Prices

January 20, 2015

Why the Energy Sector is Important to Steel

Written by Paul Lowrey

A lot has already been written about the dramatic decline in oil prices, the persistent high imports of energy tubulars, and related issues. What is missing, in my opinion, is some perspective and context to pull it all together. The purpose of this article is to show why the energy sector is so important to the steel industry.

How big is the energy sector in steel consumption terms? I hope to surprise more than a few of you with the answer. The NAFTA energy sector consumes about the same amount of steel as the NAFTA automotive industry. Think about that for a minute. It means that energy and automotive are tied for second as the largest markets for steel after the construction market.

NAFTA automotive production levels have been 16 to 17 million units for the last two years. It takes about 1.25 tons of steel +/- to manufacture a car, depending and the size & type of vehicle. This number is on a pre-stamping basis including all products – flat & long, and all grades – carbon, alloy, and stainless. This translates to about 20 to 21 million tons of steel required by the NAFTA automotive industry.

Domestic energy tubular consumption has averaged about 12 million tons the last couple of years. This includes OCTG & line pipe, welded & seamless, and domestic & import supply. Canada & Mexico add approximately 3 million tons more (statistics are not readily available for these two countries). This brings total NAFTA consumption to about 15 million tons. It requires at least 16 million tons of steel including the pipe & tube manufacturing yield loss.

Clearly, energy tubulars is the single largest application for steel in energy. The following list identifies ten more significant steel-intensive applications. Each consumes hundreds of thousands of tons of steel each year (all forms – flat, plate, and long products).

– Production tanks

– Wind towers

– Frac tanks

– Tank railcars

– Storage tanks

– Tank barges

– Drill rigs (on & off-shore)

– Sucker rods

– Drill collars

– 55 Gallon drums

There are a number of smaller applications as well. When you add it all up, you get about 20 million tons – the same number as the NAFTA automotive industry.

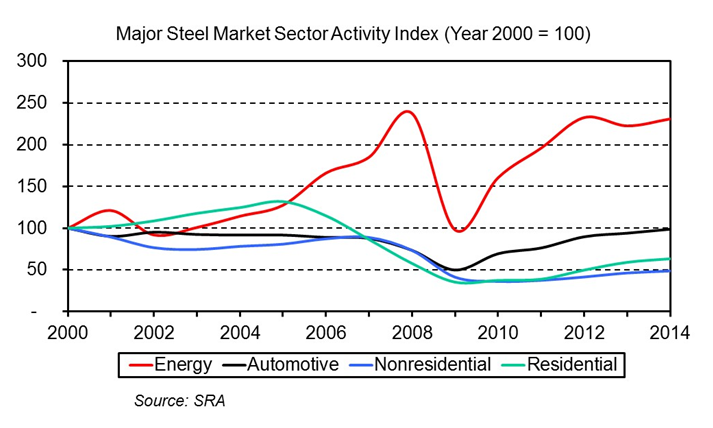

It hasn’t always been this way. Construction and automotive were the two largest markets for steel. However, both peaked last decade. In fact, energy is the only major steel market that has shown structural growth in the last 15 years. This is illustrated in the following chart.

The chart requires a little explanation. All sector activity was converted to an index to display on one graph. Energy equals domestic energy tubular consumption (tons), automotive equals NAFTA production levels, non-residential equals square feet of construction, and residential equals new housing starts.

Clearly, energy steel consumption will take a significant hit this year with the dramatic decline in the price of oil. Several energy tubular mills have recently been idled or production cuts have been put in place. In addition, I expect import levels to decline in the coming months. Given its overall size, the decline in energy will impact aggregate steel supply & demand during 2015. Hopefully, continuing strength in automotive and an accelerating recovery in construction will offset the decline in energy.