Analysis

March 27, 2026

CRU Outlook: Middle East tensions will drive steel prices higher

Written by Juliana Guarana

This item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

APAC steel prices are expected to rise due to high energy and freight costs stemming from the Middle East conflict. Imports will remain subdued in the EU due to rising freight rates but are expected to pick up marginally in the USA.

Conflict driven input costs will raise APAC steel prices

Chinese steel export prices are expected to rise marginally in the coming weeks, as the ongoing recovery in restocking activity is anticipated to support domestic steel prices and export offers. In addition, higher freight and energy costs stemming from the Middle East conflict are expected to continue to underpin Chinese steel export prices.

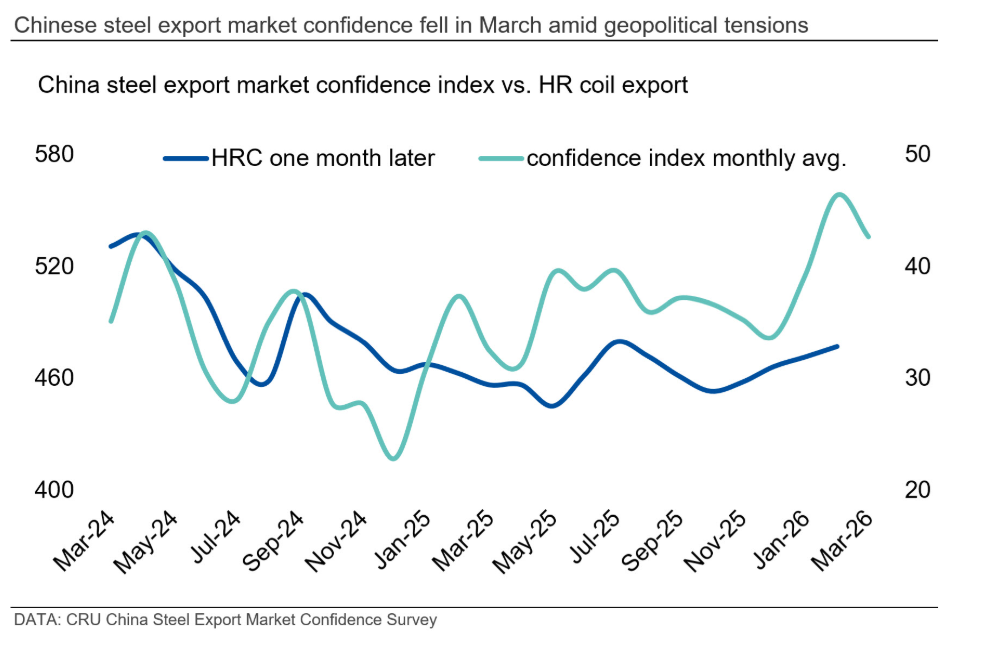

However, ongoing shipping disruptions due to current geopolitical tensions have impacted market confidence, as reflected by our Chinese steel export market confidence index (see chart below). Therefore, Chinese export price increases are expected to be limited, as overseas trading is set to remain subdued and Chinese exports to the Middle East may need to find alternative markets if the conflict persists for longer.

In Southeast Asia, steel prices are also expected to rise in the coming weeks due to stronger seasonal demand. The conflict in the Middle East will provide further cost support to prices, given rising freight and raw material costs. Moreover, the ongoing disruption to the supply of semi-finished products from Iran to Southeast Asian re-rollers is also likely to translate into higher steelmaking costs in the region.

In India, HR coil export prices may face downward pressure in the coming weeks as buyers in the Middle East have suspended orders due to the ongoing conflict. Moreover, EU buyers are likely to remain on the sidelines given uncertainty over freight costs, logistics risks and Q2 arrival timings.

Freight cost uncertainty will limit interest in imports in the EU

In Europe, domestic steel prices are expected to continue rising in the coming month as regional buyers will continue to shift towards domestic supply due to CBAM charges and freight risks from the Middle East conflict. Higher energy and slab costs will also support steel prices in the EU.

In the USA, domestic steel prices are also expected to further increase in the coming weeks, given strong demand and tight supply. Light flat-rolled steel imports into the USA are expected to pick up marginally despite rising freight rates, as the spread between the US Midwest price and landed import prices from key origins is currently significant (please see our GSTS pdf for more information on landed import prices).

Brazilian slab export prices are expected to remain supported by increased demand from the US and European markets, as well as the suspension of Iranian slab exports, given the ongoing conflict.

The duration of the conflict in the Middle East is the key variable in near-term price direction. CRU’s current base case is 6-8 weeks of disruption in the Strait of Hormuz.