Analysis

January 9, 2026

CRU: Venezuelan steel industry in crisis but with a past that shows potential

Written by Erik Hedborg & Thais Terzian & Yusu Mao

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

On Jan. 3, the USA carried out a military operation in Venezuela that resulted in the arrest of the country’s President Nicolas Maduro. As of Jan. 5, the country will be run by interim President Delcy Rodriguez. Nicolas Maduro was preceded by Hugo Chávez, who nationalized the country’s heavy industries from 2007, including steel and iron ore. These policies have remained in place during Maduro’s term as president, and the industry has continued to face significant declines. This CRU Insight provides details on the decline of Venezuela’s steel, DRI, and iron ore industries, which highlights the potential scope of recovery with the right policy agenda and support. However, CRU’s view is there will not be a significant change in the near-term.

Steel capacity utilization: From 100% to 1% in 15 years

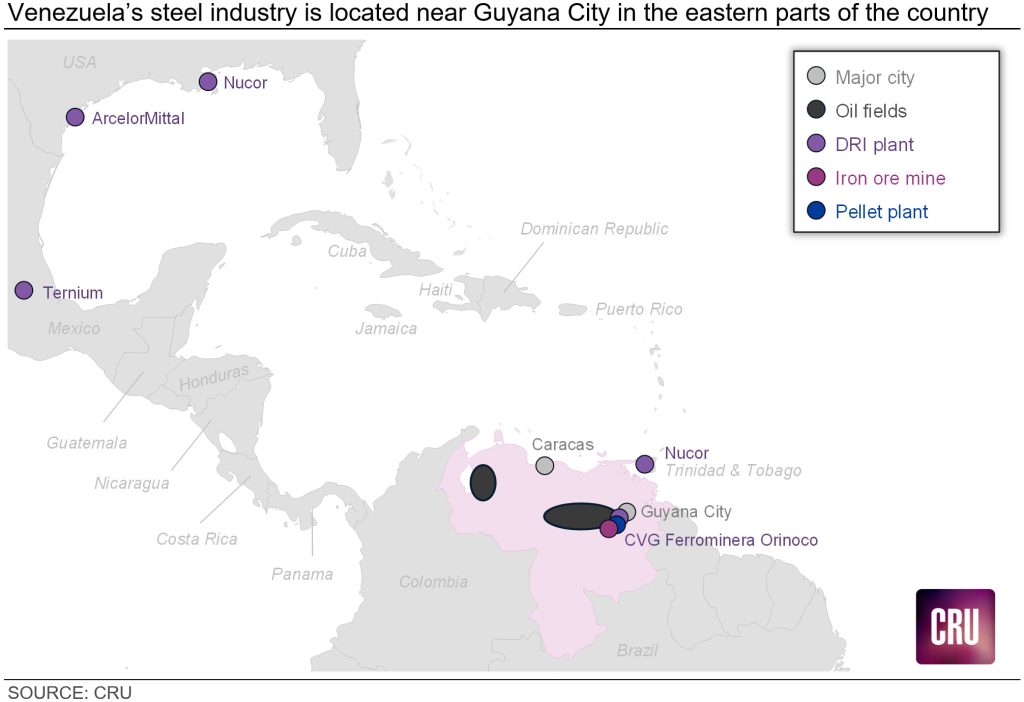

Venezuela’s steel industry has gone through several dramatic changes in the 2000s. The country is home to large iron ore reserves and an abundance of natural gas, which is why the country built its steel industry around DRI production. The raw material (DR pellets) is supplied by the country’s own iron ore producer CVG Ferrominera Orinoco, and the DRI produced by different operators has been delivered to both domestic EAFs and to the export market in the form of HBI. Iron ore mining, pelletizing operations, and DRI production are concentrated in the eastern parts of the country, near Guyana City.

