Analysis

February 26, 2026

Traders report stronger import interest as domestic HRC nears $1,000

Written by Laura Miller

With domestic steel prices rising steadily and mill lead times pushing out, import offers are becoming more attractive to US buyers.

Increasing orders

“I think there’s been over the last month or two, there’s definitely some more imports booked,” one trader told SMU.

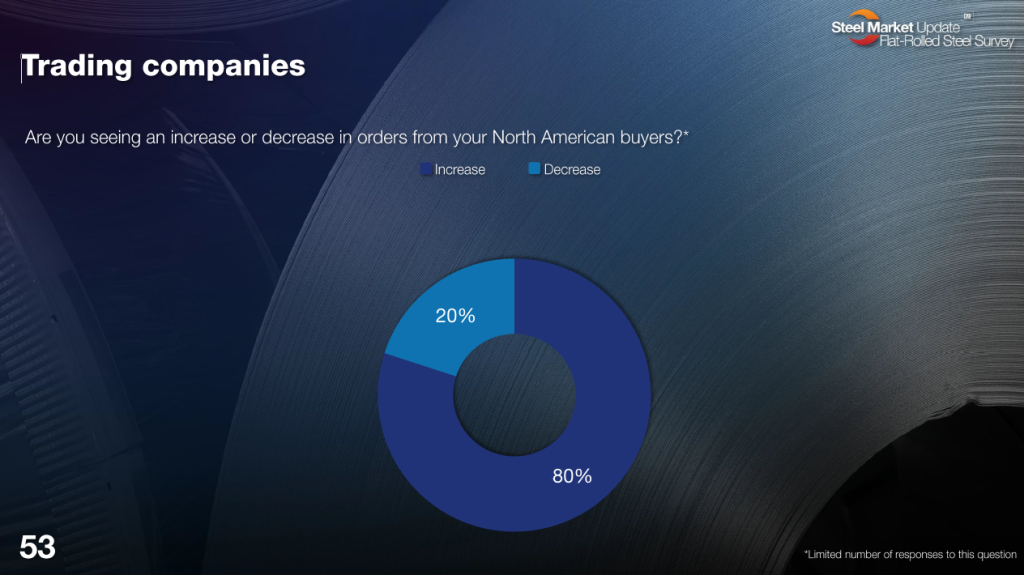

His comment aligns with SMU’s latest full survey results, which show increasing orders from traders’ North American buyers. At the start of the year, just 37% said orders were increasing. In last week’s survey, that figure grew to 80% seeing increasing orders (slide 53).

One trading company reported it as a seasonal uptick. Another clarified orders are “flat to slightly up. But not by a lot.”

“We have crossed into the territory where import pricing is better than domestic,” one manufacturer relayed to SMU. “We are being told there are spec tons either here or on the water, too.”

A service center agreed that “some [imports] have gained our attention.”

