Market Data

January 3, 2016

December 2015 at a Glance

Written by John Packard

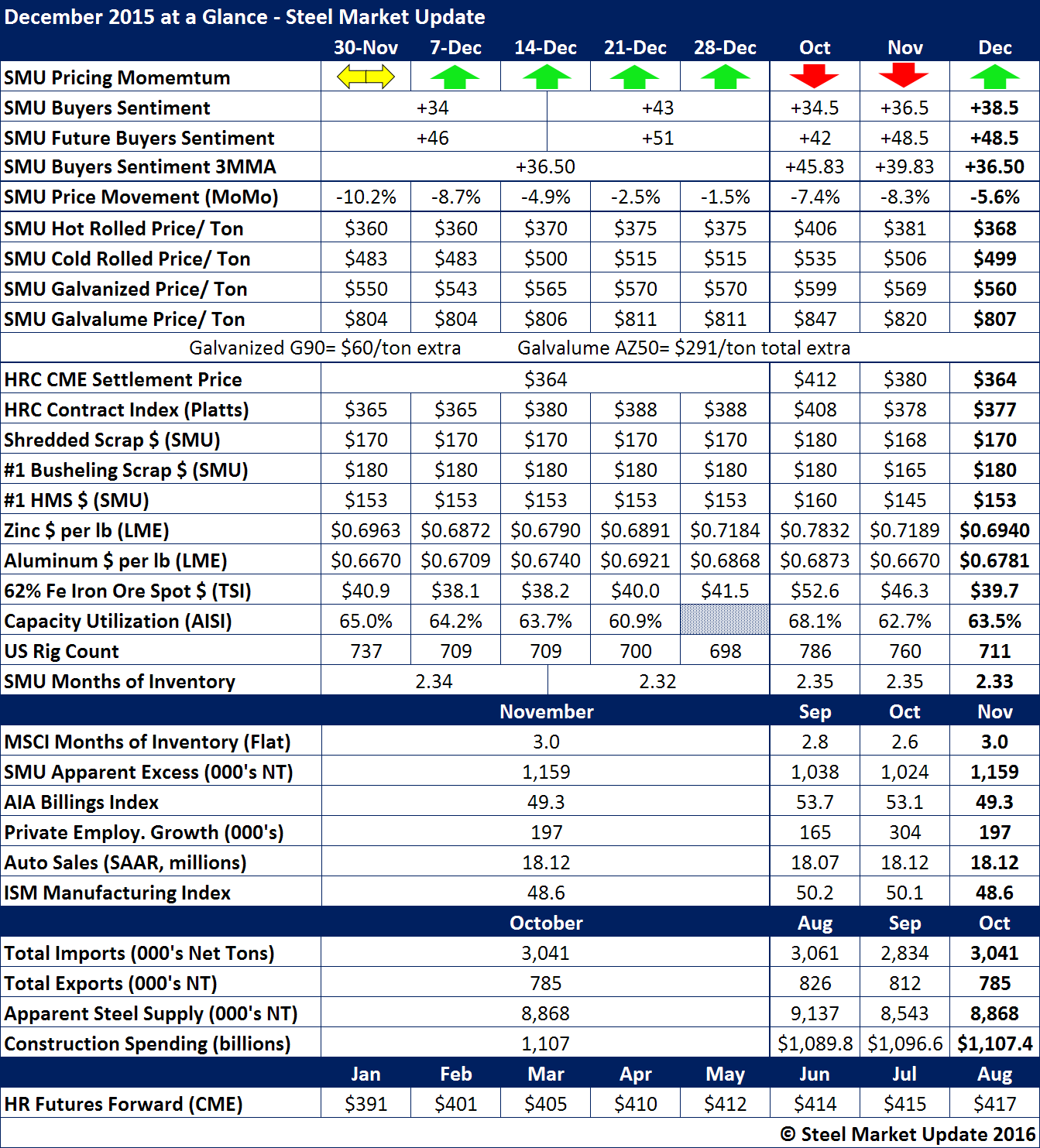

The first thing that jumps out at you when taking a look at the December steel and economic data is the change in the direction flat rolled steel prices took early in the month as the domestic steel mills raised prices for the first time since the Spring 2015 (which resulted in a dead cat bounce). It is too early to tell if we will see the same kind of bounce over the next couple of months, but, our opinion is it feels like it has staying power provided the mills (AK/USS/AM) follow through with capacity reductions.

We continue to be concerned about our SMU Steel Buyers Sentiment Index (3MMA) which has been moving steadily lower for a number of months and December did not alter that trend.

SMU average hot rolled price averaged $368 per ton with prices moving above that number over the last three weeks of the month. However, hot rolled is the weakest of the flat rolled products and we saw more movement in cold rolled and coated steels with CR averaging $499 per ton (but ending the month at $515 up $32 for the month), galvanized averaged $560 per ton for .060” G90 ($3.00/cwt extra or $60 per ton). For the month, GI prices were up $20 (average – much more when looking at the lower end of the range). Galvalume prices for .0142” AZ50, Grade 80 averaged $807 per ton. What we are finding with some of the AZ suppliers is they are going after recouping extras and we expect the AZ number to rise dramatically in the weeks ahead. One of the questions remaining on AZ is how will the trade cases influence prices – especially with Taiwan and Korea essentially being let off the hook.

Scrap prices began to rise during December negotiations and are expected to move higher as we move into January.

Inventories are still a concern and we will have to wait and see if the final December numbers show a reduction in flat rolled inventories. Our Apparent Excess model saw inventories as being up slightly in November but we are forecasting a drop over the next few months.

Imports for November and December should be well below the October 3 million net ton mark.