Prices

December 6, 2015

Comparison Price Indices: Last Big Move?

Written by John Packard

Over the past few weeks we have seen major movement in flat rolled steel prices. The question now is have we seen the end of the major moves lower (some suggest hot rolled has a way to go since lead times are not yet into January at most mills) or do we have a way to go?

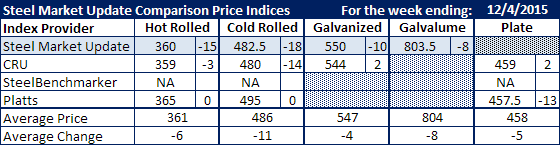

Steel Market Update picked up lower numbers on hot rolled, cold rolled and coated products this past week which were noted in our index pricing. We actually moved our hot rolled number twice during the week as we the number of offers below $360 hit our desks. However, the majority of the buyers are reporting hot rolled in the $350-$370 range but we are seeing numbers both above and below those numbers.

Benchmark hot rolled numbers dropped on both SMU($360) and CRU ($359) with Platts remaining at $365 for another week. SteelBenchmarker did not report prices this past week as they only report pricing twice per month.

Cold rolled prices also dropped on both SMU ($482.50) and CRU ($480) this past week. Platts kept their CR index at $495 and did not make any price adjustments this past week.

Galvanized was down $10 on SMU ($550 for .060” G90) and was up $2 per ton on CRU ($544 per ton for the same item).

SMU saw Galvalume as being $8 per ton lower than the week before. The $803.50 number is based on .0142” AZ50, Grade 80 as the benchmark for the AZ product.

CRU had plate up $2 per ton to $459 per ton while Platts showed the product as being $13 per ton lower than the prior week ending up at $457.50 per ton.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.