CRU

March 10, 2026

CRU: Middle East Conflict - The impact on metallurgical coal and iron ore

Written by CRU Group

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

This insight demonstrates how the conflict in Middle East supports metallurgical coal prices and iron ore will be impacted by a potential decline in demand from China and rising costs, while the pellet market will be severely disrupted.

Metallurgical coal prices to be supported

CRU expects the metallurgical prices to be supported by the conflict in the Middle East. Up to 25% of global seaborne crude/refined oil and LNG flows through the Strait of Hormuz. Constrained supply from the region has already led to a spike in oil and gas prices. Rising natural gas prices will lift thermal coal prices above the price for low-quality coking coal.

Our analysis concludes there will be limited direct impact on metallurgical coal and coke prices from demand destruction in the Middle East. The region consumes only 3 million metric tons (mt) per year of coke, ~40% of which is imported. Middle East steel production is geared towards the DRI-EAF route, with Iran being the only country to house BF and coke capacity. It consumes ~2.8 million mt per year of coke to produce 3.5 million mt per year hot metal, importing ~33% of its coke requirement. Iran’s coking coal is sourced domestically, while its coke imports are mostly from China.

Having said that, the metallurgical coal market will still see significant repercussions if the duration and scale of the conflict expand. Metallurgical coal is ultimately an energy commodity that is:

- …exposed to oil price-linked cost escalation in mining/production as well as transport

- …exposed to market substitution with thermal coal which acts as a price floor for SSCC

- …exposed to higher freight costs and longer transit times for Pacific-Atlantic coal trade.

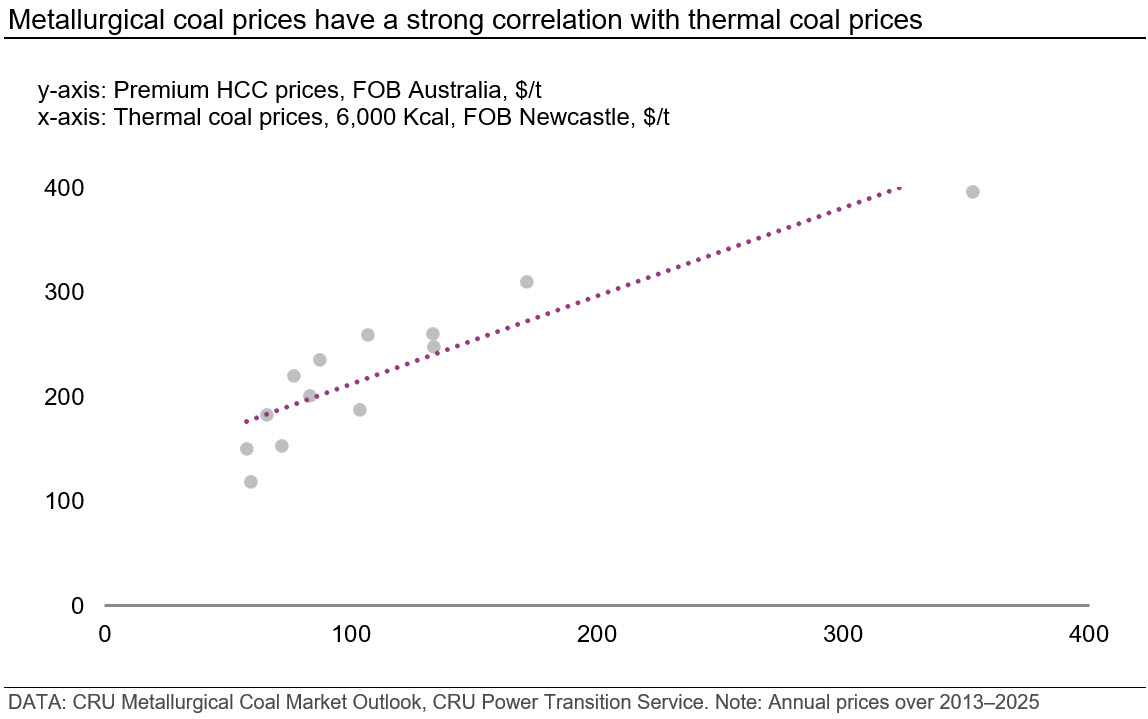

According to our recently published insight Middle East Conflict: The impact on LNG and thermal coal, thermal coal prices are forecasted to rise by $5–10 or $10–15 per mt depending on the duration of the war between the USA/Israel and Iran. This indicates a corresponding increase in seaborne premium HCC prices by $4–8 or $8–13 per mt. This is subject to further adjustments by factors such as the general cost inflation due to higher energy prices, higher freight rates, etc.