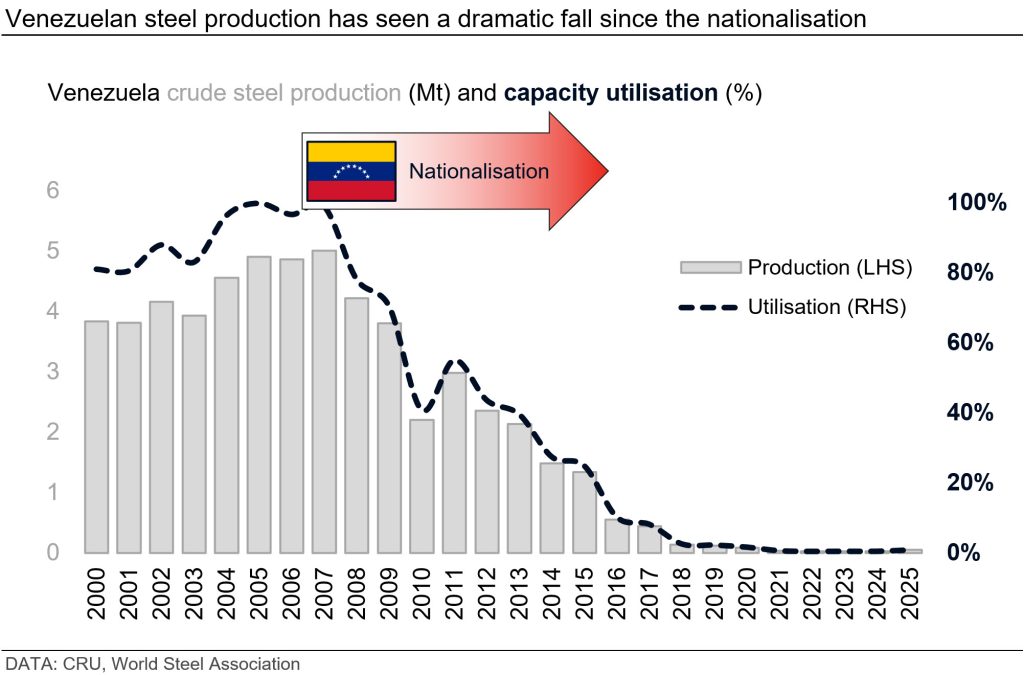

We estimate that Venezuelan crude steel production totaled around 50,000 metric tons in 2025, and the capacity utilization was only 1%. All crude steel production was rolled into long products. The fall in oil production, following the nationalisation of assets and US sanctions, led to limitations on the supply of natural gas and electricity. This curbed the country’s ability to produce crude steel, as the entire production fleet is EAF-based, using natural gas-based DRI as the main raw material. Back in 2007, Venezuelan crude steel production peaked at 5 million metric tons and utilization was close to 100%.

A key global HBI exporter, but no longer the largest

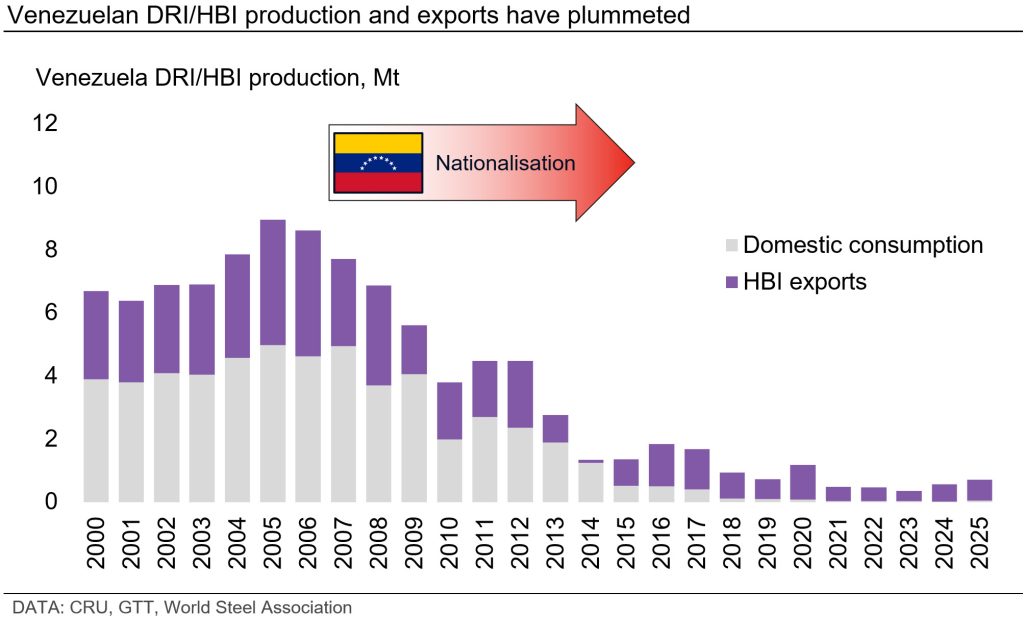

Venezuela is a relevant player in the DRI/HBI market, despite the declines in production and exports. In 2025, the country was the seventh largest HBI exporter globally, with ~0.7 million metric tons of exports destined mainly to Italy, Turkey, and other European countries.

