Analysis

December 19, 2025

CRU: US sheet price increases open the door to import opportunities

Written by Brett Reed & Diego Giangreco

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

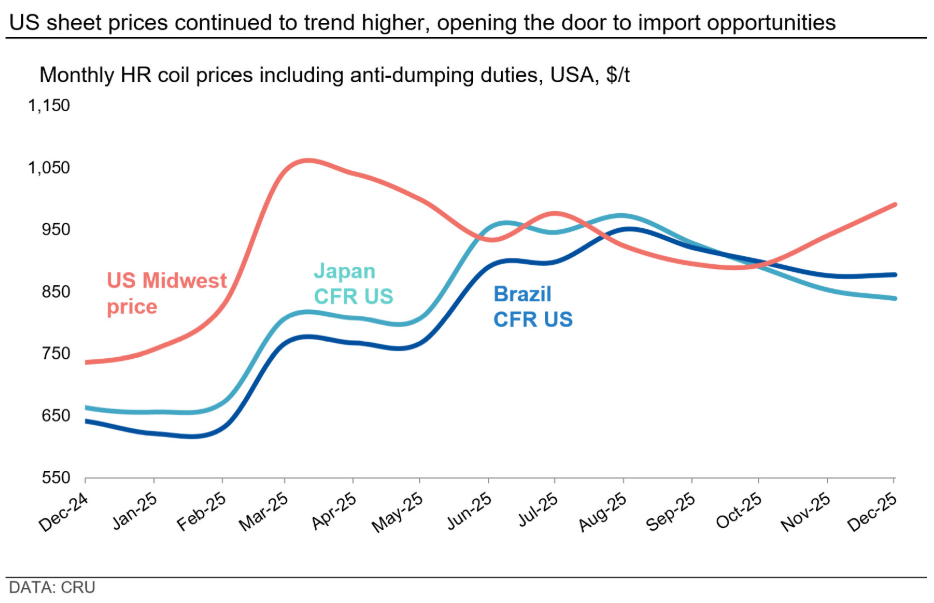

US domestic sheet prices continued to trend higher, with spot prices now high enough for imports to become attractive. Price gains have been most notable for HDG coils, partly due to the finalization of a recent AD/CVD trade case across multiple exporting countries. Meanwhile, imports of longs products trended lower in November as tariffs continued to limit import volumes into the US.

US HR coil prices trend higher, supporting imports

US Midwest sheet prices continued to rise alongside continued mill prices increases as lead times remained extended. Price gains have been most notable for HDG coils, partly due to the finalization of a recent AD/CVD trade case on imports of corrosion-resistant (CORE) steel, with final dumping rates imposed on multiple exporting countries (Australia, Brazil, Canada, Mexico, Netherlands, South Africa, Taiwan, Turkey, United Arab Emirates, and Vietnam). Additionally, HDG coil prices fell at a faster rate from their April peak to the Q3 low vs. HR coil. For the past nine weeks, the spread between HDG and HR coil products has been below $100 per short ton (st) vs. an average of $157/st in the prior 12 months.

While buyers have maximized discounted contract purchases, spot prices are now high enough for imports to become attractive (see chart). The longer lead times associated with imports may still deter new orders, but if buyers expect domestic prices to remain at or above current levels over the near term, more imports are likely to be booked.

As for US domestic long products, prices diverged in early December, with rebar and structurals prices rising on data center demand. Meanwhile, wire rod prices remained flat as demand was soft, although significantly reduced imports supported demand for domestic products. While the US Department of Commerce has updated import statistics from the government shutdown period, final data is not yet available. Thus far, US import license data showed sharp declines across long products in November. Import pricing for most long products has been unfavorable for several months now. Consequently, landed rebar imports fell to approximately 28,000 metric tons (mt, down from 51,000 mt in October, with material primarily sourced from Turkey and Brazil, according to the Department of Commerce. Wire rod imports licenses declined 56% month over month (m/m) to ~47,000 mt in November.

Brazilian slab export volumes increased again in November

Brazilian slab prices decreased m/m in December by $5/mt to $470/mt FOB Brazil. In terms of trade, export volumes increased in November by 21% m/m, with the year-to-date export volumes until November being 19% higher year over year (y/y). The main export markets were the US and Mexico, with 65% of the total volume, but exports to Europe have increased, accounting for 30% of the total, with the rest of the volumes going to Argentina.