Analysis

February 7, 2023

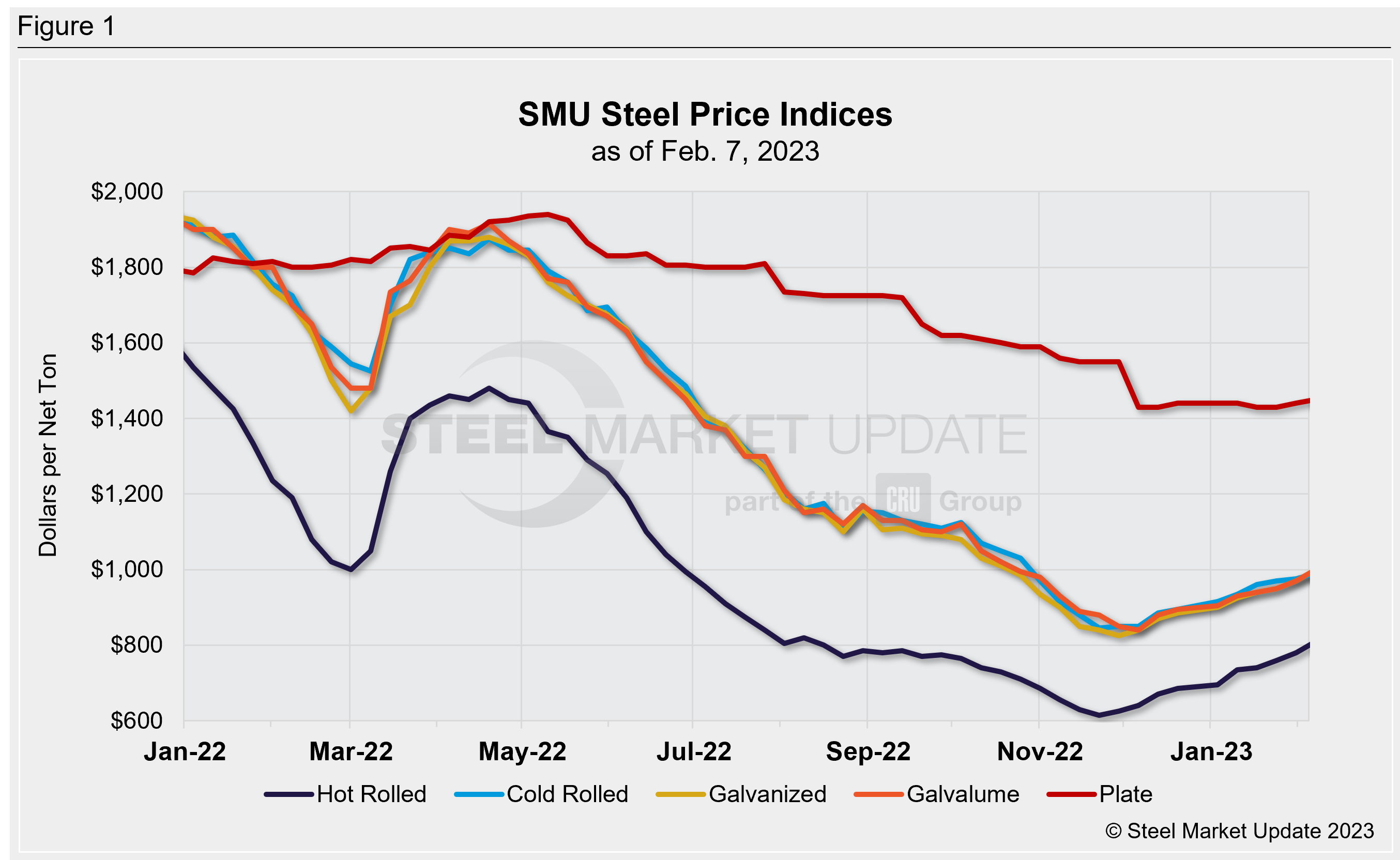

SMU Price Ranges: Another Week of Gains as Q1 Rally Continues

Written by Michael Cowden

Sheet prices continue to rise, extending a rally that began the week after Thanksgiving. SMU’s hot-rolled coil price is now above $800 per ton ($40 per cwt) for the first time since early August, roughly six months ago.

At $810 per ton on average, HRC prices are up $30 per ton from $780 per ton last week. They are also nearly $200 per ton above a 2022 low of $615 per ton recorded in mid-November.

Cold-rolled (up $15 per ton week over week) and coated prices (up $30 per ton) continue to see steady gains as well. And premiums over hot-rolled continue to hold at approximately $200 per ton.

Higher sheet prices in part reflect a wave of $50-per-ton price hikes announced last week by domestic mills.

Plate prices inched up too, rising $10 per ton to $1,450 per ton from $1,440 per ton a week ago. We see this as essentially flat given how high plate prices are to begin with.

Our price momentum indicators for sheet remain higher and our plate momentum indicator at neutral.

Hot-Rolled Coil: The SMU price range is $780–840 per net ton ($39.00–42.00/cwt), with an average of $810 per ton ($40.50/cwt) FOB mill, east of the Rockies. The bottom end of our range increased by $20 per ton, while the top end rose $40 per ton vs. one week ago. Our overall average is up $30 per ton from one week ago. Our price momentum indicator on hot-rolled steel points to Higher, meaning we expect prices to increase over the next 30 days.

Hot-Rolled Lead Times: 4–7 weeks

Cold-Rolled Coil: The SMU price range is $960–1,020 per net ton ($48.00–51.00/cwt) with an average of $990 per ton ($49.50/cwt) FOB mill, east of the Rockies. Our cold-rolled range widended this week when compared to last week. The bottom end rose $10 per ton, while the top end of our range icrease $20 per ton compared to one week ago. Our overall average is up $15 per ton from one week ago. Our price momentum indicator on cold-rolled steel points to Higher, meaning we expect prices to increase over the next 30 days.

Cold-Rolled Lead Times: 5–9 weeks

Galvanized Coil: The SMU price range is $980–1,020 per net ton ($49.00–51.00/cwt) with an average of $1,000 per ton ($50.00/cwt) FOB mill, east of the Rockies. The lower end of the range rose $40 per ton, while the top end of our range increased $20 per ton vs. one week ago. Our overall average is up $30 per ton from one week ago. Our price momentum indicator on galvanized steel points to Higher, meaning we expect prices to increase over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,077–1,117 per ton with an average of $1,097 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5–9 weeks

Galvalume Coil: The SMU price range is $980–1,020 per net ton ($49.00-51.00/cwt) with an average of $1,000 per ton ($50.00/cwt) FOB mill, east of the Rockies. The lower end of the range rose $40 per ton vs. the week prior, while the top end of our range was up $20 per ton compared to one week ago. Our overall average is up $30 per ton from one week ago. Our price momentum indicator on Galvalume steel points to Higher, meaning we expect prices to increase over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,274–1,314 per ton with an average of $1,294 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 7–8 weeks

Plate: The SMU price range is $1,420–1,480 per net ton ($71.00–74.00/cwt) with an average of $1,450 per ton ($72.50/cwt) FOB mill. The lower end of range rose $20 per ton vs. the prior week, whilte the top end of our range was unchanged compared to one week ago. Our overall average is up $10 per ton from one week ago. Our price momentum indicator on steel plate is Neutral, meaning we are still unsure whether prices will remain stable, or move up or down over the next 30 days.

Plate Lead Times: 4–7 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

By Michael Cowden, michael@steelmarketupdate.com