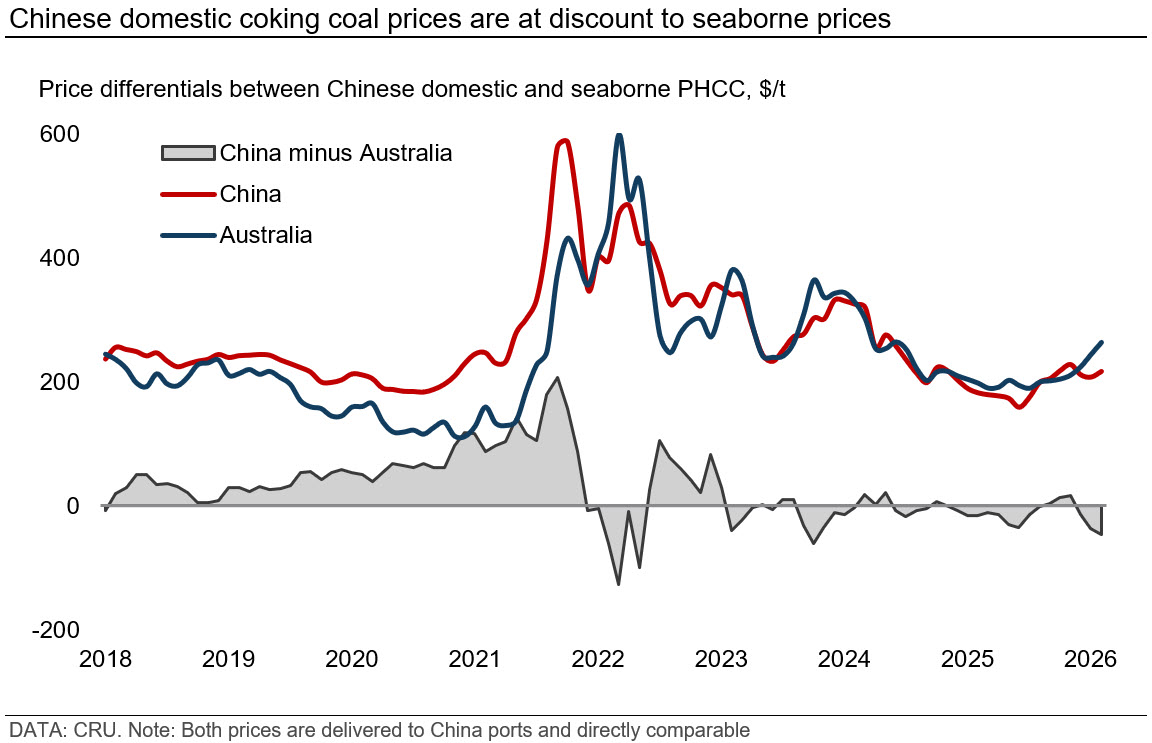

Chinese domestic metallurgical coal prices are expected to be more shielded from the conflict. Despite the risk of supply disruptions of crude oil and LNG in Middle East, China has diversified supply and sufficient inventories of these energy products. In addition, the domestic thermal coal market has seen a loose balance prior to the conflict, indicating sufficient thermal coal capacity and low necessity of drawing switchable semi-soft coking coal from the metallurgical market to the thermal market. Meanwhile, China has extra metallurgical coal supply from Russia and Mongolia that many countries are unable to access.

As a result, we forecast the current discount of Chinese domestic coking coal price to the seaborne price will persist. This indicates spot demand for metallurgical coal from China will vanish in the seaborne market in the near term.

The impact on iron ore prices is more unpredictable

The conflict in the Middle East is not expected to shift the global iron ore market much, as the region accounts for only a small share of seaborne trade. However, there are severe impacts on costs and the DR pellet market, which is highly sensitive to any disruptions at the Strait of Hormuz.

