Market Data

March 27, 2017

Consumer Confidence in March 2017

Written by Peter Wright

The source of this data is the Conference Board with analysis by Steel Market Update. Please see the end of this piece for an explanation of the indicator.

The March report was excellent and handily beat expectations by rising to 125.6 from an upwardly revised 116.1 in February. The three month moving average (3MMA) has improved for ten consecutive months and was the strongest since July 2001. The low point for consumer confidence last year was May with a value of 92.4. Consumer confidence is the driver of consumer spending which is the largest component of GDP and which ultimately drives a large portion of steel consumption.

Included at the end of this write up is the official news release from the Conference Board.

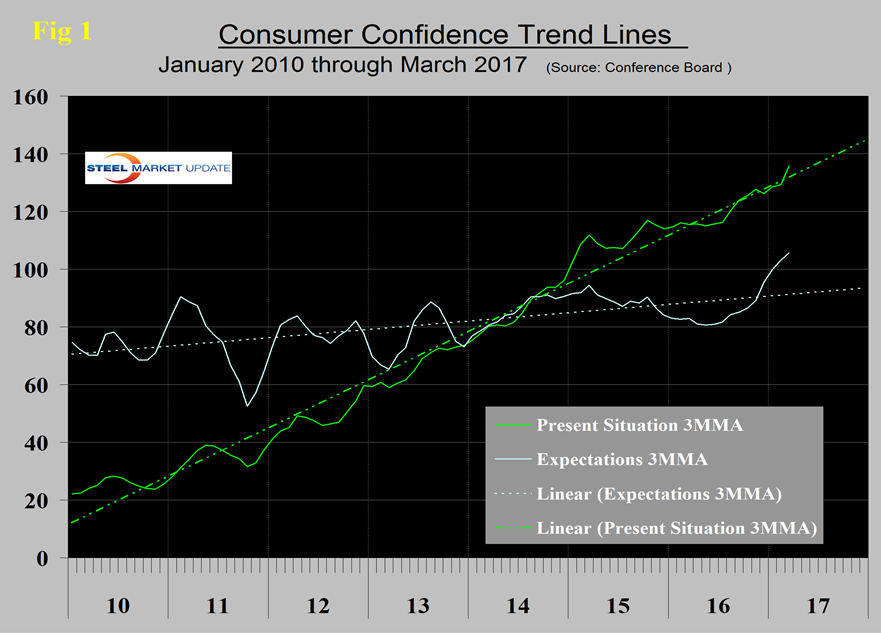

In March, the 3MMA of the composite increased from 113.7 to 117.8. We prefer to smooth the data with a moving average because of monthly volatility which, in the case of consumer confidence, has been quite extreme since the beginning of last year. The composite index is made up of two sub-indexes. These are the consumer’s view of the present situation and his/her expectations for the future. Both are now above their eight-year trend line. Expectations have surged well past their trend line in the last four months (Figure 1).

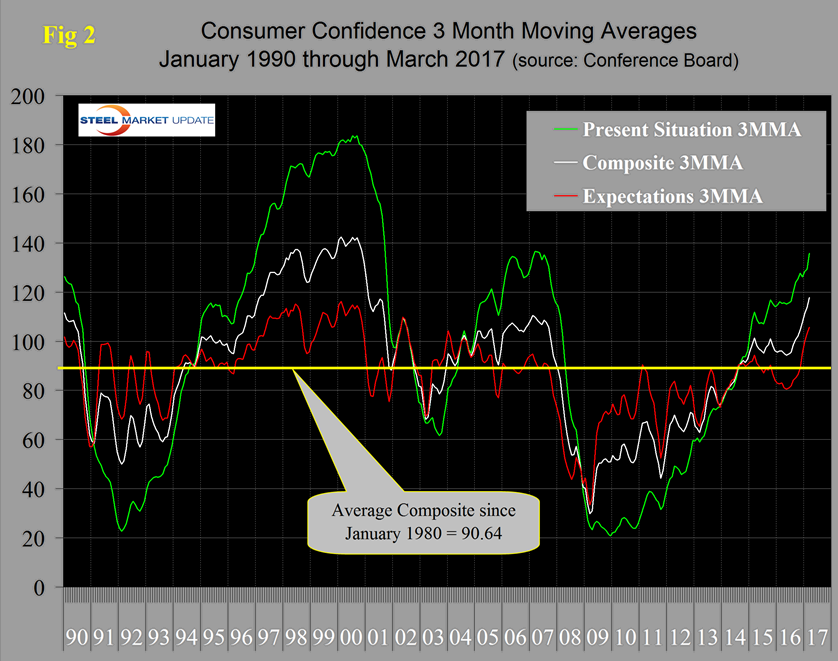

The historical pattern of the 3MMA of the composite, the view of the present situation and expectations are shown in Figure 2.

