Prices

December 13, 2016

November & December Foreign Steel Import Analysis

Written by John Packard

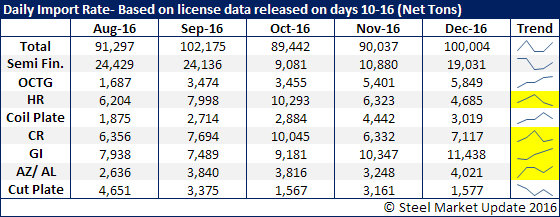

November import license data is suggesting the month will come in just shy 3.0 million net tons (2.9 million net tons). The U.S. Department of Commerce updated their import monitoring system this afternoon and the early trend for December as for the month to end up around 3.1 million tons.

SMU believes the 3.1 million net tons is overstating the true strength of the market and the true December number will be closer to the October number than the November number.

We are seeing smaller tonnage in hot rolled and coiled plate. Otherwise, early returns show increases in CR, GI and AZ.

But, the month is early and we will need to let each item play itself through the market. Our expectation is when the holidays are taken into consideration most likely the pace of license data will wane and the December number will retreat.

We thought it a little early to provide a full month forecast and instead have opted for a look at the weekly trend (see below). Next week we will have more confidence in the numbers.