Market Data

November 25, 2025

SMU Survey: Lead times extend across the board

Written by Brett Linton

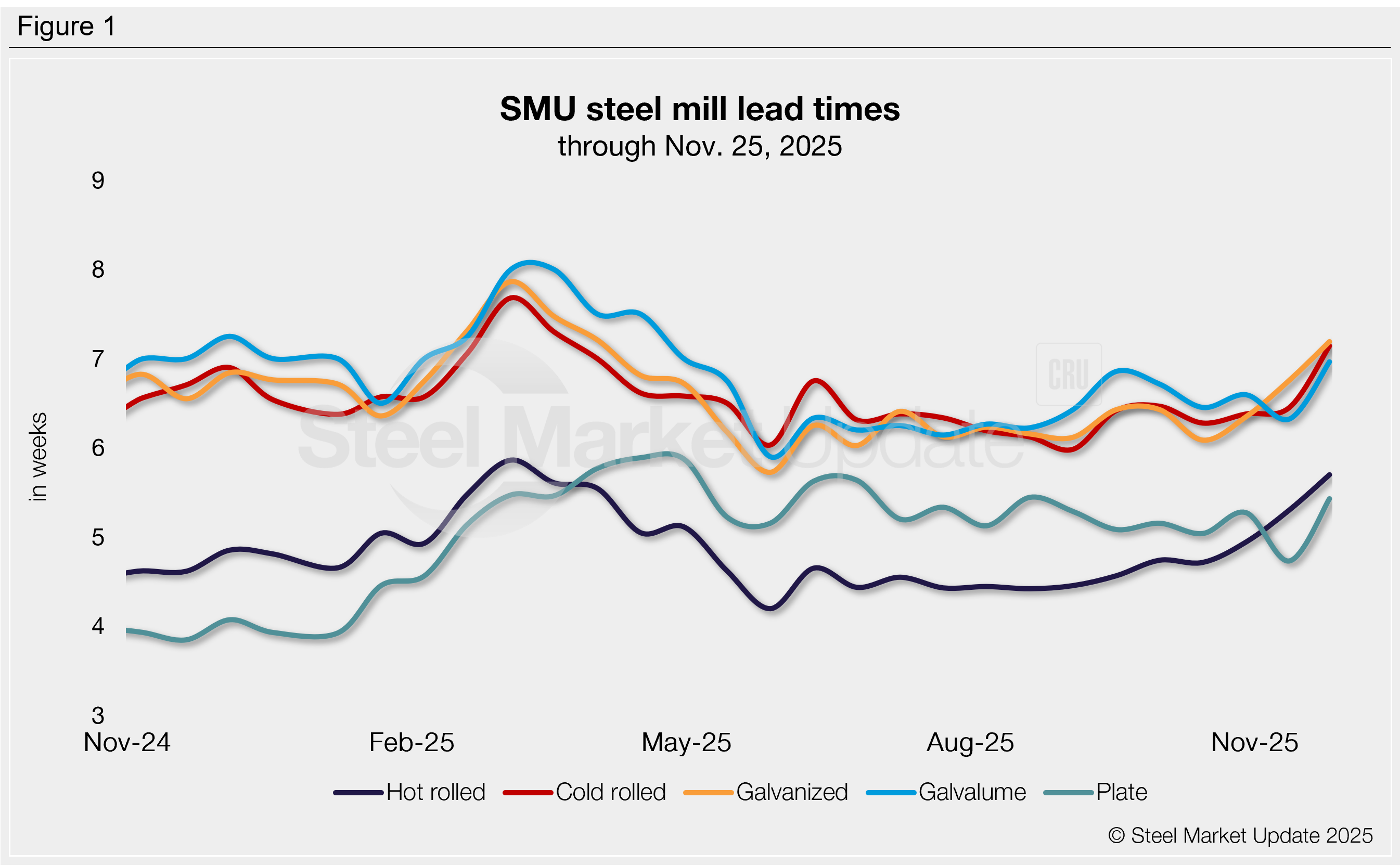

Steel mill lead times extended this week on all sheet and plate products we track, according to responses from SMU’s latest market survey.

Production times extended from our early November survey by half a week on average, but still remain within range of the multi-year lows we saw over the summer.

The average lead time for hot-rolled coil is just over five and a half weeks. Cold rolled and coated products are all around seven weeks. Plate is just under five and a half weeks.

Table 1 summarizes current lead times and recent changes by product (click to expand)

Compared to our previous market check, all five of our lead-time ranges shifted this week:

- The shortest hot rolled and plate lead time considered increased from three weeks to four.

- The shortest cold rolled lead time considered increased from four weeks to five, while the longest increased from nine weeks to 10.

- The longest galvanized and Galvalume lead time considered increased from eight weeks to 10.

Buyer predictions

Most buyers expect lead times to remain stable (46%) or lengthen (44%) over the next two months. In previous surveys this was less of an even split, with more buyers foreseeing stable production times over extensions. Just 10% anticipate lead times to contract, similar to recent surveys.

Here are some of the comments we collected:

“Extending, we are trying to get ahead of the price increases.”

“Extending due to mill planned outages.”