More competitive prices

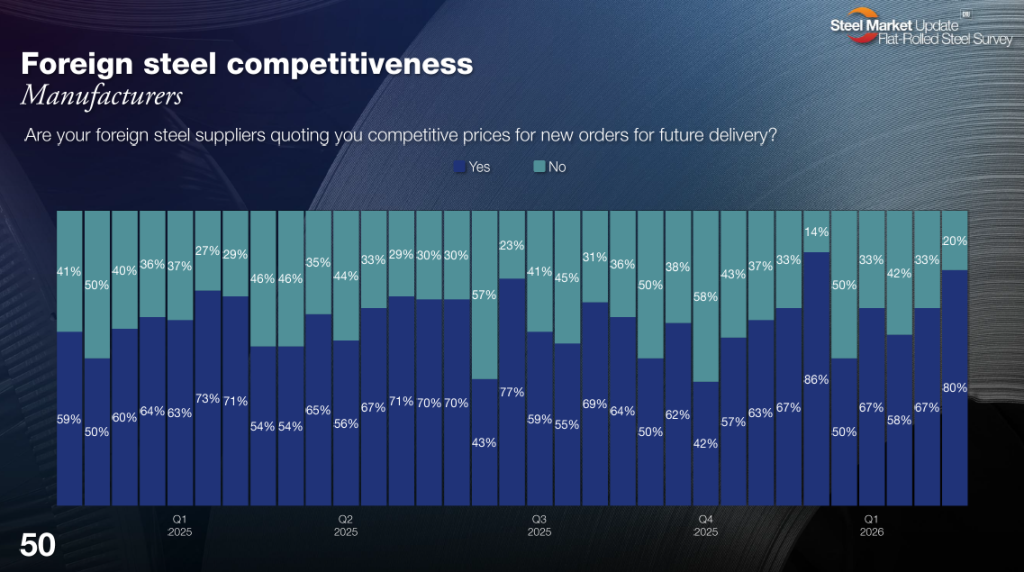

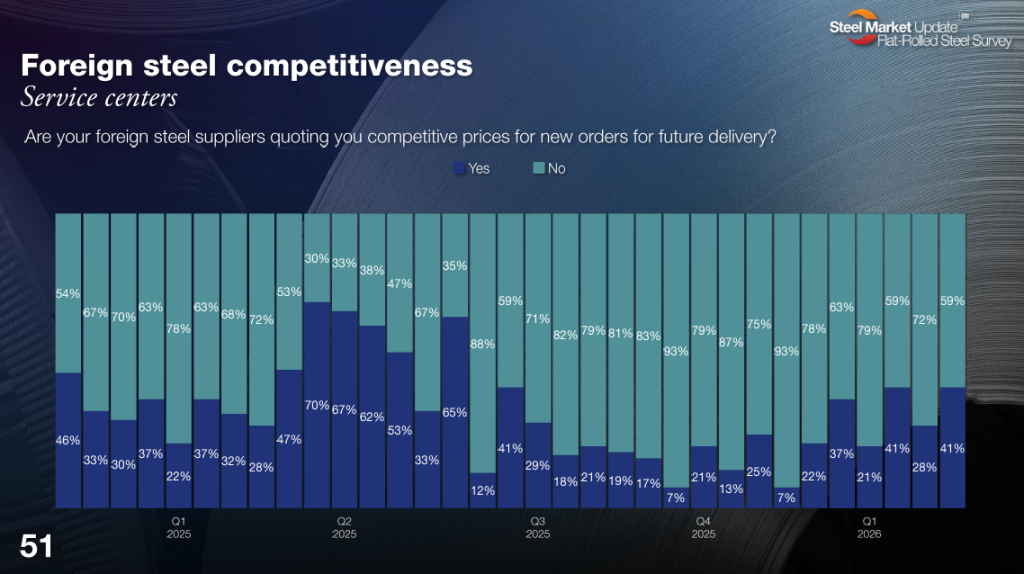

More manufacturers (80% slide 50) report competitive prices for new orders of foreign steel for future delivery than service centers (41% slide 51).

One service center source, for example, said imports remain unattractive due to longer lead times associated with overseas material. Another cited uncertainty around tariffs as a potential deterrent.

Orders placed now with overseas mills might not ship until May, which could push delivery into the summer months, one trader said. Still, lead times at US mills are also pushing out, with many reports of mills running late on orders, he added.

“Domestic mills are very late,” a manufacturer source agreed. “Without imports, they cannot keep up with demand.”

Some imports more attractive than others

Comments from survey respondents revealed that certain imports are more attractive, especially those that aren’t produced extensively in the US.

“Only on light-gauge painted,” reported one manufacturer.

“Pre-painted products (galvanized or Galvalume bare) are definitely attractive enough to be bought,” commented another trader.

