Prices

June 7, 2014

April Apparent Steel Supply Up 9.1%

Written by Brett Linton

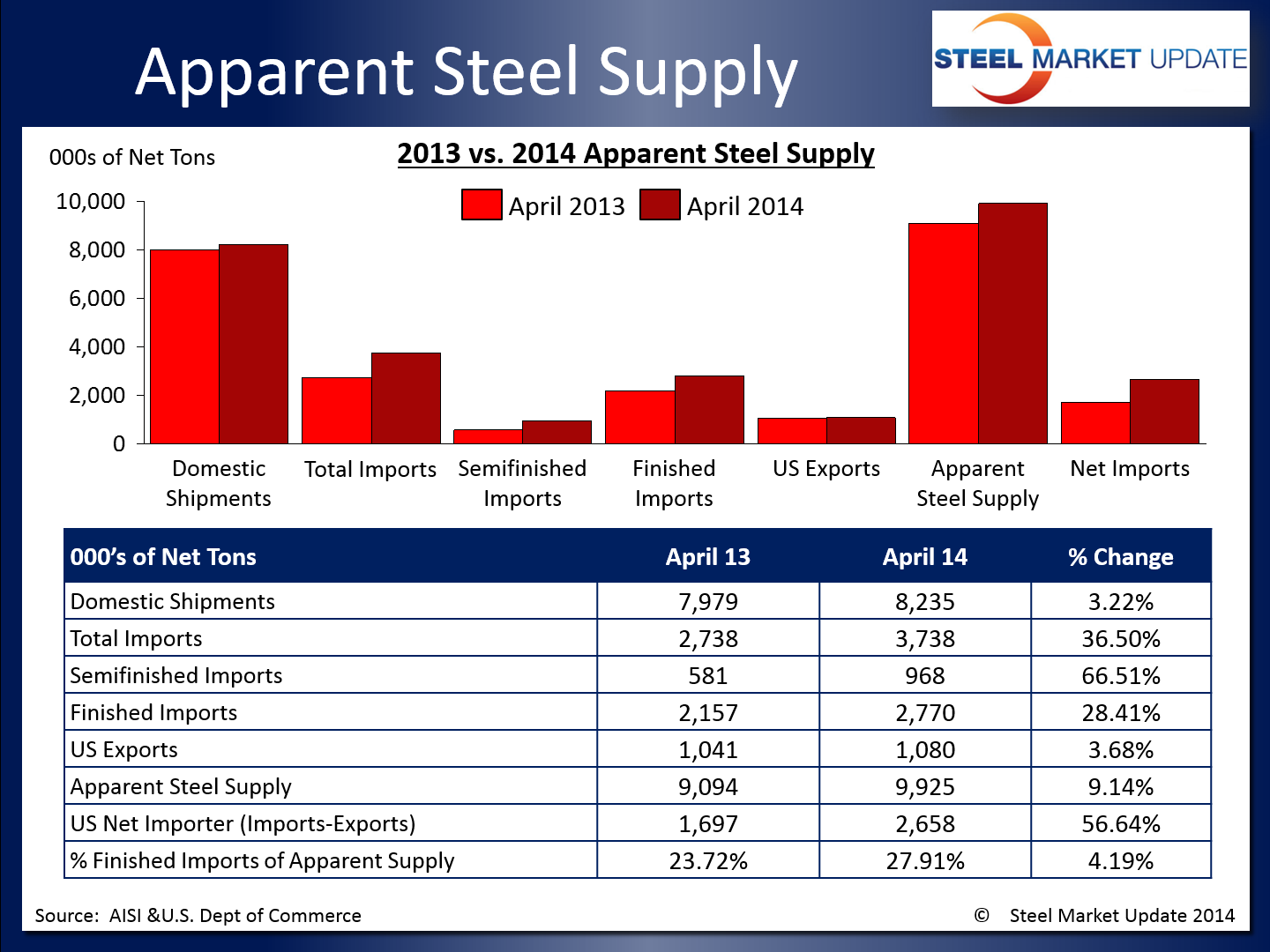

Apparent steel supply for April was 9,925,287 net tons, the highest figure Steel Market Update has in its recorded history beginning in January 2010. April supply represents an 831,098 ton or 9.1 percent increase compared to the same month one year ago. This is primarily due to the massive spike in April imports, up 36.5 percent or nearly 1,000,000 net tons over April 2013 tonnage. Steel imports captured 27.91 percent of the total U.S. market during the month of April.

Domestic shipments, finished imports, and total exports also increased over levels one year prior. The net trade balance between imports and exports was a surplus of 2,658,304 tons in April, an increase of 56.6 percent from the same month last year, and the highest figure in our 4+ year recorded history.

