Prices

September 10, 2013

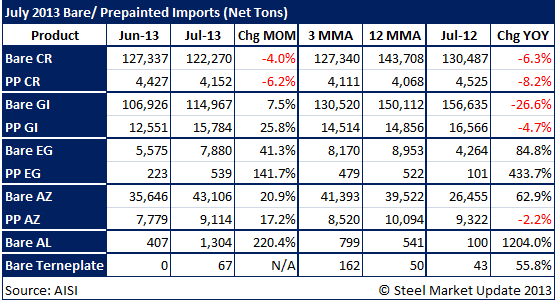

Prepainted Flat Rolled Imports Down in July

Written by Brett Linton

Prepainted flat rolled imports moderately increased in July over June for all products with the exception of prepainted cold-rolled sheet and strip. Compared to the same month one year ago, this month’s prepainted imports slightly decreased for all products with the exception of prepainted electro-galvanized sheet and strip.

As you can see by our table below – prepainted cold rolled (CR) imports decreased by 275 NT from June to July but remained above both the 3-month and 12-month moving averages calculated through July. Compared to levels one year ago, prepainted CR imports were down 373 NT or 8.2 percent.

Prepainted galvanized (GI) imports increased by 3,233 NT month-over-month. They are now above both the 3-month and 12-month moving averages. Compared to one year ago, prepainted GI imports were down 782 NT or 4.7 percent.

Prepainted electro-galvanized (EG) imports increased by 316 NT or 141.7 percent month-over-month. They were above both the 3-month and 12-month moving averages. Compared to one year ago, prepainted EG imports were up 438 NT or 433.7 percent. Note that prepainted EG imports are much smaller than the other products in this comparison, and fluctuations in imports from China tend to skew the figures from month to month.

Prepainted Galvalume (AZ) imports increased by 1,335 NT over last month, right in between the 3-month and 12-month moving average. Tonnage imported in July was down 208 NT or 2.2 percent over that of last year.