“Flat to extending – remember the pending Fed chair term ends in May.”

“Depends on the product. HRC, CRC, and Galvalume will remain strong, galvanized less so.”

“Flat. Demand will remain strong during Q1, still too early to tell if the demand will continue outside large projects.”

“Contracting, our team is banking on imports coming back into the US and new capacity coming online too.”

“Contracting due to the ‘Market Slowdown of 2026.’”

“Contracting. We believe mills closed December before they were full. If they come back up on schedule, they will start to produce the January orders in December creating a hole.”

Trends

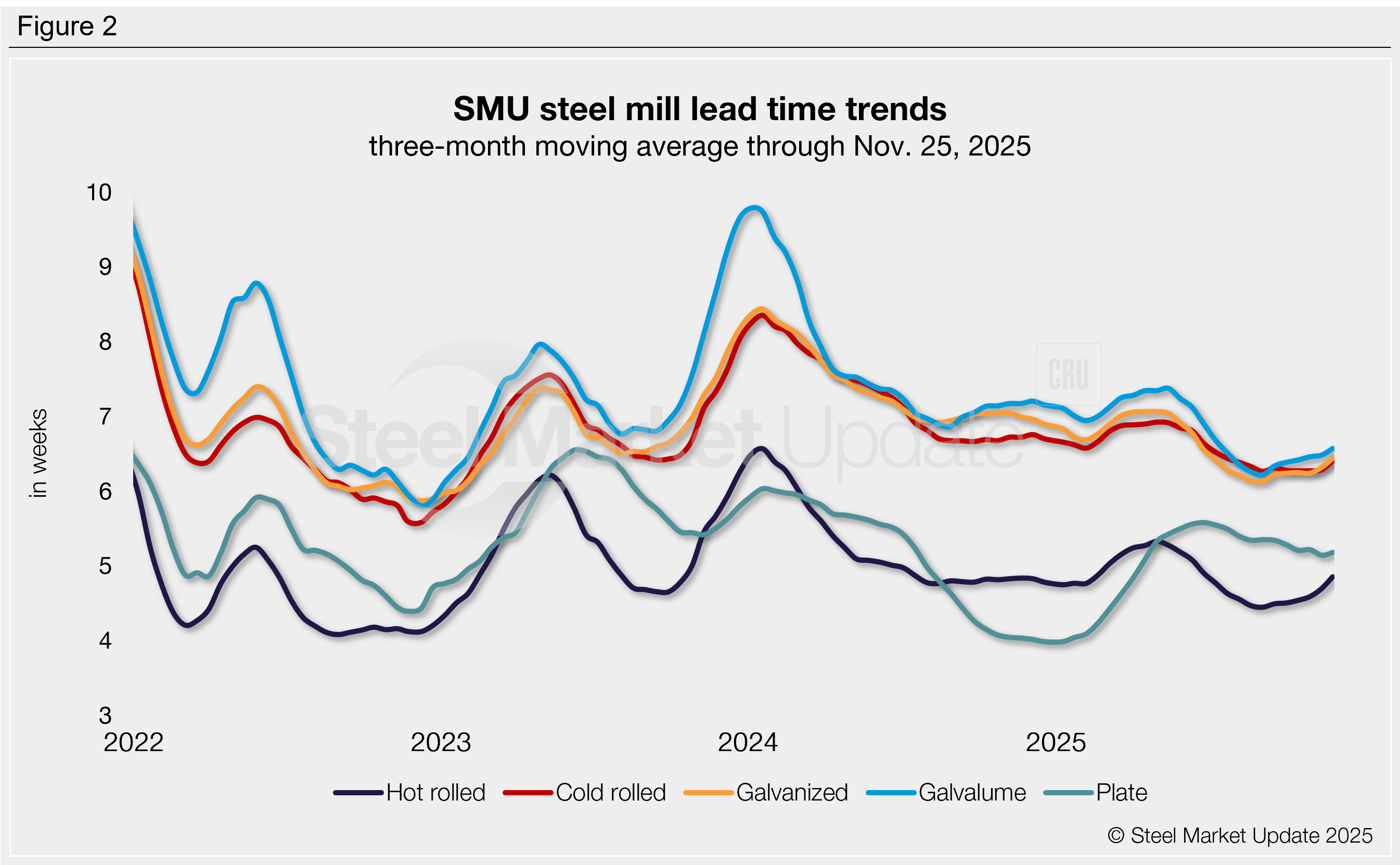

To highlight broader trends, lead times can be calculated on a three-month moving average (3MMA) basis (Figure 2). All five of our 3MMAs increased this week compared to early November.

Overall, sheet 3MMA lead times remain just above the two-year lows seen in early September. The plate 3MMA has trended lower since August but remains about a week longer than it was this time last year.

Average lead times by product across the past three months were: hot rolled at 4.9 weeks, cold rolled at 6.4 weeks, galvanized at 6.4 weeks, Galvalume at 6.6 weeks, and plate at 5.2 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Consult your mill rep for actual lead times. Premium members can view an interactive history of our steel mill lead times data on our website. If you’d like to participate in our surveys, contact smu@crugroup.com.