Prices

February 10, 2015

2014 Apparent Steel Supply Up 11.5% Over 2013

Written by Brett Linton

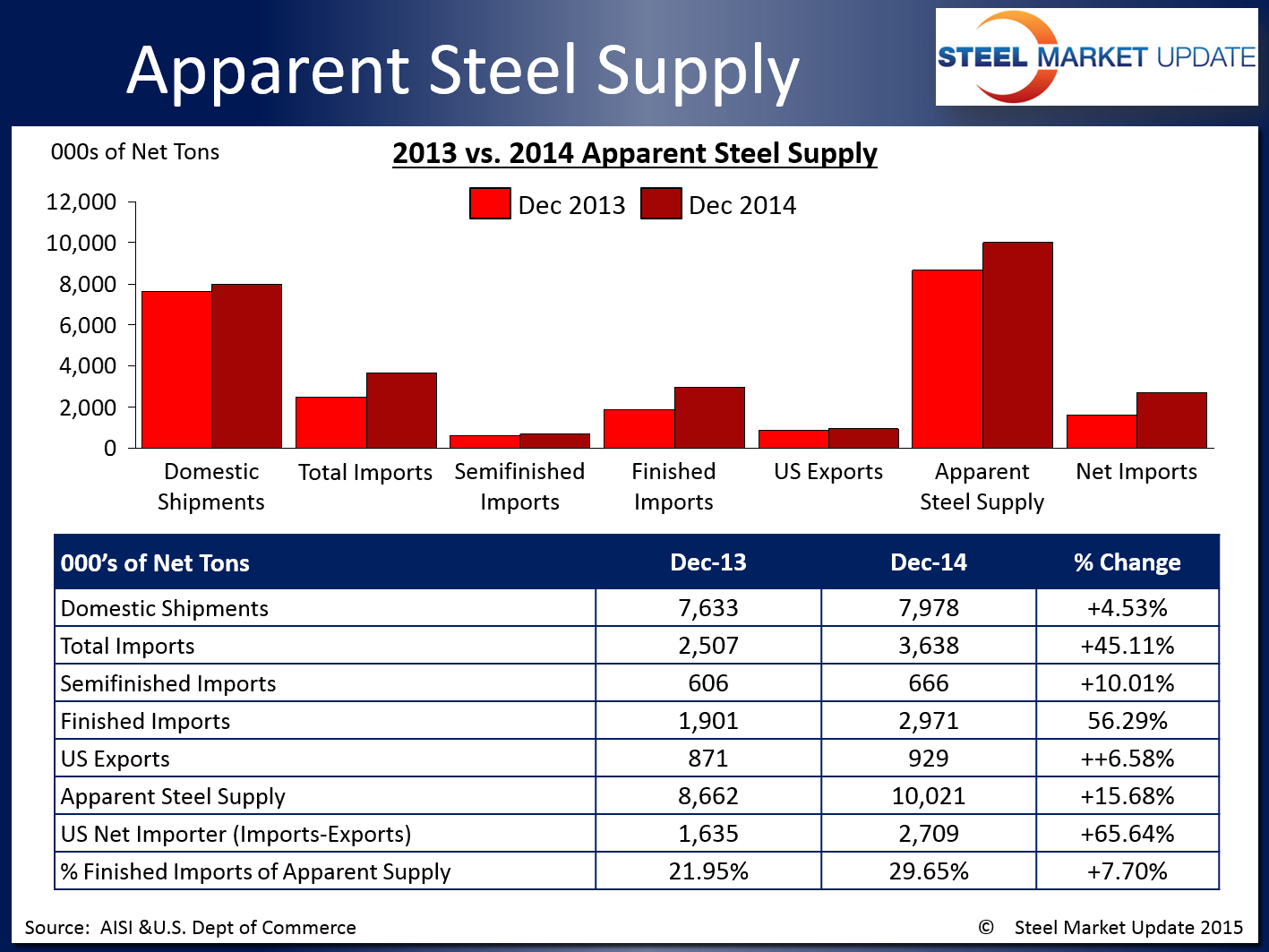

Apparent steel supply for the month of December 2014 was 10,020,704 net tons, the sixth month in 2014 to be above the 10 million ton mark. Steel Market Update calculates our apparent steel supply figure by combining total domestic steel shipments with finished US steel imports and subtracting total US steel exports.

December supply represents a 1,358,492 ton or 15.7 percent increase compared to the same month one year ago. This is primarily due to the massive spike in 2014 imports, with total December imports up 45.1 percent or 1,130,767 tons over December 2013 tonnage. When separated into to finished imports, there was a 56.3 percent or 1,070,143 ton increase compared to the same month one year ago. Domestic shipments and total exports also increased over levels one year prior, up 4.5 and 6.6 percent respectively. The net trade balance between imports and exports was a surplus of 2,708,846 tons in December, an increase of 65.6 percent from the same month last year.

SMU Note: Our Premium Level apparent steel supply analysis goes into more detail as we provide data on apparent steel supply for both flat and long products. We published this analysis earlier this week to our Premium members.