When compared to last month when apparent steel supply was at 9,753,954 tons, April supply increased by 171,333 tons or 1.8 percent. This is due to a decrease in domestic shipments but an increase in finished imports and total exports.

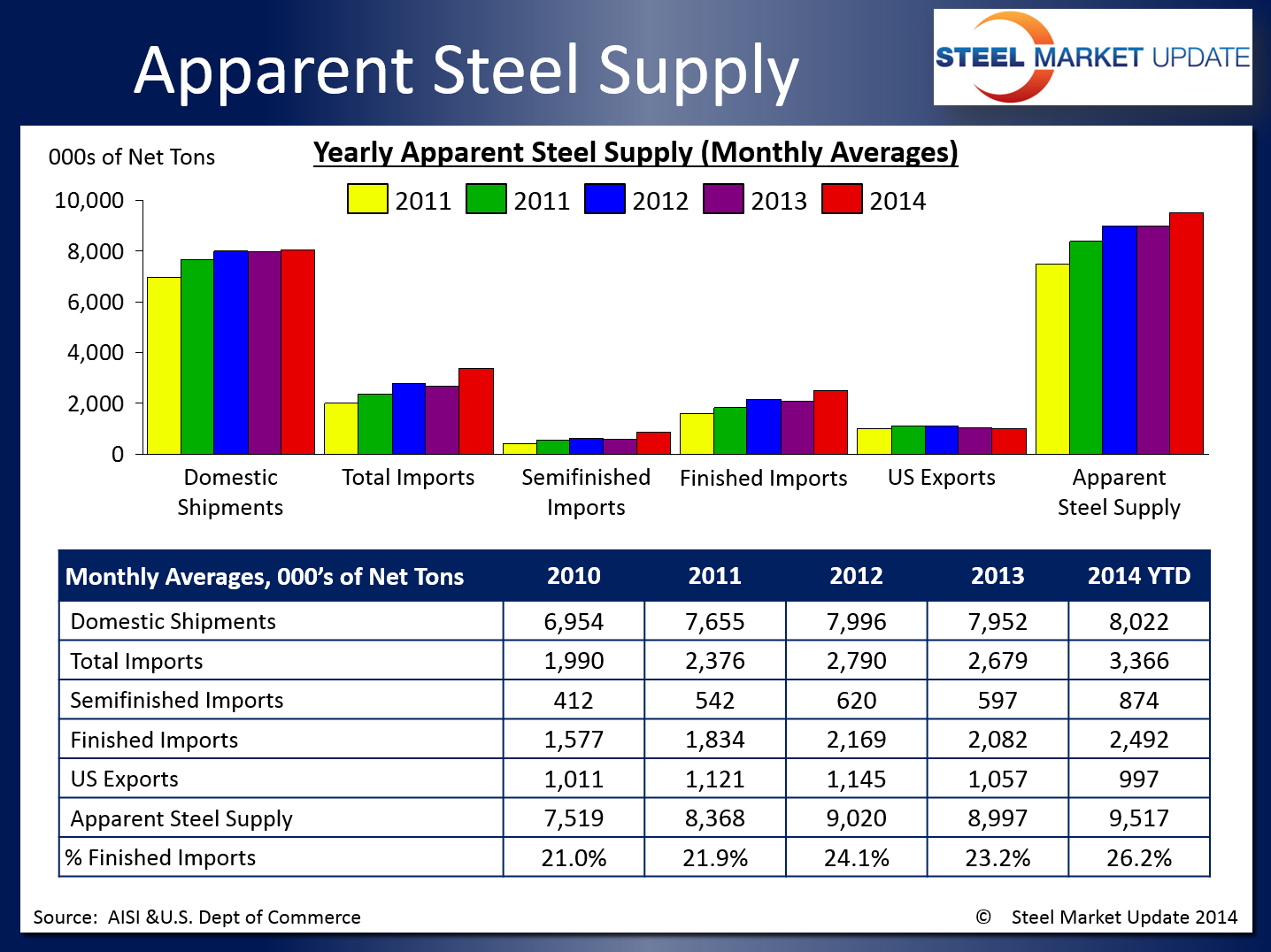

On a year to date basis, the 2014 YTD averages are all above what we saw during in the previous two years, with the exception of total exports. They are significantly higher than the averages we saw in 2010 and 2011.

SMU Note: You can view the interactive graphic below when you are logged into the website and reading the newsletter online. If you have not logged into the website in the past and need a new user name and password we can do that for you out of our office. Contact us at: info@SteelMarketUpdate.com or by calling 800-432-3475. If you need help navigating the website we would also be very happy to assist you.

{amchart id=”120″ Apparent Steel Supply- Domestic Shipments, Semi-Fin Imports, Exports}