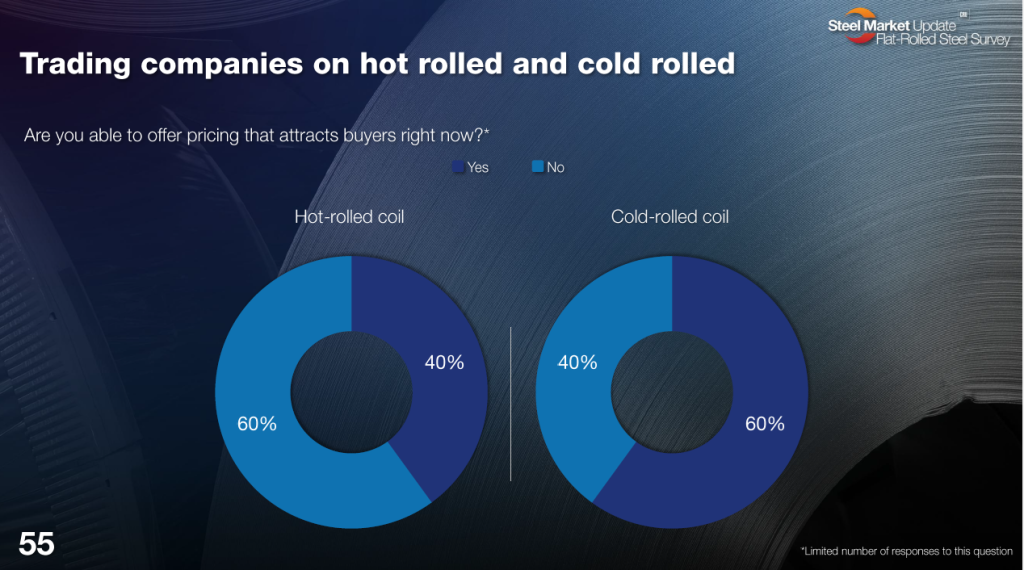

Breaking it down by product, we can see that cold-rolled coil (CR) offers are the most appealing, with 60% of traders reporting them as attractive (slide 55). One buyer said domestic mills aren’t as willing to negotiate CR pricing, which jives with SMU’s latest report on negotiation rates: CR showed the lowest negotiation rate (20%) among the five flat-rolled products we track.

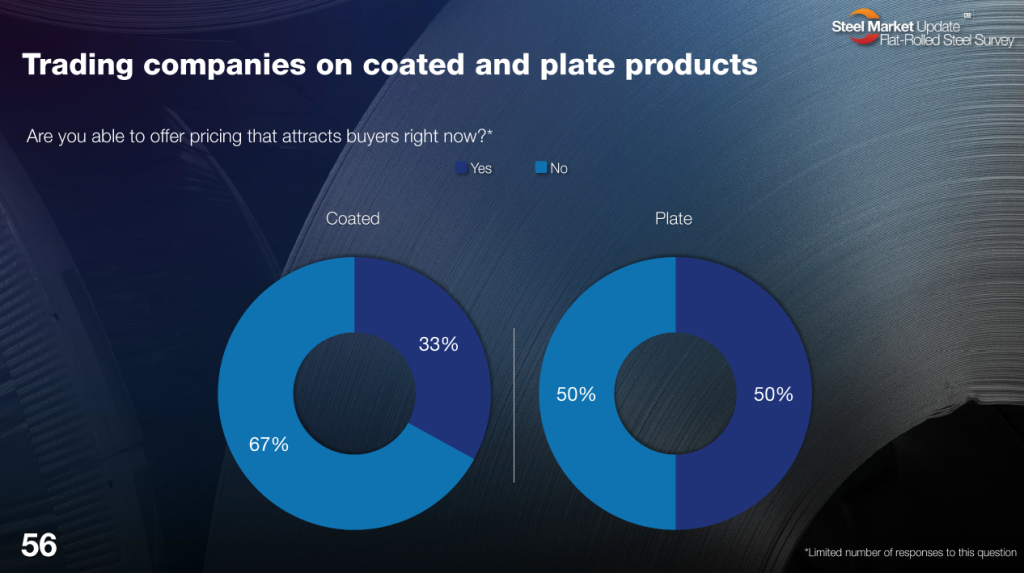

Traders are split 50/50 on being able to offer attractive plate pricing, while just 40% can offer solid hot rolled prices. Coated products remain the least attractive, with just a third of traders reporting they can offer competitive pricing (slide 56).

Pricing

One trader commented that the market is “skewed” and “weird” at present, as there are few offers from traditional major trading partners Canada and Mexico.

SMU did hear of hot-rolled coil being offered into the US from Mexico for $950 per short ton (DDP US port).

Another offer was heard for Korean HRC at $850/st for late April/early May delivery.

SMU also heard that at least one major domestic mill that recently lost an order in the Houston market due to imports beating its price.

This week’s SMU price assessment shows domestic HR prices ranging from $960 to $1,000/st, with an average of $980/st.

Just two weeks ago, domestic HR prices, at $975/st on average, were about $50/st below landed import prices, inclusive of the 50% tariff.

We’ll publish another domestic vs. foreign HRC price analysis in Sunday’s newsletter.

Editor’s note: We’d love to see more traders participate in our surveys. If you’re involved in the steel trade and would like to make your voice heard, please reach out to us at smu.editorial@crugroup.com.