Market Data

January 12, 2014

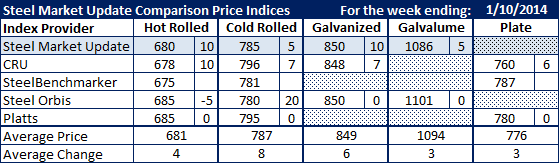

SMU Comparison Price Indices: Prices Move Higher

Written by John Packard

Flat rolled steel prices began to rise this past week according to the steel indices releasing data for the week. Benchmark hot rolled now averages $681 per ton with the range being $675 to $685 per ton (although the $675 is from SteelBenchmarker who did not report new numbers last week). Cold rolled is approaching $800 per ton and both galvanized and Galvalume also saw modest increases.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

SteelOrbis: Midwest Domestic Mill.

Platts: Northern Indiana Domestic Mill.