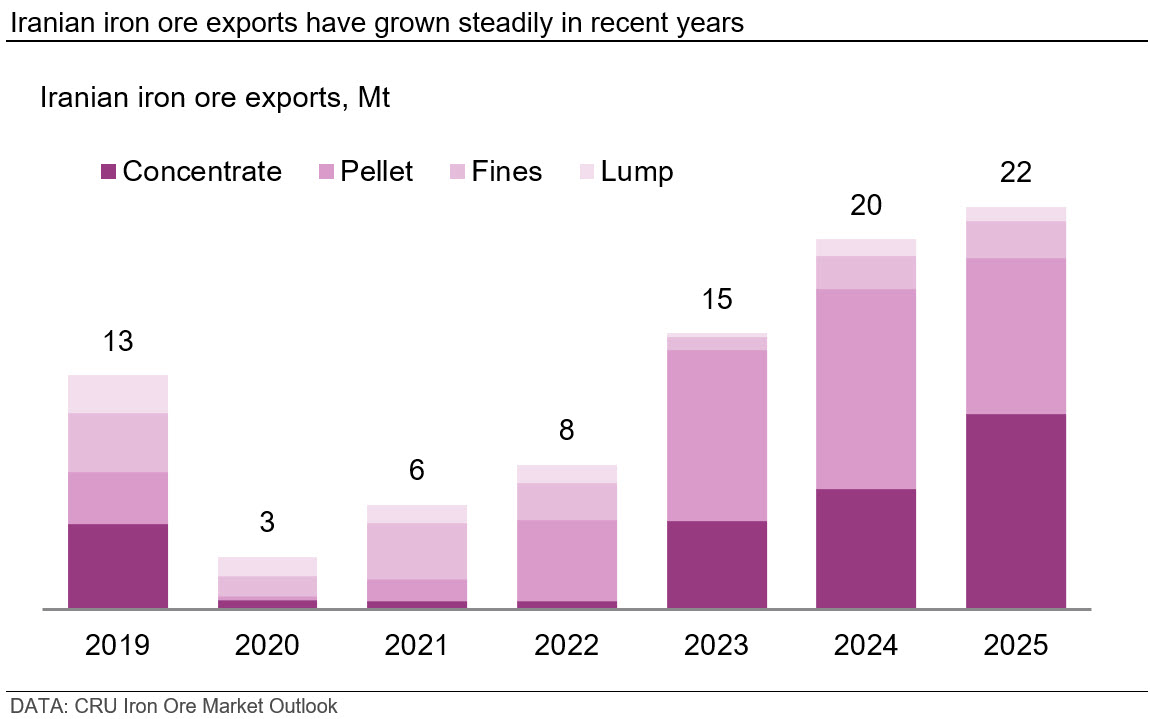

Iran is the largest iron ore producer and exporter in the region with its seaborne supply being mostly sold to China directly or through Oman and the UAE. According to our estimates, Iran’s iron ore exports have increased steadily over recent years with the volume reaching 22 million mt in 2025, consisting mostly of concentrate and pellets.

Iran’s iron ore exports have stalled as shipping through the Strait of Hormuz is disrupted by war. The scale of disruption will depend on how long the conflict drags on. Prior to the conflict, we already expected Iran’s exports to fall to ~17 million mt this year, and the conflict adds further uncertainty to Iran’s ability to keep exports high.

