SMU Steel Summit 2025: These panels break it down

We’re just 88 days out from North America’s largest gathering of the flat-rolled steel industry.

We’re just 88 days out from North America’s largest gathering of the flat-rolled steel industry.

Mill lead times shrunk this week for all of the sheet products tracked by SMU and held steady on plate, according to buyers responding to our latest market survey.

Most of the surveyed US and Canadian metalforming manufacturers expect general economic activity to remain steady over the next three months.

“Unless the administration actually gets serious about levelling the playing field… for consumers of steel, then everything they've done on the steel side is useless."

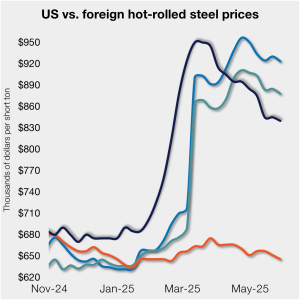

Domestic hot-rolled coil prices moved lower again, maintaining the downward move seen in eight of the last 10 weeks.

Most steel buyers responding to our latest market survey report that domestic mills are willing to talk price to secure new orders. Mill negotiability has continued to rise across all sheet and plate products we track, now at some of the highest levels recorded since late 2024.

SunCoke Energy has purchased Phoenix Global, a metals and mining services company, for $325 million.

The US mills have managed to reduce pig iron prices to correspond with the sharp declines in domestic scrap prices in May.

I sort of expected big news last Friday and over the long, Memorial Day weekend. Because that's become more the norm than the exception for steel this year. Sure enough, Trump posted on Truth Social on Friday afternoon that he had given his blessing to a “partnership” between Nippon Steel and U.S. Steel. And then over the weekend we had market moving new on tariffs, this time involving the EU.

Total US mill output rebounded last week to the highest rate recorded since last September, according to raw production figures released by the American Iron and Steel Institute (AISI).

Sheet and plate prices marginally declined again this week for the second consecutive week, pausing the strong downward trend seen from April through early May.

Oil and gas drilling activity declined in both the US and Canada this week, according to Baker Hughes.

We're going to have to wait a bit longer for the final outcome of the Nippon/USS deal.

Steel Market Update will be taking time off in observance of Memorial Day.

Global raw steel production dipped from March to April, according to the latest release from the World Steel Association.

Here are highlights of what’s happened and a few things to keep an eye on this upcoming week.

According to our latest analysis, prices for four of the seven steelmaking raw materials we track increased from April to May. However, select materials saw a collective 1% decline month over month and are down 4% compared to three months ago.

Metallus shuffles the management deck with new appointments.

One cause of this was increased competitiveness from imports that have put pressure on some domestic producers.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Sure, demand isn’t as good the market had hoped it would be earlier this year. But assuming it doesn’t fall of a cliff, buyers will have to restock at some point. And that might give domestic mills enough leverage to raise prices again.

Most sheet and plate prices edged lower again this week, albeit at a slower pace compared to the movements seen over the last seven weeks. Buyers remain cautious and hesitant to hold onto much inventory, citing lingering demand concerns, ongoing tariff uncertainty, and a potentially weakening scrap market in June.

Following three weekly increases, domestic mill output edged lower last week, according to the American Iron and Steel Institute (AISI).

While I would anticipate market sentiment to pivot and improve if all the questions around tariffs were answered, that still leaves us with a few other factors.

Market participants in both the US and Europe noted that most buyers are patiently waiting for prices to reduce as they have enough inventory at hand.

SMU’s Buyers’ Sentiment Indices resumed their downward trend this week, erasing the modest recovery seen two weeks ago.

Let's see what SMU survey respondents are saying about Trump's tariffs.

SMU’s Mill Order Index (MOI) declined for a second straight month in April after repeated gains at the start of the year, according to our latest service center inventories data.

Sheet and plate lead times declined across the board this week, according to buyers responding to the latest SMU market survey. While our lead time ranges were unchanged compared to mid-April levels, average production times for each steel product we measure have declined from they were two weeks ago.

Domestic mills are largely negotiable on spot prices, according to the majority of steel buyers responding to our latest market survey.