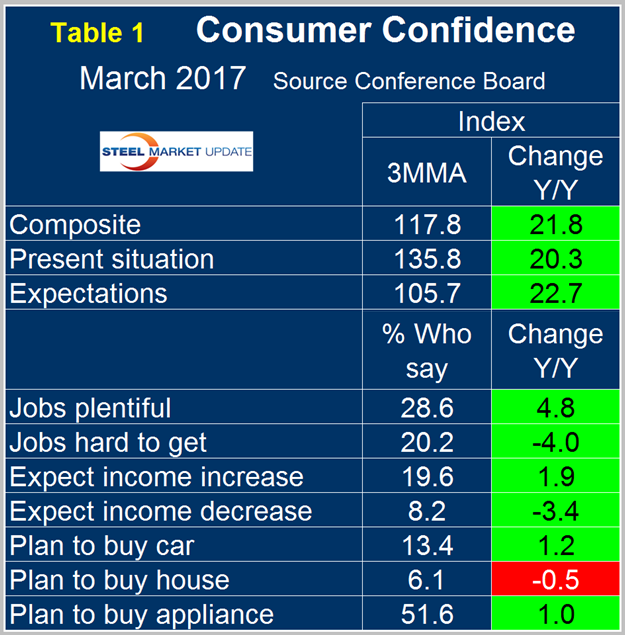

The 3MMA of the composite made no progress from early 2015 through mid-2016 as improvements in the consumer’s view of the present situation were negated y a decline in expectations. The Comparing March 2017 with March 2016 (y/y) the 3MMA of the composite was up by 21.8, the present situation was up by 20.3 and expectations were up by 22.7 (Table 1).

The only negative in Table 1 are intentions to buy a home which may be a function of rising interest rates. The consumer confidence report includes data on job availability and wage expectations. It reports on the proportion of people who find that jobs are hard to get and those who believe jobs are plentiful and it measures those who expect a wage increase or a decrease. Since August 2011 both of the job availability components have steadily improved. Expectations for wage increases have not been as consistent but in this report the differential between those expecting an increase and those expecting a decrease was the best since before the recession. Prior to the January, February and March reports, plans to buy a home had been positive y/y in 17 of the previous 19 months. Plans to buy a car have been positive y/y for 11 of the last 12 months.

SMU Comment: This was an excellent report particularly in the employment sub-components. This will drive personal consumption which is the largest component of GDP. This is turn will have a positive effect on steel consumption. Last month we commented that, “at the present rate, consumer confidence will exceed the previous peak that occurred just before the recession in the next few months.” This has become reality faster than we or most others expected.

The official news release from the Conference Board reads as follows:

The Conference Board Consumer Confidence Index Increased Sharply in March

The Conference Board Consumer Confidence Index, which had increased in February, improved sharply in March. The Index now stands at 125.6 (1985=100), up from 116.1 in February. The Present Situation Index rose from 134.4 to 143.1 and the Expectations Index increased from 103.9 last month to 113.8. The cutoff date for the preliminary results was March 16th .

“Consumer confidence increased sharply in March to its highest level since December 2000 (Index, 128.6),” said Lynn Franco, Director of Economic Indicators at The Conference Board. “Consumers’ assessment of current business and labor market conditions improved considerably. Consumers also expressed much greater optimism regarding the short-term outlook for business, jobs and personal income prospects. Thus, consumers feel current economic conditions have improved over the recent period, and their renewed optimism suggests the possibility of some upside to the prospects for economic growth in the coming months.”

Consumers’ appraisal of current conditions improved considerably in March. The percentage saying business conditions are “good” increased from 28.3 percent to 32.2 percent, while those saying business conditions are “bad” decreased from 13.4 percent to 12.9 percent. Consumers’ assessment of the labor market was also more positive. The percentage of consumers stating jobs are “plentiful” rose from 26.9 percent to 31.7 percent, while those claiming jobs are “hard to get” decreased moderately, from 19.9 percent to 19.5 percent.

Consumers were also significantly more optimistic about the short-term outlook. The percentage of consumers expecting business conditions to improve over the next six months increased from 23.9 percent to 27.1 percent, while those expecting business conditions to worsen declined from 10.5 percent to 8.4 percent.

Consumers’ outlook for the labor market was also more upbeat. The proportion expecting more jobs in the months ahead increased from 20.9 percent to 24.8 percent, while those anticipating fewer jobs declined from 13.6 percent to 12.2 percent. The percentage of consumers expecting their incomes to increase improved from 19.2 percent to 21.5 percent, while the proportion expecting a decrease declined from 8.1 percent to 7.0 percent.

About The Conference Board: The Conference Board is a global, independent business membership and research association working in the public interest. Our mission is unique: To provide the world’s leading organizations with the practical knowledge they need to improve their performance and better serve society. The monthly Consumer Confidence Survey, based on a probability-design random sample, is conducted for The Conference Board by Nielsen, a leading global provider of information and analytics around what consumers buy and watch. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months. The Conference Board is a non-advocacy, not-for-profit entity holding 501 (c) (3) tax-exempt status in the United States. www.conference-board.org.