Prices

October 23, 2025

HR Futures: Consequences of a tariff trap

Written by Daniel Doderer

As another month goes by and another futures columnist starts by saying “not much to see here,” I understand that a reader might flip their brain to skim mode. However, I urge you to stay with me here as I work through what the longer-term implications of a sleepy futures market may actually suggest.

It’s been about seven months since my last column, and a lot has happened over that period of time.

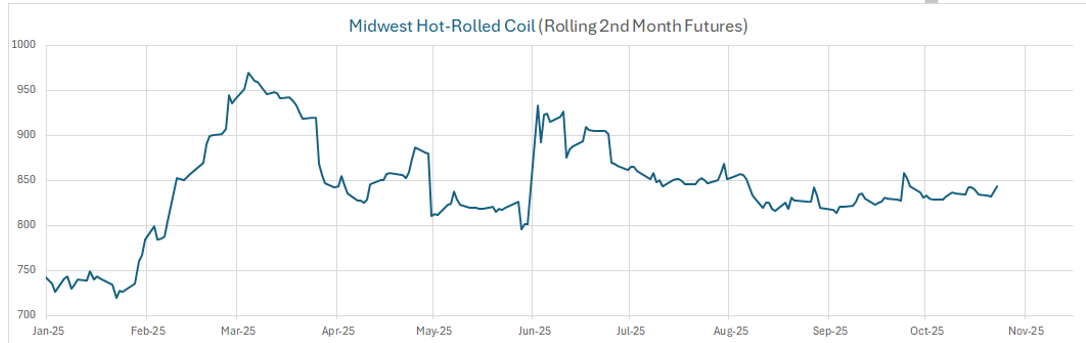

Noted above, near-term pricing (shown in rolling second-month futures) has remained confined to roughly a $50 range since late June—a pattern that began when President Trump’s announcement of 50% tariffs sparked a brief rally, followed by a relatively quick pullback.

Beneath the surface, however, the issue may not be weak demand so much as the presence of a stronger hand than the invisible one meant to guide markets.

For months, uncertainty around the rules of the road has acted as a brake on activity across the ferrous value chain. Buyers have resisted the usual impulse to attempt to time the market and rebuild inventories, opting instead to wait unsure what policy framework they’ll be operating under.

The effects are clear both in the data and in sentiment: consumption has softened, lead times remain short (although outages should lead to a modest improvement), and even attractively priced tons struggle to find urgency. This hesitation isn’t irrational, but rather systemic. For nearly two years, waiting has carried little downside, from the long pause before the Federal Open Market Committee (FOMC) cuts to today’s lack of policy clarity. And with each hint of resolution delayed – much like the Fed’s can-kicking through 2024 – the market’s collective mood has shifted from cautious optimism to frozen in place.

Again, the problem here is that there is underlying demand for steel behind a myriad of affordability concerns. There is a clear gap in housing and construction for decades, along with the massive second-effect benefits for the steel industry that come along with that.

The gap in auto sales caused by the pandemic supply chain issues has yet to be filled, despite tariff front running last winter and the recent rush to beat the expiration of the EV tax credits. Think piece after think piece inundate us with how desperate the need is to dramatically increase energy production in general but especially for AI. On top of the fact that infrastructure in the US is in significant need of upgrades. All of these dynamics should provide a massive tailwind for innovation, optimism, and a long runway for increases to production and consumption.

At the same time, the market has found itself tethered to an artificial stability that no one quite believes in. Tariffs have done what they were designed to do – putting a floor under domestic prices, thereby building a mote around native industry. The major risk now is that the floor becomes a structural feature rather than a safeguard. At this point, you cannot fathom removing them without collapsing the entire framework it was meant to support. The combination of restricted imports and embedded policy risk has dulled both price discovery and competitive tension. There is no longer a free-market correction waiting in the wings. Prices simply oscillate within narrow boundaries that policy allows.

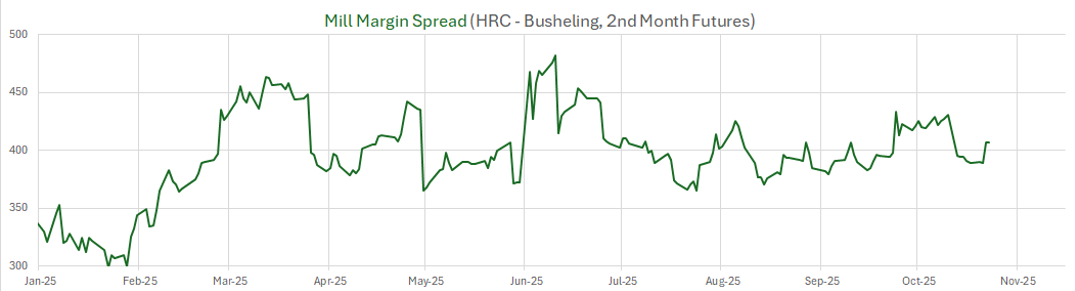

And the mills? They have no reason to intervene. Margins continue to be healthy and impressive (shown below), buoyed by input costs that have eased and competition that has vanished. Imports are nearly nonexistent, rivaling the lows of the Global Financial Crisis (GFC) in 2009, and domestic producers face no real pressure to adjust pricing or chase volume. With mills holding all the cards, they can afford to wait for demand to return on its own terms rather than coax it forward.

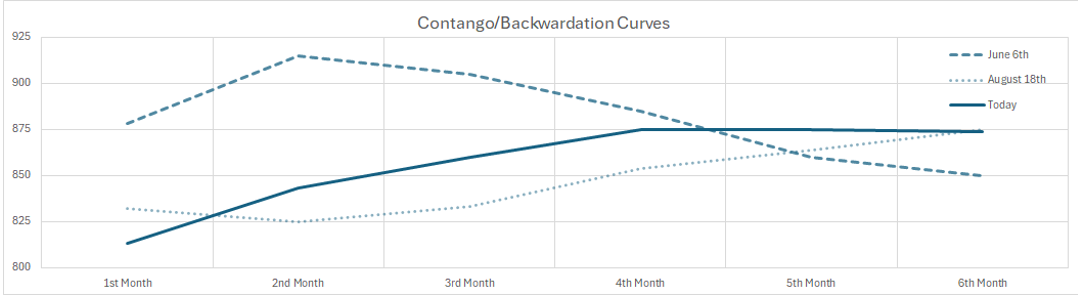

The futures curve reflects the same quiet equilibrium – steady, and uninspired. The chart below shows the sharpest recent contango (surplus) and backwardation (shortage). These market structures are measured by subtracting the 3rd and 6th month futures. The sharpest point of backwardation (dashed line, June 6) represents temporary fear of an assumed shortage of steel, as well as the steepest contango (dotted, Aug. 18) represents recent peak surplus. As we stand today (solid), the market signals a modest surplus.

There is no clear catalyst on the horizon, no fundamental imbalance forcing a resolution. For now, futures sit in stasis along with the physical market – not booming and without a reason to collapse. The rules are written but more in pencil than pen, the artificial floor that is in place cannot be built upon, and the mills are content to watch from above.

Eventually, the page will be turned to either increased confidence and a follow-through from underlying demand, or abrupt change in policy. The problem is that the former would likely only lead to modest increases, while the latter could cause a massive and prolonged upheaval for both prices and inventories.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed should not be treated as a specific inducement to make a particular investment or follow a particular strategy. Views and forecasts expressed are as of date indicated. They are subject to change without notice, may not come to be, and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.