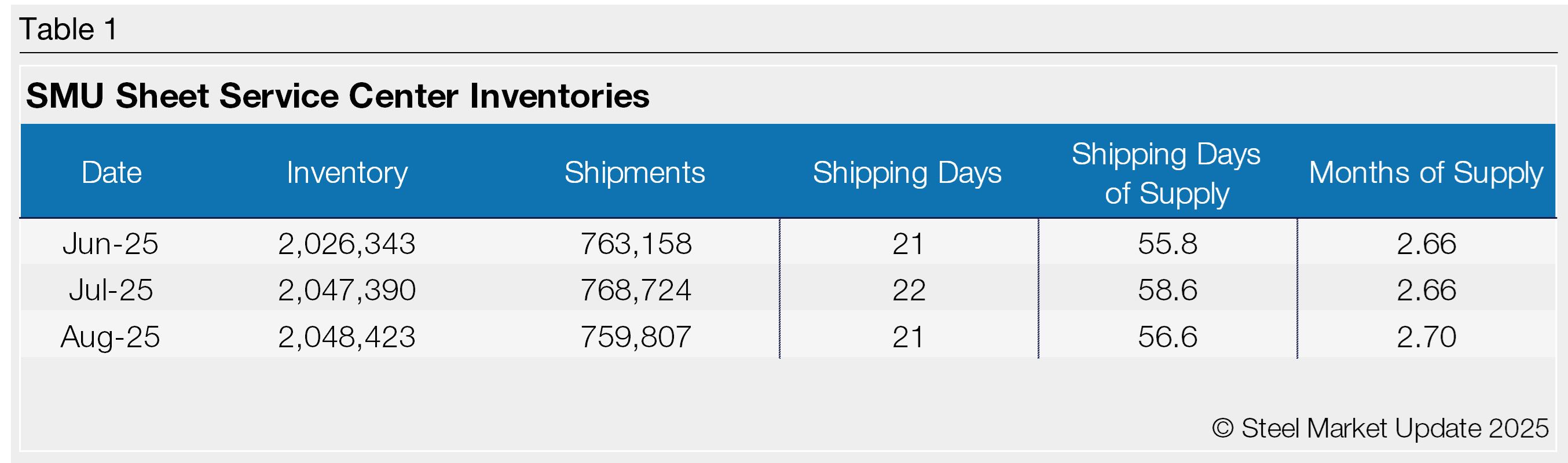

Flat rolled = 56.6 shipping days of supply

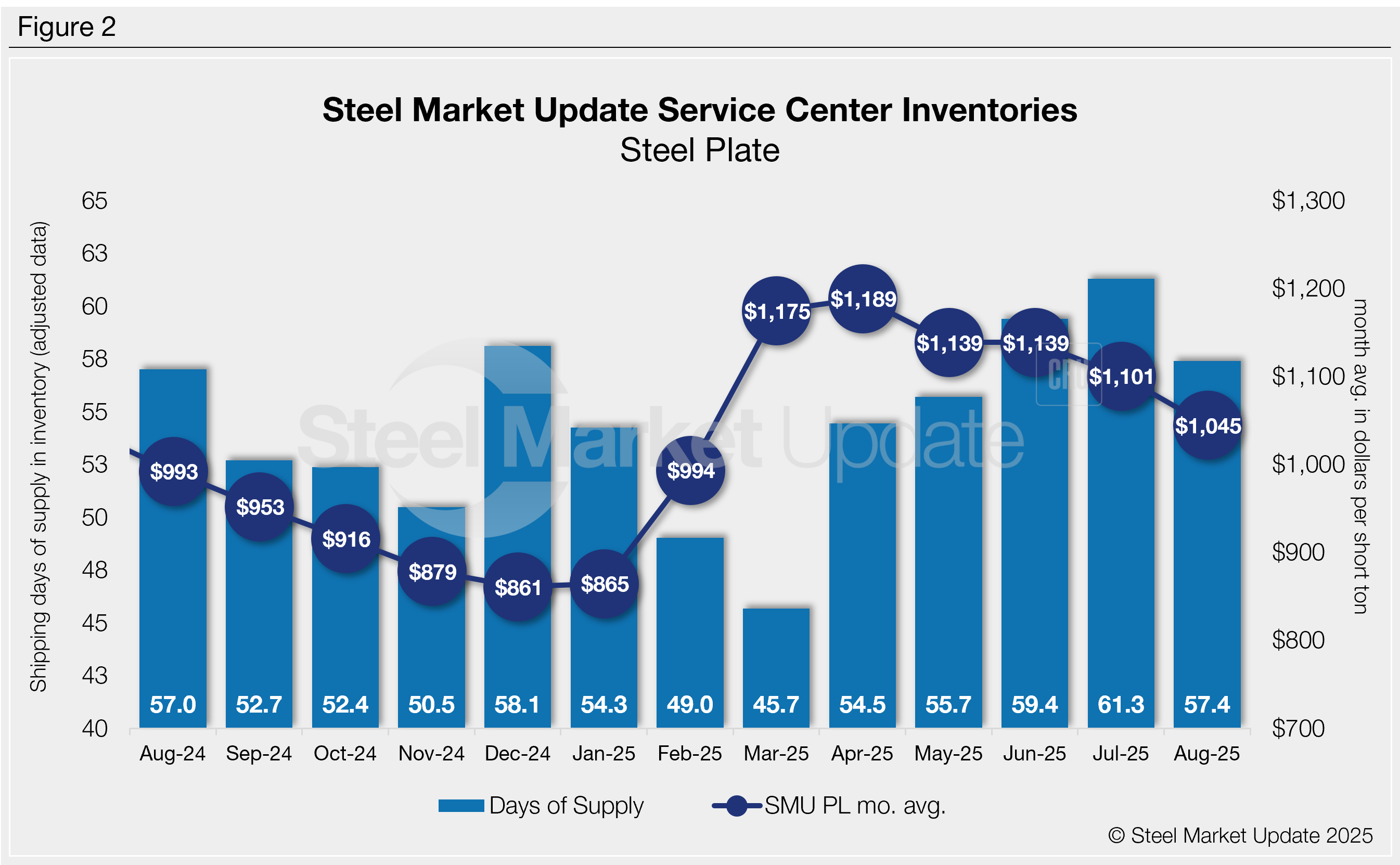

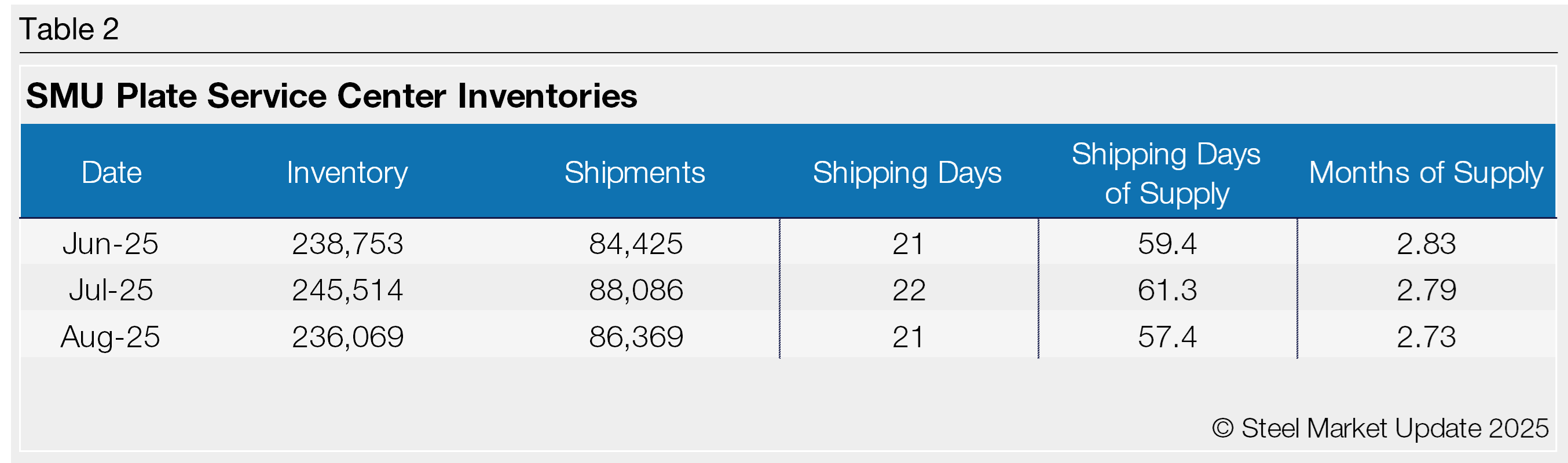

Plate = 57.4 shipping days of supply

Flat rolled

US service centers flat-rolled steel supply in August declined month-over-month (m/m) and year-over-year (y/y), according to SMU data. At the end of August, service centers held 56.6 shipping days of flat roll supply on an adjusted basis, down from 58.6 days in July and 66.3 days in August 2024.

Flat roll inventories represented 2.7 months of supply in August, which is slightly more than the 2.66 months in July 2025 but lower than 3.01 months in August 2024.

August had 21 shipping days, compared to July’s 22. While inventories are lower year over year, they are still in a slight surplus. Market contacts have reported a lackluster demand, exceeding the usual seasonal slowdown.

The latest SMU survey on Sept. 5 had 50% of service centers reporting that their manufacturing customers were reducing orders, and 40% were maintaining orders. A month ago, 23% of service centers said manufacturing customers were reducing orders, and 71% were maintaining orders. The survey also found that 70% of service centers were releasing less steel than a year ago.

Meanwhile, flat-rolled steel on order increased slightly in August. This could be related to additional buying to account for fall maintenance outages or possibly because of new capacity. This could also reflect some opportunistic deals before the outages.

Though inventories are in a slight surplus and material on order rose in August, the data points to a pickup in sheet prices. Last year at this time, there was a greater surplus, and that did not stop prices from getting a temporary bump in September/October. We expect flat roll inventories to trend lower in September.

Plate

US service center plate supply also declined m/m in August, though it remains higher than y/y levels. At the end of August, service centers carried 57.4 shipping days of plate supply, down from 61.3 days in July but up from 57 days in August 2024.

Plate inventories represented 2.73 months of supply in August, down from 2.79 months in July. In August 2024, service centers held 2.59 months of supply.

Plate inventories seem to be in near balance, though possibly still heavy relative to softer-than-expected demand. While market contacts have reported an increase in project work, mill lead times have not moved out significantly. SMU reported plate lead times at 5.29 weeks in the latest survey, just slightly higher than 5.13 weeks the month before.

Material on order also supports the view that lead times are relatively flat. Service centers shipping days of plate supply at the end of August are down vs. July, but still nearly 20% above shipping days of supply on order y/y.

While plate inventories and material on order declined m/m, the data does not signal an obvious turning point. Service centers remain focused on reducing higher-priced inventory.