Market Segment

July 18, 2019

Nucor Reports Weaker Shipments in Second Quarter

Written by Sandy Williams

Nucor reported a decline in earnings for the second quarter of 2019 due to lower shipments and pricing. A build-up of inventory before the Section 232 tariffs resulted in aggressive destocking at the end of 2018 and into 2019, which impacted order rates, along with an increase in domestic steel supply and a declining scrap environment.

Nucor’s $40 per ton price increase introduced three weeks ago held in its entirety, said Nucor’s CEO and President John Ferriola. He added that the second $40 per ton increase looks encouraging.

“We are cautiously optimistic that we have hit bottom on pricing and on volumes,” said Ferriola. “We see lead times beginning to stretch out a little bit, and that has to happen before service centers come back in the market.”

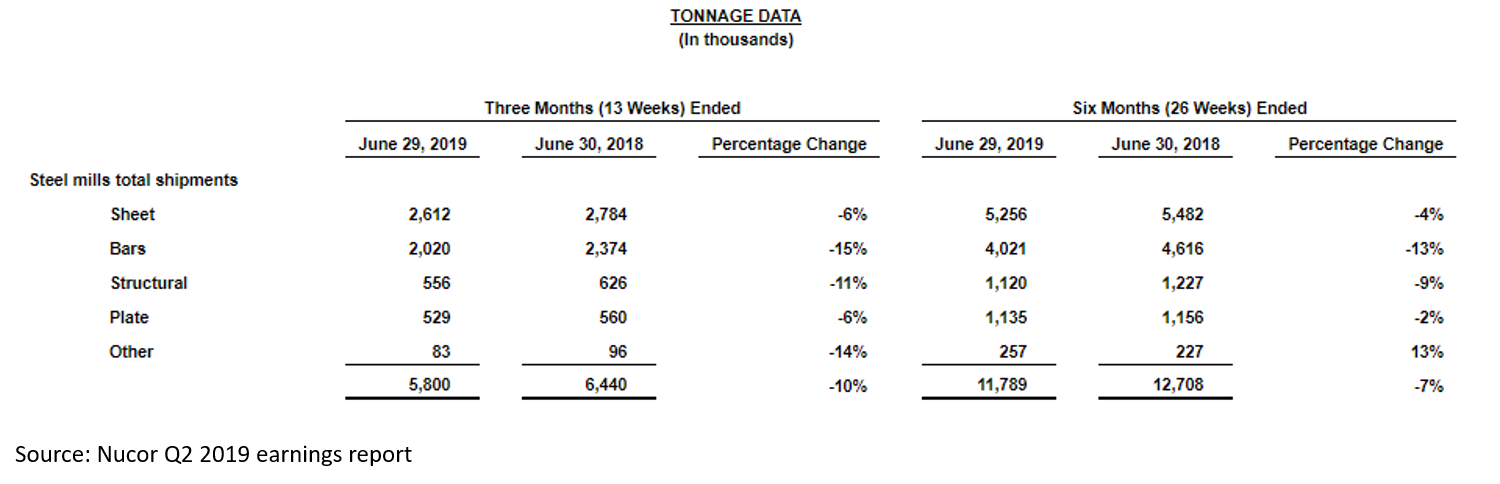

Nucor’s total steel mill shipments fell 3.0 percent in the second quarter compared to the first quarter, with the biggest declines seen in rebar and structural steel. Net sales in the quarter slipped 3.0 percent to $5.90 billion. Average price per ton declined 3.0 percent in Q2.

The downstream steel products segment fared better, with net sales increasing 3.0 percent compared to the first quarter and shipments to outside customers up 2.0 percent.

The raw materials segment was flat in the second quarter due to a planned outage at the DRI facility in Trinidad that lasted from June 19 through July 13.

The average scrap and scrap substitute cost per ton used during the second quarter declined 6.0 percent to $330.

“Unusually wet weather and aggressive supply chain destocking impacted mill order rates in the first half of 2019. We have seen lower volumes during the first half of this year resulting in a more challenging price environment,” said Ferriola. “However, real demand for our products remains strong in key end-use markets. We see healthy conditions in end-use markets that typically account for more than two-thirds of our steel shipments.”

For third quarter, Nucor is expecting steel mill segment performance to be lower than second quarter due to lower prices for flat rolled and plate steel.

“Prices for several key product lines have only recently reversed the downward trajectory that prevailed during the first half of the year due to weather conditions and service center destocking,” said Nucor. “We expect service center customers will resume more normal market demand-driven buying patterns during the third quarter of 2019.”

Nucor expects its steel products segment to continue to improve in the third quarter on strong nonresidential market conditions.

New capacity coming online for U.S. Steel and JSW will mean an end to supplying billets and blooms to the two mills, but Nucor has been securing contracts with other customers and is confident it will be able to replace the tons lost.

The new Buy American executive order is not likely to have a major impact for Nucor, which supplies plate and SBQ to the military, said Ferriola. The company is pleased, however, to see some loopholes in the sourcing policy closed.

When asked about recent reports that ArcelorMittal is requesting discounts from its suppliers on existing contracts, Ferriola said Nucor is a “high integrity company and would not demand price reductions on any contracts we have signed.” He did indicate, however, that if discounts are offered by suppliers to Nucor’s competitors and Nucor is treated differently, there may be consequences to those suppliers when contracts come up for renewal in 2020.

An outage at Nucor’s Louisiana DRI facility will begin later this quarter and last 65 days in order to complete major enhancements to the plant. Material sourcing is not expected to be an issue during the outage as Nucor has alternate sources of HBI as well as prime and obsolete scrap from David J. Joseph Company.

Nucor is expecting scrap pricing to increase $20-$30 per ton in the third quarter and pig iron to rise $10-$15 dollars. Electrode pricing dropped 7.0 percent in the second quarter, falling from unsustainable highs set last year. Refractory prices are still high with little reduction during the quarter. Alloys are also high, said Ferriola, but not quite as high as 2018.