Analysis

March 6, 2026

Ferrous scrap market chatter this month

Written by Ethan Bernard

Every month, SMU polls participants in the ferrous scrap market on a variety of topics. These include prices, business conditions, and tariffs, among others.

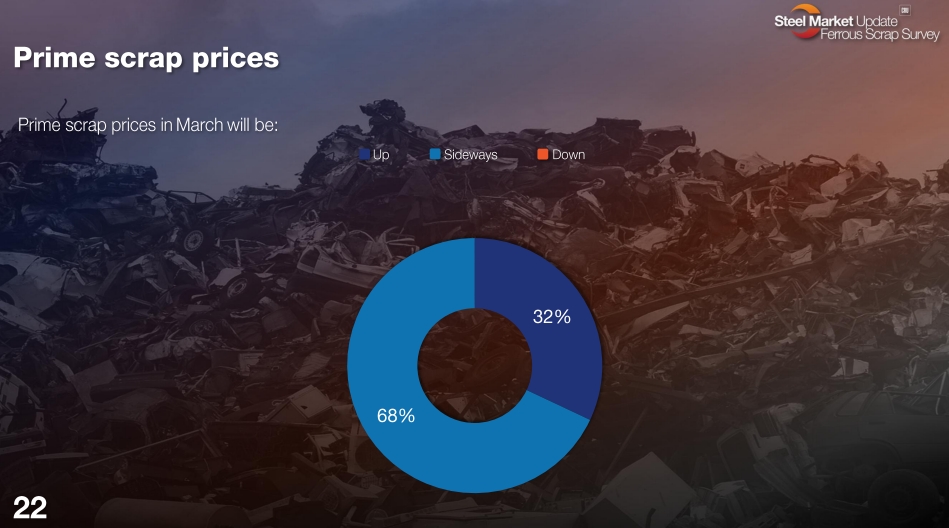

This month’s survey arrived just as the March trade was settling. With nearly 70% of respondents saying prime scrap prices would land sideways, the vast majority seemed in line with market consensus.

Let’s take a look at what else these participants are seeing on demand, tariffs, and pricing. We’ll post the slides, followed by a few respondents’ comments.

Want to share your thoughts? Contact david.schollaert@crugroup.com to be included in future market questionnaires. (For Premium subscribers, the full results are available here.)

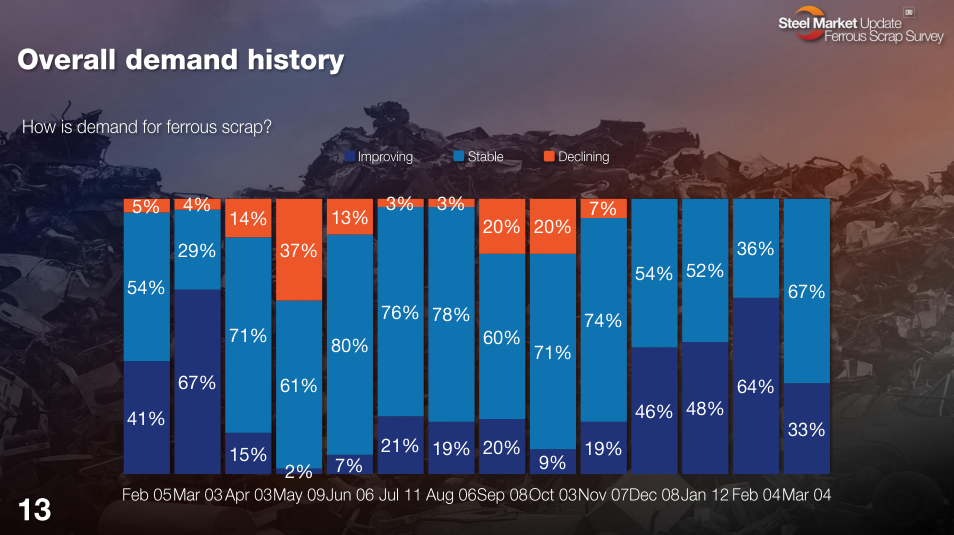

How is demand for ferrous scrap?

“Order books at the mills are full.”

“Demand for steel is increasing, allowing domestic scrap pricing to increase.”

“Plenty of supply, even in light of poor weather.”

Prime scrap prices in March will be:

“Demand is increasing.”

