Market Data

July 22, 2018

Steel Mill Negotiations: Sensing a Shift

Written by Tim Triplett

Negotiations between steel mills and buyers may have turned a corner as the mills appear significantly more willing to negotiate spot prices than at any other point this year.

“We’re sensing that some of the steel mills have holes in their August order book for hot rolled coil,” one steel pipe executive told Steel Market Update. “Not long ago, the mills had limited tons on the spot market. Now they are open to negotiations within a very limited range.”

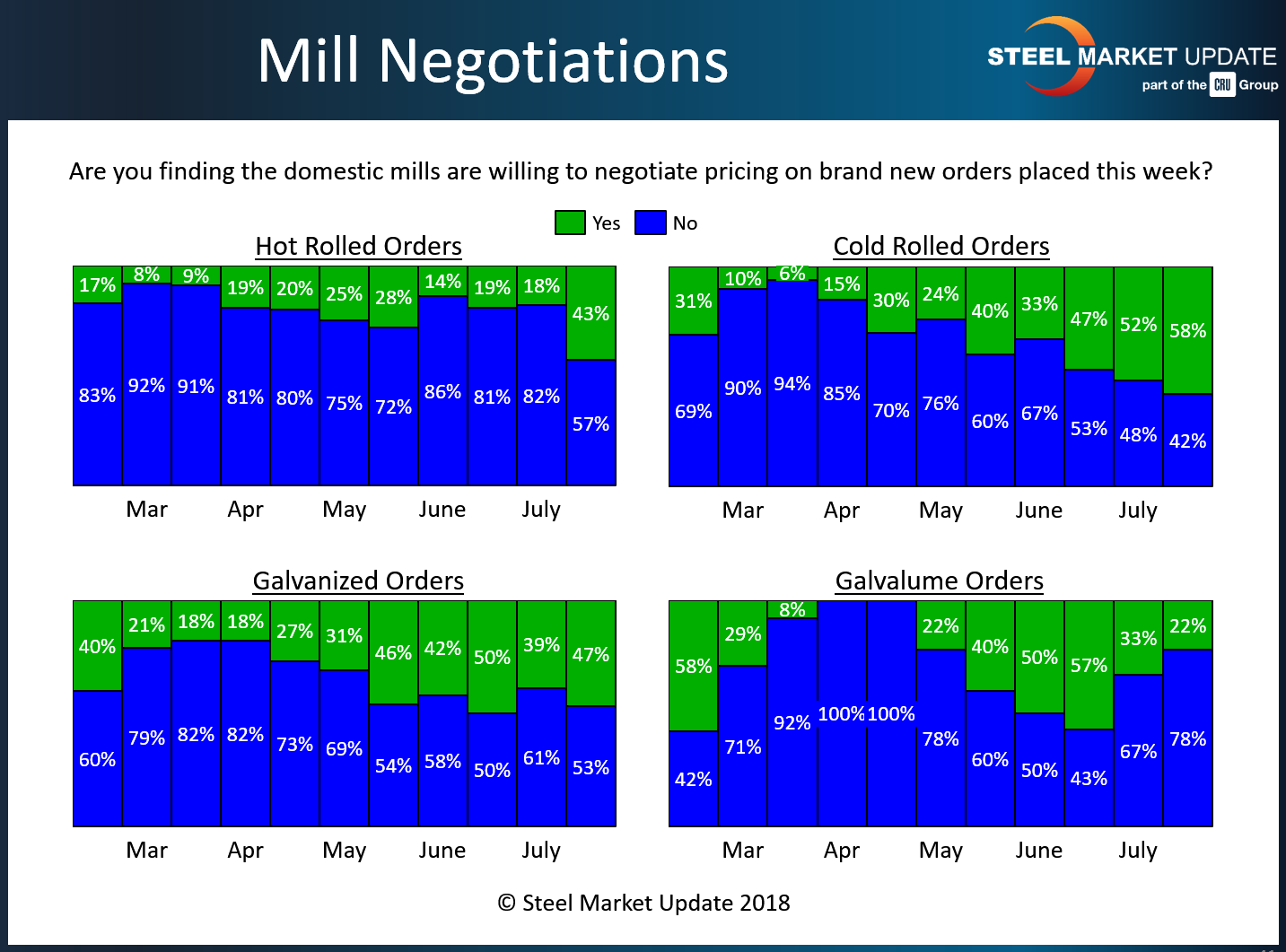

Every two weeks, in a proprietary poll, SMU tracks how buyers and sellers of flat rolled steel represent the mill negotiation position. According to respondents to this week’s market trends questionnaire, 43 percent of hot rolled buyers said they have found mills willing to negotiate, up from 19 percent one month ago. Just a small majority, 57 percent, said the hot rolled mills are still standing firm.

In the cold rolled segment, the majority, 58 percent, said they have found some mills willing to talk price, up from 47 percent a month ago. Forty-two percent of respondents reported mill prices on cold rolled as non-negotiable.

Prices on coated products appear to have loosened up a bit more recently. In the galvanized sector, 47 percent said the mills were open to price discussions, compared with 39 percent in early July. About 22 percent of Galvalume buyers said mills are now willing to talk price, down from 33 percent two weeks ago.

Don’t count on this shift in negotiating power continuing indefinitely, however. Tariffs imposed on steel products this spring will likely slow the flow of imports into the U.S. in the fourth quarter, given the typical lag of three to five months for shipment. This is likely to tighten steel supplies and firm up the mills’ negotiation position once again.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.