Prices

July 23, 2017

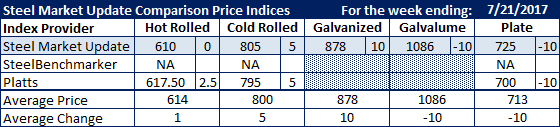

Comparison Price Indices: Yet Another Mixed Week

Written by John Packard

The week ending July 21 was another mixed week for flat rolled steel and plate prices. Steel Market Update (SMU) steel price indices saw two products as being higher, two lower and one unchanged. Platts had two higher and one lower. SteelBenchmarker did not report prices this week as they only report twice per month.

Benchmark hot rolled averages remained the same at $610 per ton, according to the SMU index, while Platts had the product up $2.50 per ton to $617.50 per ton.

Cold rolled prices were seen as being higher by $5 per ton on both the SMU and Platts indexes. The SMU average on CRC rose to $805 per ton while, Platts rose to $795 per ton.

Galvanized .060” G90 went up $10 per ton compared to the week ending July 14. At the same time, Galvalume .0142” AZ50, Grade 80 was down $10 per ton.

Both Platts and SMU saw plate prices as being lower by $10 per ton. SMU plate pricing is based on a freight delivered price, while Platts is using FOB Southeastern mill as their reference point. So, to have a $25 per ton variance between the two with SMU being higher should be considered normal.

Four domestic steel mills increased spot prices by the end of the week. We have not yet seen the increase announcement translate into firm transaction pricing. SMU will be watching the market very carefully over the next two weeks to see if there is enough momentum to take prices higher without the announcement of a Section 232 decision that is favorable to the domestic steel mills.

SMU Note: Galvanized prices include $78 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Plate price FOB points are different for each of the indexes:

SMU: FOB Delivered to the Customer (includes freight)

Platts: FOB Southeaster Mill (does not include freight)

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.