Before nationalization, Venezuela was the world’s largest DRI/HBI exporter, with ~3 million metric tons of exports per year. The main destination for these exports was the US market. Back then, DRI/HBI production outpaced exports considerably as it was also the main raw material to domestic steelmakers. In 2005, DRI production peaked at ~9 million metric tons, and capacity utilization was above 85%. We estimate utilization was below 7% in 2025, while it is likely that part of the previously installed capacity of around 10.3 million metric tons was dismantled in the past years.

Iron ore: Reliant on exports to China for survival

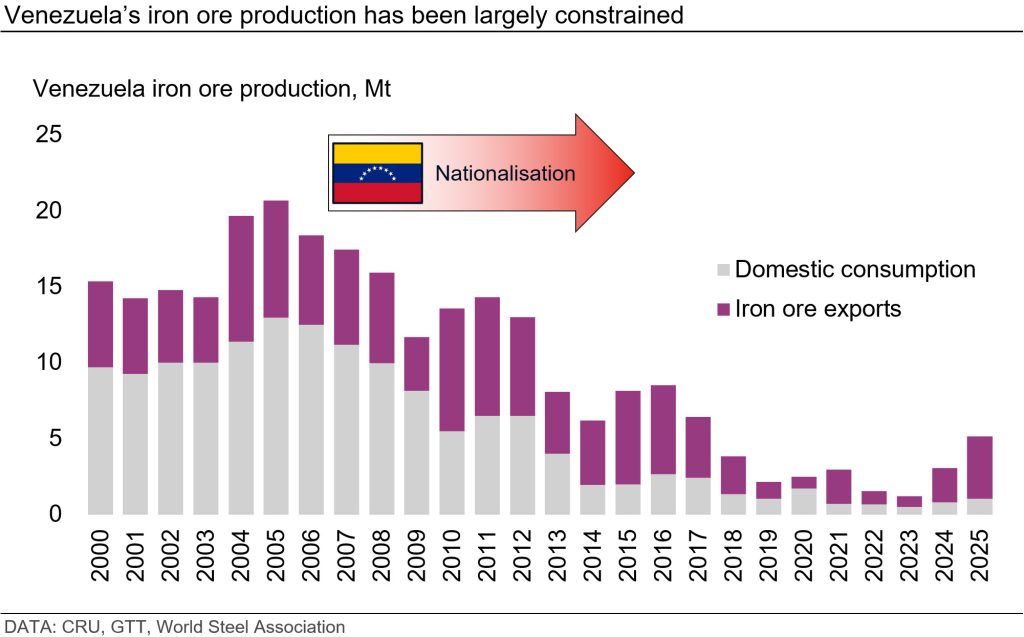

Venezuela has large reserves of high-grade iron ore, suitable for beneficiation and pelletizing. Historically, iron ore production numbers were much higher than today, ranging from 15–20 million metric tons per year during peak periods. Production has been on a structural decline since nationalization and fell below 5 million metric tons in 2018, with the industry operating at below 20% of nameplate capacity ever since. Funding shortfalls and sanction risks largely hinder iron ore outputs and infrastructure maintenance. Deteriorating railway and port facilities, together with unstable power supply, have, in turn, further lowered output.

CVG Ferrominera Orinoco, the state-owned company, owns the iron ore assets near Guyana City. Meanwhile, sources indicate that Jindal Steel & Power (JSPL) took over operations in March 2024 without a transfer of ownership, though details of this arrangement remain unclear. Iron ore output has increased in 2024 and 2025 on higher exports to China.

In 2025, of the ~5 million metric tons of production, ~4 million metric tons, or 80%, was exported to the seaborne market, primarily to China and Trinidad & Tobago, while 20% was consumed domestically. China has emerged as the key export destination over the past two decades, accounting for over 90% of total exports in recent years, and the products are mainly high-grade lump and fines, with a smaller portion of pellets.

Little impact on the steel industry

The recent events in Venezuela will have a limited impact on the global steel industry. Even though a change in government could help to turn the country’s struggling steel industry around, many of the facilities are in desperate need of investments, maintenance, and upgrades. This means it could take years for the country’s industry to recover some of the production lost over the past two decades. As for iron ore, Venezuela has already increased its exports, likely facilitated by JSPL’s takeover of the mining operations, and the country has the potential to maintain or even increase the current level of production.

The DRI/HBI industry is where Venezuela plays a more important role in the global steel value chain. We expect the country to remain a key exporter of HBI, but it is too early to change our forecast, as we need more clarity on who will be in power next and how the new government will treat its struggling steel industry.