“Could be down a bit, especially in the South.”

Where will busheling prices be in March?

“Demand is up and steel pricing has increased domestically.”

“General demand improvements, and rising steel prices.”

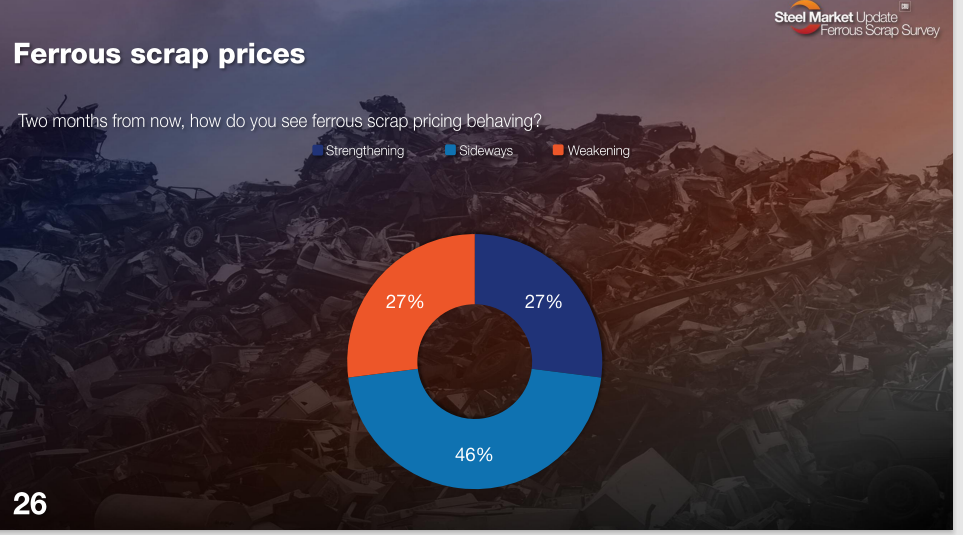

Two months from now, how do you see ferrous scrap pricing behaving?

“Obsolete supply catching up to demand.”

“The market will top out in March due to demand and supply levels.”

“I’d like to think sideways at worst. However, talk is scrap will flow better and potentially down. Maybe a quick boost. But not sustainable with down numbers.”

“Seasonality.”

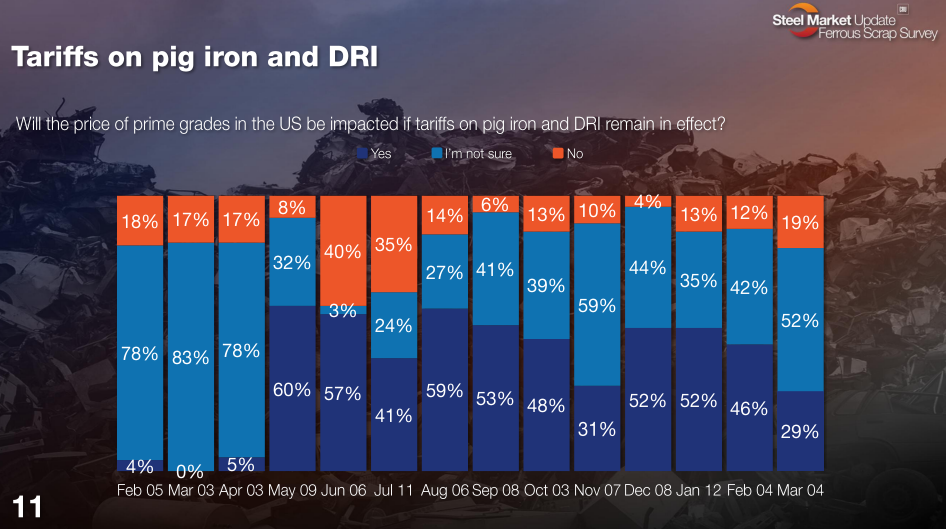

Will the price of prime grades in the US be impacted if tariffs on pig iron and DRI remain in effect?

“If tariffs continue to affect pig iron and DRI, it makes scrap more attractive.”

“Tariffs and local capacity limits.”

“Busheling that is here ready for prompt delivery waiting for cargo. Now war.”

(For a look at SMU’s Stephen Miller take on what is happening now with tariffs on pig iron, click here.)