When compared to last month when apparent steel supply was at 9,637,349 tons, December supply increased by 340,224 tons or 4.5 percent. A 4.5 percent increase in domestic shipments and a 2.6 percent decrease in total exports accounted for the majority of the apparent supply increase.

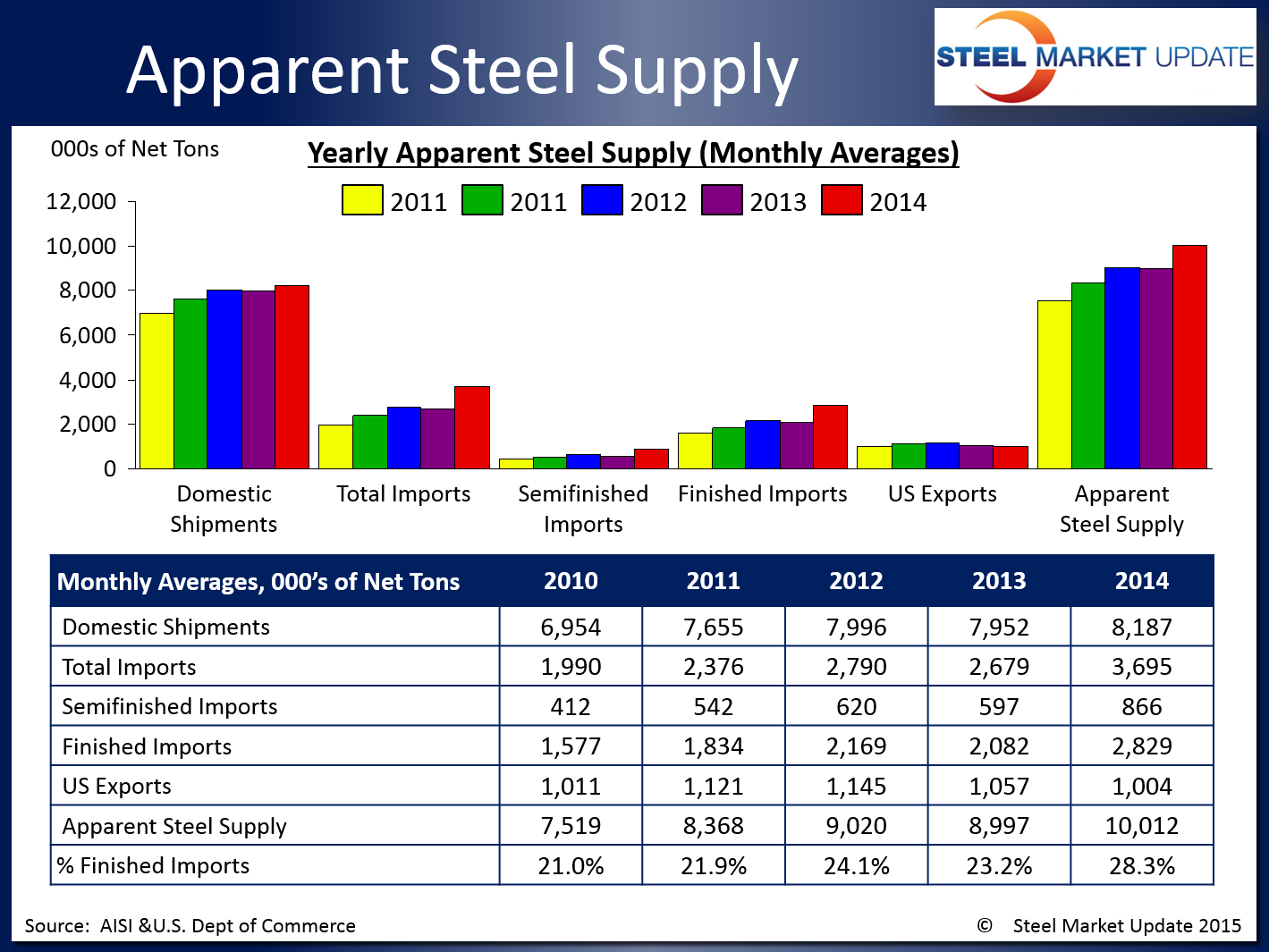

On a yearly basis, total 2014 figures were all above what we experienced during previous years, with the exception of total exports which were slightly down. Total apparent steel supply for 2014 was 120,149,537 net tons, the highest yearly level recorded since 2006 when it was 137,566,075 tons. Total 2014 apparent supply was 11.5 percent greater than 2013, 11.0 percent greater than 2012, 19.6 percent greater than 2011, and 33.2 percent greater than 2010. Below is a table showing the monthly averages for each data set for the last five years.

You can view the interactive graphic of our Apparent Steel Supply history below when you are logged into the website and reading the newsletter online. If you need help accessing or navigating the website, don’t hesitate to contact us at info@SteelMarketUpdate.com or 800-432-3475.

{amchart id=”120″ Apparent Steel Supply- Domestic Shipments, Semi-Fin Imports, Exports}