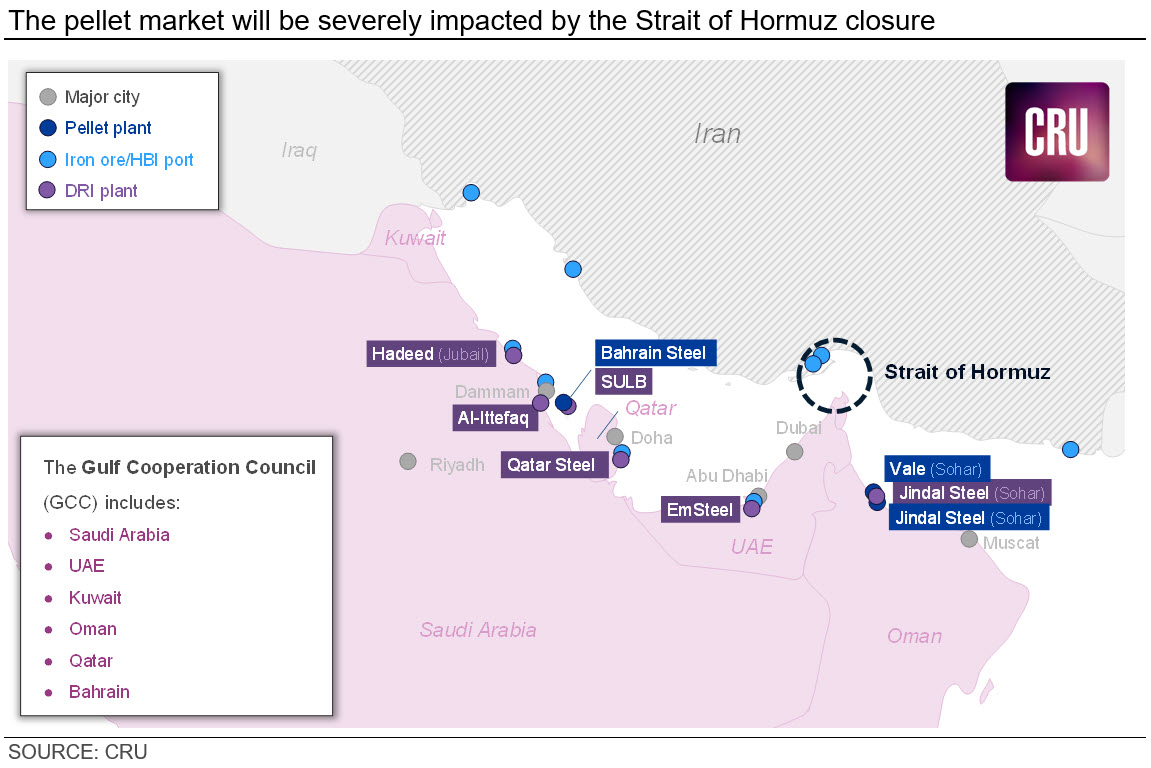

The disruption in the Strait of Hormuz has also blocked the inflow of iron ore into the Middle East. Pellets and pellet feed that previously moved into the Persian Gulf will now have to find alternative markets while key DRI and pellet producers in the GCC region face the risk of having to halt their operations due to their raw materials shortages. In 2025, steelmakers in the Persian Gulf produced 14 million mt of DRI. This generated 21 million mt of pellet demand, which was either imported through the Strait of Hormuz or produced locally by Bahrain Steel, which in turn imports all its pellet feed through the same route.

Another impact will market access for pellet producers in Oman, just outside the Strait of Hormuz. In Sohar in northern Oman, Vale has two pellet plants (9.5 million mt per year capacity) and Jindal Steel has recently commissioned its 6 million mt per year pellet plant. Vale is a key supplier to the GCC region and, if the company maintains pellet production, will have to find other markets for its pellets as long as the strait is closed. There are, however, signs in the market that Vale is reducing pellet production in Oman.

We expect initial pressure on the pellet premium, followed by a wave of restocking in the GCC region once the strait opens. In China, there is potential for the pellet premium to lift as the country will likely be seeing less imports from Iran going forward. In 2025, Iran accounted for 9 million of China’s 23 million mt of pellet imports.

Within China, another factor indirectly weighing on iron ore demand is the potential reduction of Chinese steel exports. We heard from our market contacts that steel export offers from China to Middle East have declined since the war started on February 28. Chinese steel exports to Middle East have grown steadily since 2021 and reached ~17 million mt in 2025. China’s indirect steel exports through sales of steel-containing goods have also grown and were as high as 10.4 million mt in 2025 based on our estimate. A combination of these indicates an average of ~2.3 million mt steel exports per month to the region in 2025. A complete loss of these exports will result in a loss of iron ore demand by 3.5 million mt per month.

As the iron ore clearing market, China will potentially see a reduction in both iron ore demand and iron ore supply, considering the ~20 million mt of imports from Iran, making the iron ore price moves more unpredictable. That said, what is certain is the higher fuel and energy prices will push up the cost of trucking, processing, and shipping iron ore all over the world. In other words, the cost curve will rise, and iron ore producers will seek higher prices to cover their rising costs.

In summary, the Middle East conflict is expected to push up global metallurgical coal prices, more in the seaborne market and less so in the Chinese domestic market. The impact on iron ore prices will be more unpredictable as the conflict will likely reduce both supply and demand in China. That said, iron ore prices will be supported by higher costs. As the incident is fast-moving, please stay with us for further update.