Analysis

April 10, 2026

CRU: Sheet prices continue rising as the Middle East conflict drags on

Written by Shankhadeep Mukherjee

This item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

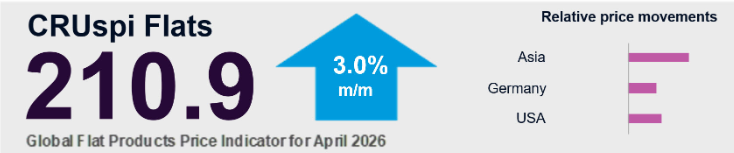

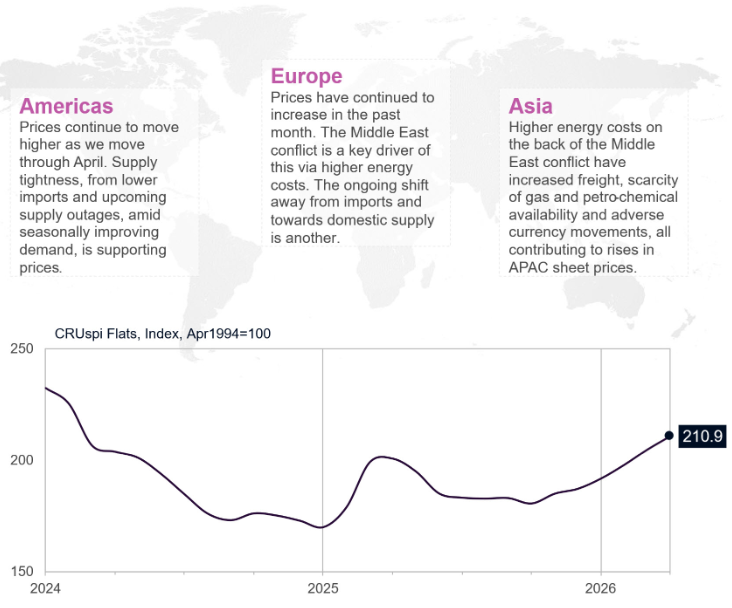

CRU’s Global Flat Products Price Indicator (CRUspi Flats) stands at 210.9 in April 2026, up 3.0% m/m. The Middle East conflict continues to be the principal factor in rising prices, as its impact is now being felt throughout the supply chain. Coated sheet prices have borne the larger brunt of the impact. This is despite there being no evidence of a broad-based demand recovery across the globe.

The Middle East conflict continues to drive higher costs through the steel supply chain

The Middle East conflict has pushed costs up as higher energy prices ripple through the supply chain, and it is the principal factor behind this month’s price uptrend. That is despite a predominantly integrated production route globally, where the steelmaking process itself is an important source of energy.

The increase in oil prices has resulted in higher freight costs, which have increased transportation costs, both on sea and on land, increasing the landed cost of important raw materials.

Iron ore prices have increased by around $10 per metric ton since the start of March, as higher oil and gas prices have lifted the cost of producing and delivering iron ore. Together with high freight rates, there has been a strong cost push for iron ore prices.

Coking coal prices have increased modestly; however, the limited availability of diesel in key producing areas has introduced a risk factor. Countries like India, which depend a lot on the Middle East for their energy requirements, have seen their currency depreciate on the back of increasing oil prices. This has made landed coking coal costs expensive for Indian mills.

Meanwhile, the surge in gas prices has significantly impacted the energy-intensive electric-arc furnace (EAF) mills, though the proportion of sheet produced through this route is low globally and varies by region. APAC and Europe have low shares of EAFs, while regions such as Turkey and the US have higher shares.

Coated sheet prices have been impacted the most of all sheet prices

Within our portfolio of sheet prices, coated sheet prices have seen a bigger impact. This is because standalone coated sheet producers do not have the benefit of access to process energy that integrated producers have access to.

Also, the coating process requires the use of oil by-products and gas for treatment and melting. The Middle East conflict has tightened the supply of these products and increased these input prices. Consequently, coated sheet prices have seen the bigger impact.

There is no evidence of a broad-based demand recovery across the globe

While pockets of demand keep emerging, it remains generally fragmented and not sufficient to absorb the full impact of rising production costs. In APAC, transaction volumes remained modest across most markets. In China, there is a seasonal demand pick-up, but this recovery in demand is not strong enough, as a rapid supply response has contained any recovery in profit margins. In India, many buyers are waiting for prices to reduce.

In the US, demand is holding up, but macroeconomic indicators remain mixed with 30-year mortgage rates jumping back up to nearly 6.5% in the first week of April, and inflation expectations are rising for the near term due to the ongoing conflict. Manufacturing data, however, has been more positive, with the general PMI and new orders expanding for three straight months.