Prices

March 14, 2017

January Apparent Steel Supply Rises to 1.5 Year High

Written by Brett Linton

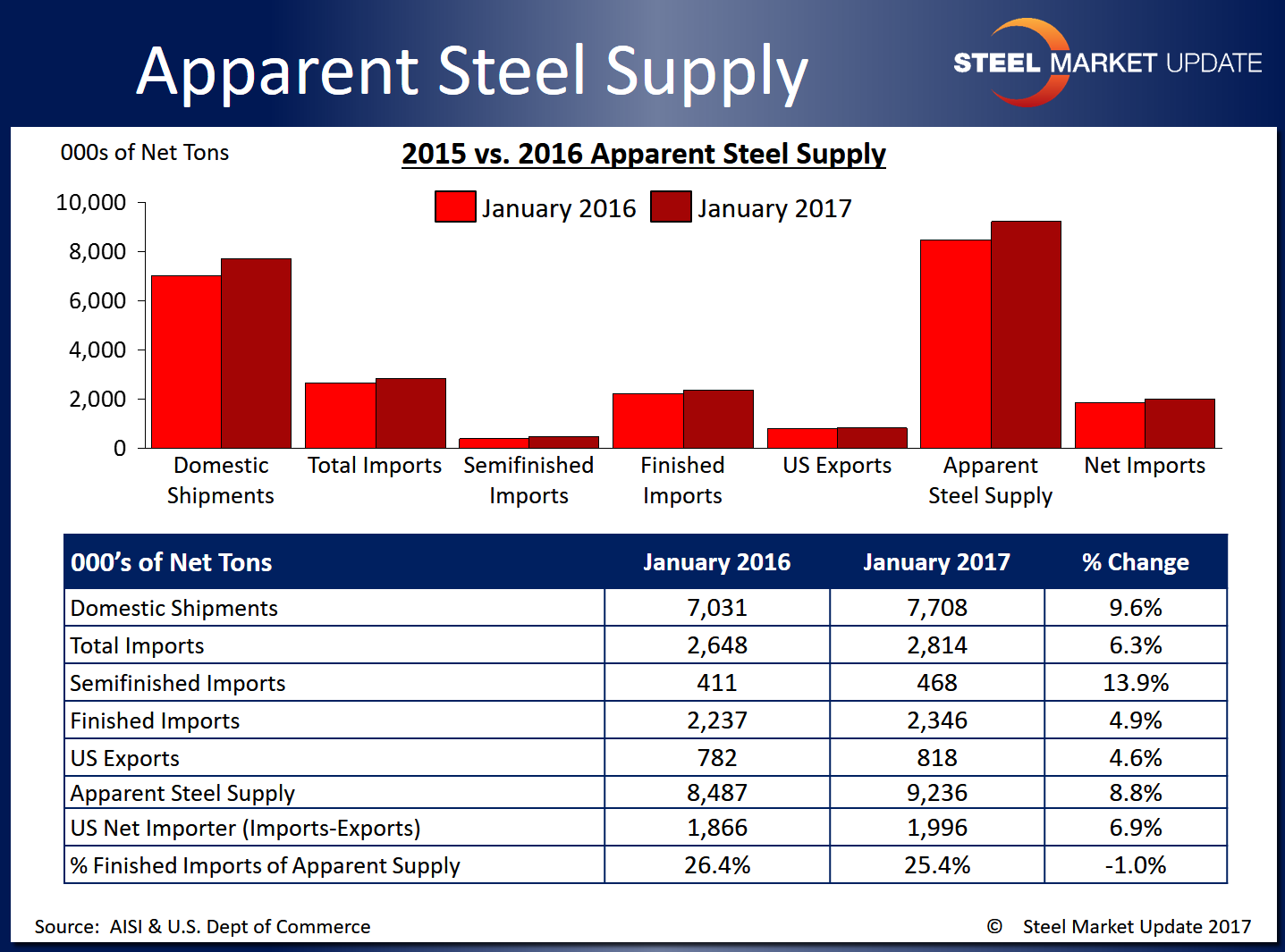

According to the latest data released from the U.S. Department of Commerce and the American Iron and Steel Institute, apparent steel supply for the month of January 2017 was 9,236,140 net tons. Apparent steel supply is calculated by adding domestic steel shipments and finished US steel imports, then subtracting total US steel exports.

This is the highest apparent steel supply figure since July 2015 when it was 9,409,421 tons.

January apparent steel supply represents a 749,526 ton or 8.8 percent increase compared to the same month one year ago when apparent steel supply was 8,486,614 tons. The majority of this change came from an increase in domestic shipments and finished imports. Shipments increased 677,109 tons or 9.6 percent and finished imports were up 108,677 tons or 4.9 percent. Total exports rose 36,259 tons or 4.6 percent, slightly negating the rise in apparent steel supply.

The last time domestic shipments were this high was in June 2015 when they were at 7,758,087 tons.

The net trade balance between US steel imports and exports was a surplus of +1,995,651 tons imported in January 2017, 6.9 percent higher than that of January 2016. Foreign steel imports accounted for 25.4 percent of apparent steel supply, down 1.0 percent over the same month one year ago.

When compared to last month, when apparent steel supply was 8,622,171 tons, January supply increased by 613,970 tons or 7.1 percent. This was primarily due to an increase in domestic imports, up 535,171 tons or 7.5 percent month over month. The remainder of the increase was from finished imports rising 170,382 tons or 7.8 percent. A rise in total exports of 91,583 tons or 12.6 percent slightly reduced the month over month increase.

To see an interactive graphic of our Apparent Steel Supply history, visit the Apparent Steel Supply page in the Analysis section of the SMU website. If you need any assistance logging in or navigating the website, contact us at info@SteelMarketUpdate.com or 800-432-3475.